- Asian buyers cautious amid seasonal steel demand slowdown

- JPY volatility, tariff risks pressure Japanese scrap offers

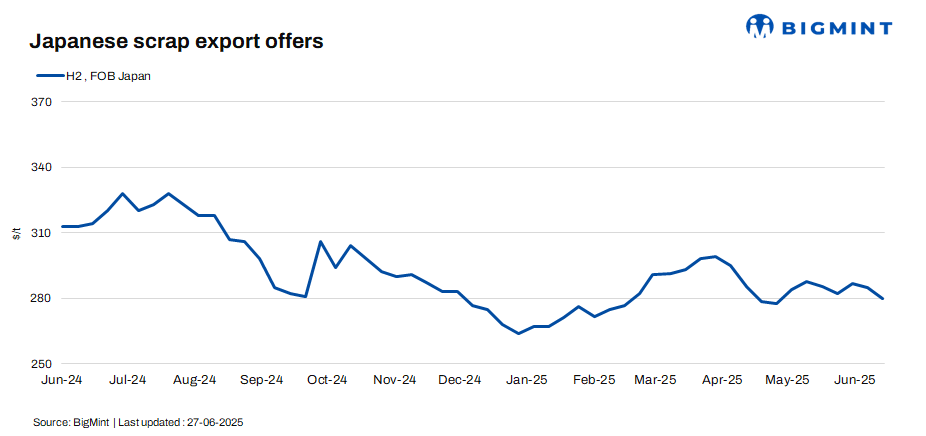

Japanese H2 scrap export offers fell by $7/tonne (t) this week as buyers across key Asian markets retreated, pressured by seasonal demand weakness and rising trade risks. Offers to Vietnam slipped to $315-317/t CFR, while bids softened to around $310/t amid sluggish rebar demand and the onset of the rainy season. Bangladeshi buying remained limited, with offers heard near $340/t CFR but met with little interest.

Market participants cited growing caution among suppliers, driven by JPY’s volatility and geopolitical headwinds. “The currency swings are making it harder to quote confidently,” a Tokyo-based trader said, noting that some exporters have paused transactions. Sentiment was further dampened by concerns over US tariff measures, including a potential 25% duty on Japanese automobiles from 9 July and possible extensions to steel products.

BigMint’s weekly assessed FOB Tokyo Bay prices of H2 scrap were down by JPY 1,000/t ($7/t) w-o-w to JPY 40,500/t ($280/t), reflecting the softer outlook. “We are in a wait-and-watch phase,” another trader added, pointing to limited trade activity and cautious pricing behaviour.

Importer’s market updates

Vietnam: Vietnam’s imported scrap market remained subdued this week, with buyers showing little appetite amid seasonal demand slowdown and falling steel margins. Offers for Japanese H2 declined to $315-317/t CFR, while bids slipped to around $310/t as rebar consumption weakened under the rainy season.

“Buyers are cautious and not aggressive,” a local trader said, adding that some mills preferred cheaper containerised HMS cargoes over bulk H2.

Deep-sea offers from the US also fell, with HMS 80:20 heard at $345/t CFR, though bids lagged at $335/t. Market participants expect limited activity ahead, citing weak downstream demand and wide bid-offer spreads.

Taiwan: Taiwan’s imported scrap market weakened further this week, with containerised US-origin HMS 80:20 prices slipping to a six-week low of $290-293/t CFR. Mills remained largely inactive, limiting scrap restocking amid poor rebar demand and the seasonal monsoon slowdown. “Scrap appetite is low, and bids are not improving,” a buyer said.

Domestic giant Feng Hsin slashed rebar and local scrap prices, citing global scrap softness and weak construction demand. Bulk Japanese H1:H2 offers held firm at $315-323/t CFR, but few deals were heard. With Turkish scrap prices still low and no freight cost impact yet from Middle East tensions, Taiwan’s scrap market is expected to stay under pressure in the near term.

South Korea: South Korea’s imported scrap market remained subdued this week, with mills raising inventories ahead of planned maintenance shutdowns in July. Cumulative scrap stockpiles at eight major steelmakers rose 8% w-o-w to 793,000 t, led by a 15% jump in the central region as import arrivals outpaced consumption.

“Daily arrivals are high, but mills are preparing for reduced operations next month,” a source said.

Despite the stockpiling, demand remained lacklustre as several mills, including Dongkuk and Daehan, plan production halts. Expecting lower scrap usage in the coming weeks, mills such as SeAH Changwon and Korea Special Steel cut domestic scrap purchase prices by KRW 10/t ($7/t), reinforcing a bearish tone in the market.

Outlook

Japanese H2 scrap export offers are likely to face further downward pressure amid weak buying interest from key Asian importers, currency volatility, and trade policy uncertainty. With Vietnam, Taiwan, and South Korea showing limited appetite due to seasonal demand slowdown and upcoming mill maintenance, sellers may need to adjust pricing further to stimulate trade.

Leave a Reply