- Tokyo Steel reduces bids amid rising scrap inventories

- South Korea, Taiwan buyers wary amid seasonal slowdown

Japan’s H2 ferrous scrap export market weakened in early July as a stronger JPY dampened competitiveness. Offers to Vietnam ranged between $313-320/tonne (t) CFR, but bids remained lower at around $313-315/t amid soft demand and a weakening VND. Traders highlighted limited buying interest, with Asian mills opting for conservative procurement due to the monsoon steel demand lull and summer maintenance.

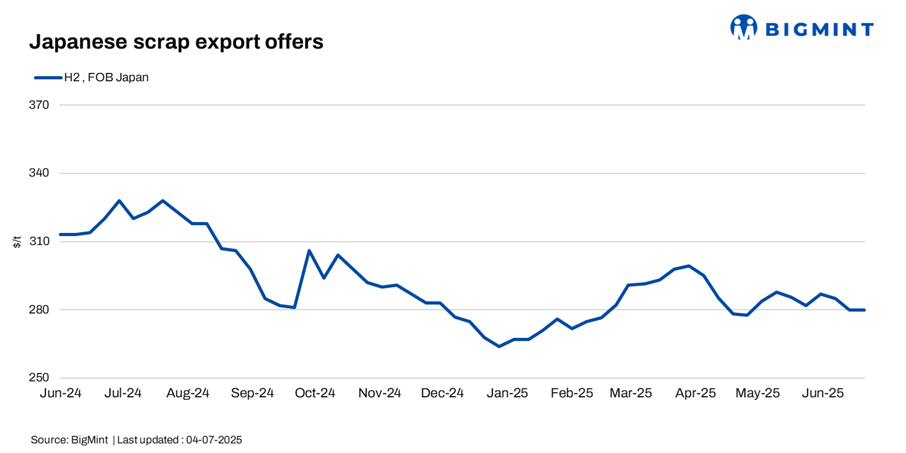

BigMint’s weekly assessment placed H2 scrap down by JPY 100/t ($0.7/t) w-o-w at JPY 40,400/t ($280/t) FOB Tokyo Bay.

Tokyo Steel cut bids by JPY 500/t ($3/t) at major plants, citing rising inventories. Revised H2 prices stood at JPY 40,500/t ($281/t) in Tahara; JPY 40,000/t ($278/t) in Nagoya, Okayama, and Kansai; and JPY 38,000/t ($264/t) in Takamatsu.

Importer’s market updates

Vietnam: Vietnam’s imported scrap market remained sluggish, with buyers maintaining a cautious stance amid currency fluctuations and subdued steel demand. Japanese H2 scrap offers ranged between $313-320/t CFR, but bids stayed lower at $313-315/t, signalling weak buying appetite. Traders pointed to the ongoing rainy season and a weakening Vietnamese dong as key factors dampening sentiment.

Bulk HMS 80:20 offers from the US held steady at $345/t CFR, while bids hovered at $335/t CFR. Australian-origin offers were also heard at $335/t CFR and above, though no firm bids emerged. Buyers reportedly preferred smaller lots to hedge against market volatility.

South Korea: South Korea’s imported scrap market remained weak, as mills reduced purchase prices and focused on inventory rotation over stockpiling. Scrap prices turned bearish from late-June amid production cuts, slowing demand, and a drive to secure liquidity. Major mills such as Taewoong, SeAH Changwon, and Korea Special Steel cut purchase prices by KRW 10,000/t ($7/t) across most grades.

Ferrous scrap inventories rose 15% from mid-June lows to 822,000 t by the first week of July, with central region mills leading the build-up in anticipation of summer production cuts. While inflows continue to outpace consumption, traders remain cautious amid the risk of temporary shortages during the upcoming rainy season.

Taiwan: Taiwan’s imported scrap market remained under pressure amid weak rebar sales and a seasonal construction lull. US-origin HMS 80:20 containerised scrap was assessed at $285-290/t CFR, down $5-8/t from earlier in the week. Japanese H2 continued to decline to $311/t CFR. Mills remained cautious, seeking lower prices as demand from end-users stayed muted.

Feng Hsin Steel cut rebar list prices by TWD 300/t ($10/t) but kept domestic scrap unchanged after a recent TWD 200/t cut. Import volumes also dropped sharply in May, reflecting reduced buying appetite.

Outlook

Japanese H2 scrap export offers are likely to stay soft amid a firm JPY, muted demand from key buyers in Vietnam, South Korea, and Taiwan, and seasonal slowdowns. With mills focusing on inventory control and cost management during summer maintenance, a near-term recovery in prices appears unlikely. Market sentiment remains broadly bearish.

Leave a Reply