- Vietnam top buyer of Japanese scrap in Q1

- Thailand’s imports jump threefold y-o-y in Jan-Mar’25

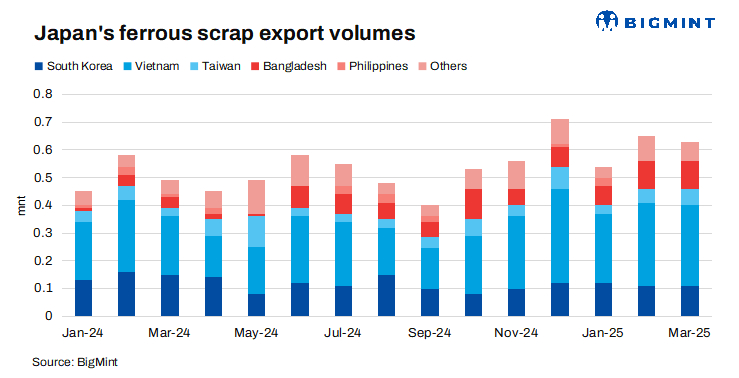

Japan’s ferrous scrap exports rose by 22% q-o-q to 1.82 million tonnes (mnt) in Q1CY’25, up from 1.49 mnt in Q4CY’24. On a y-o-y basis, exports increased by 18% compared to 1.54 mnt in Q1CY’24.

Strong demand from Vietnam, Bangladesh, India, Thailand, and Taiwan drove the growth in Japan’s ferrous scrap exports. Notably, shipments to Vietnam exceeded 800,000 t, marking the highest import volumes from Japan in Q1CY’25.

Key updates

Crude steel production: Japan’s crude steel production dropped by 2% q-o-q to 20.39 mnt in Q1, down from 20.72 mnt in Q4CY’24. Y-o-y, production declined by 5% from 21.45 mnt in the year-ago period.

Average H2 export prices: Average H2 scrap export prices stood at $294/t FOB Japan in Q1, down $14/t q-o-q from $308/t in Q4 of last year. Y-o-y, prices fell by $69/t from $363/t in Q1CY’24.

Country-wise exports

Vietnam: Vietnam remained Japan’s largest ferrous scrap buyer, with imports rising by 4% q-o-q to 838,562 t in Q1, up from 803,882 t in Q4CY’24.

On a y-o-y basis, imports increased by 23% from 683,816 t in Q1CY’24.

This notable increase was supported by strong steel sales despite lower production. Also, the price of Japanese H2 scrap dropped from $334/t in Q4 of last year to $323/t in Q1, down by $11/t, which contributed to the increase in imports during this quarter, as the lower price made the material more attractive to buyers.

On the domestic front, demand showed early signs of recovery with resumed construction activity, but buyers continued to tread carefully, monitoring international trends before committing to larger purchases.

South Korea: Imports from Japan increased by 12% q-o-q to 336,626 t in Q1, up from 300,684 t in Q4CY’24. Imports declined sharply by 24% from 441,590 t in Q1CY’24.

Import volumes had been limited in January due to South Korea’s New Year holidays, which led to a slowdown in activities.

Japanese H2 scrap offers stayed firm due to port congestion and tight supply, but Korean mills showed little buying interest. A struggling construction sector and rebar production cuts further dampened demand, prompting some suppliers to shift focus to Vietnam.

Despite lower prices prompting mills to secure material, warehousing is outpacing shipments, resulting in continued inventory accumulation.

Bangladesh: Imports from Japan increased by 21% q-o-q to 274,023 t in Q1, up from 227,148 t in Q4CY’24. On a y-o-y basis, imports saw a sharp threefold rise from 91,205 t in Q1CY’24.

India: Japan’s scrap exports to India decreased by 30% q-o-q to 56,122 t in Q1 down from 80,709 t in Q4CY’24. Y-o-y, exports surged exponentially by 25 times, compared to 2,289 t in Q1 of last year.

Steel demand and prices remained under pressure for six months but saw an uptick in mid-February, driven by speculation over a safeguard duty and rebar production cuts. While demand was largely met by domestic scrap and DRI, steady imported scrap bookings every 15-20 days prevented a sharp decline in imports. Purchases were limited to essential restocking, primarily from nearshore suppliers such as Japan and Oceania, leading to increased arrivals.

Thailand: Scrap exports to Thailand increased significantly by 55% q-o-q to 48,595 t in Q1, up from 31,439 t in Q4CY’24. On a y-o-y basis, exports rose threefold compared to 14,323 t in Q1CY’24.

Outlook

Japan’s ferrous scrap exports are expected to remain strong, with Vietnam and Bangladesh continuing to drive demand amid rising steel sales. India may also continue its imports from Japan, while South Korea’s intake could improve with steady buying.

Leave a Reply