- Appreciation of JPY pressures Japan’s FAS prices

- Kanto tender next week may provide price clarity

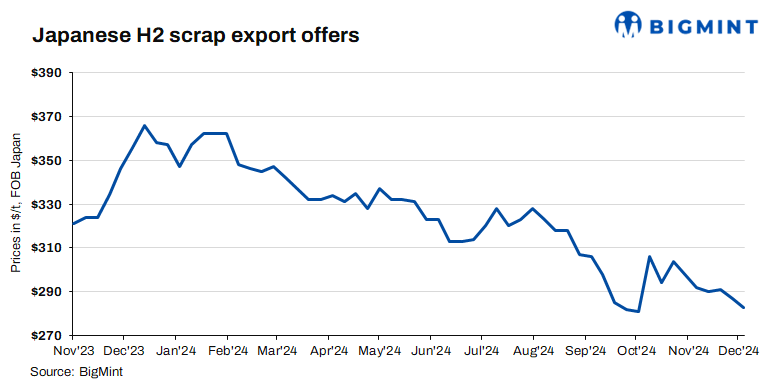

Japanese H2 scrap export offers fell by $3/t this week due to a combination of factors, including low demand, high freights, and bearish market sentiments. Vietnam, a key buyer, saw sluggish interest, as mills awaited greater price clarity amid reduced domestic construction activity and financial constraints. The appreciation of the JPY further pressured Japan’s FAS prices, while competitive alternatives and risks with the procurement of deep-sea cargoes shifted buyer interest away from the country.

BigMint’s weekly assessment placed Japanese H2 export offers at JPY 42,500/tonne (t) (283/t) FOB Tokyo Bay, down by JPY 500/t ($3/t) in comparison with JPY 43,000/t ($286/t) FOB in the previous week.

The average H2 price across three regions – Kanto, Kansai, and Chubu – remained stable at JPY 38,200/t ($254/t) in the first week of December, as per the Japan Iron and Steel Association. Regional prices also held steady, with Kanto at JPY 41,500/t ($276/t), Kansai at JPY 37,000/t ($246/t), and Chubu at JPY 36,200/t ($240), showing no change from the previous week.

Other market updates

Vietnam: Vietnam’s imported scrap market remained quiet, as weak demand, cautious sentiment, and financial challenges limited transactions. Japanese H2 offers stood at $335/t CFR, with bids at $325/t CFR. US-origin deep-sea HMS 80:20 offers were heard at $360/t CFR, but high costs and procurement risks kept buyers away. The domestic market also showed bearish trends, with prices falling to VND 8,100/t ($318/t) in the southern region amid sluggish construction activity and financial constraints.

Mills avoided fresh bookings due to the unclear price outlook. Although Japanese scrap was available at competitive rates due to a weak JPY, overall demand was too subdued for significant uptake. With buyers largely on the sidelines and no urgency to restock, the market remained in a wait-and-watch mode, reflecting broader bearish sentiments.

South Korea: South Korea’s imported scrap market remained subdued today, reflecting cautious sentiment. Offers for Japanese HS scrap hovered at around JPY 50,000/t ($334/t) CFR Korea, and shredded was quoted at JPY 48,000/t ($320/t). Meanwhile, mills raised bids for Shindachi Bara to JPY 49,000/t ($327/t). Despite competitive offers, mills refrained from significant bookings due to bearish market expectations and weak downstream demand.

Domestically, scrap prices remained stable but are set to decline, with major steelmakers such as Hyundai and Dongkuk Steel announcing reductions of KRW 10,000-15,000/t ($7-10/t) starting next week. Domestic inventories fell 3.8% w-o-w, amid reduced production in response to sluggish demand. Downstream, rebar sales remained weak, keeping operating ratios low at 30-40%. Seasonal factors and lacklustre construction activity further dampened sentiment, with market participants bracing for continued downward pressure on prices in the near term.

Taiwan: Taiwan’s imported scrap market remained under pressure today, with limited buying interest amid weak finished steel fundamentals. Offers for containerised HMS (80:20) from the US softened to $300-305/t CFR, down $5/t w-o-w, with unconfirmed rumours of deals at $295/t CFR. Japanese bulk H1/H2 offers also fell to $315-320/t CFR, but no trades were reported.

Domestically, Feng Hsin Steel reduced rebar and local scrap purchase prices by TWD 200/t ($6/t). This follows declining global scrap prices and sluggish demand and reflects the market’s continued battle with bearish sentiments amid broader challenges in the steel sector.

Outlook

Japanese H2 offers are likely to remain under pressure due to limited demand, high freights, and a bearish global market. Vietnam and South Korea’s sluggish construction activities and financial challenges suggest that scrap demand will not recover anytime soon, despite attractive pricing. In Taiwan, softened offers and domestic price reductions highlight the continued weakness in steel fundamentals. The overall market outlook remains bearish, with buyers staying cautious amid uncertain price trends and weak downstream demand. The upcoming Kanto tender next week may provide some clarity.

Leave a Reply