- Strong demand supports ADC12 prices amid tight scrap supply

- LME aluminium tops $2,600/t in early-July, supporting scrap tags

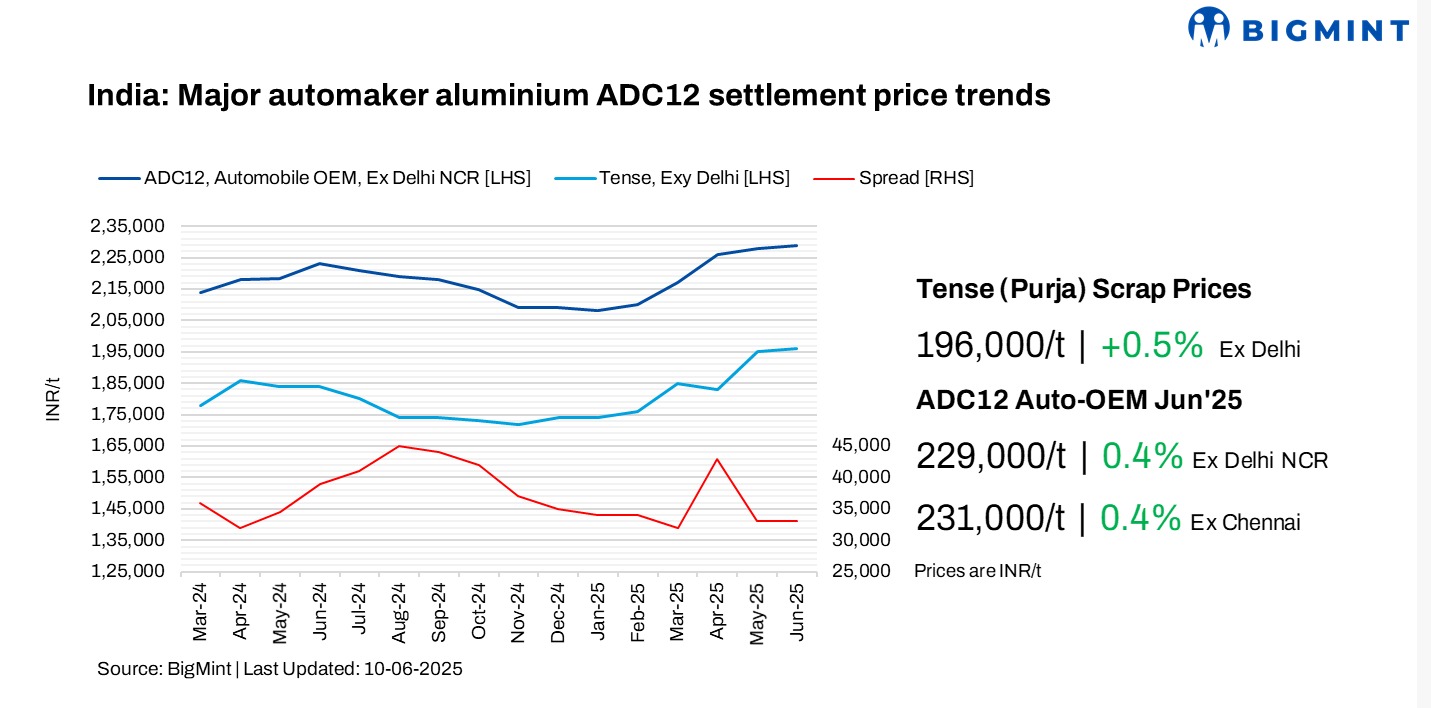

India’s secondary aluminium market witnessed a slight rise in alloy ingot prices through June 2025, supported by strong demand from die-casting and auto component manufacturers, along with elevated input costs.

BigMint’s assessment for June placed OEM-approved ADC12 at INR 229,000/tonne (t) in Delhi and INR 231,000/t in Chennai, marking an increase of up to INR 1,000/t from May.

A major Indian automaker increased its ADC12 settlement price by INR 2,150/t m-o-m to INR 228,900/t for July deliveries – the highest since May 2022. This surge was attributed to strong global scrap prices and a decline in alloy imports.

Price negotiations for July – offers high, but buyer resistance grows

Despite sellers quoting high ADC12 prices of INR 235,000-236,000/t, OEMs began pushing back. North India-based buyers targeted INR 230,000-233,000/t, while southern buyers negotiated at around INR 232,000-234,000/t.

An OEM in the southern region said, “Sellers are quoting up to INR 235,000-236,000/t for ADC12 with 30-day credit, but most negotiations are centred around INR 232,000-234,000/t. Many OEMs are not willing to exceed INR 234,000/t for July settlements.”

The scrap-to-ADC12 spread in early July widened slightly by INR 2,500/t m-o-m to INR 33,000-35,000/t due to lower bids from buyers but higher Tense scrap costs in Delhi and Chennai amid shortages.

An alloy producer based in the north observed, “Current Tense scrap prices are at INR 197,000/t, but sellers are demanding INR 203,000/t, indicating a firm stance amid tight availability. With a +INR 30,000/t conversion premium, indicative ADC12 prices are being quoted around INR 233,000/t.”

Raw material trends

Monthly average aluminium prices on the London Metal Exchange (LME) stood at $2,516/t in June, reflecting an increase of nearly 3% m-o-m. Prices were range-bound at the beginning of the month. However, towards the fourth week, LME prices hit a 3-month high, reaching $2,570-80/t, as the US airstrikes on Iran’s nuclear facilities raised the prospect of higher energy rates and disruptions to shipments of the metal from the Middle East.

Following this increase in the LME levels, offers for imported as well as domestic aluminium scrap saw an increase during the same period.

Imported aluminium scrap prices rose significantly in June. US-origin Tense rose by $25/t m-o-m to $1,990/t, while UK-origin Wheels increased by $40/t to $2,480/t. LME aluminium three-month contracts also firmed up by $40/t m-o-m to $2,520/t. However, domestic Tense prices saw an INR 1,000/t m-o-m increase, with BigMint’s June-end assessment at INR 196,000/t in Delhi and INR 197,000/t in Chennai.

Sentiment remained bullish due to rising global tags and supply tightness in previous months. Silicon 553 prices from China dropped $150/t m-o-m to $1,200/t CFR Mundra.

Tracking India’s scrap, ingot import flow in 5MCY’25

In 5MCY’25, India’s aluminium scrap imports surged by 13% to 721,862 t from 641,435 t in 5MCY’24.

The US continued as the leading supplier, exporting 132,101 t to India, reflecting a 12% decrease from 5MCY’24, primarily due to the strong domestic demand for scrap in the US.

India’s ADC12 alloy market witnessed a dramatic contraction in imports during the first five months of 2025 (5MCY’25), with inbound volumes plunging by 92% y-o-y. Total ADC12 imports stood at just 751 t, down sharply from 9,963 t in 5MCY’24.

The most significant decline came from Malaysia, which had historically been India’s top ADC12 supplier. Imports from Malaysia dropped by 95% to 450 t from 8,398 t a year earlier. This was primarily due to delays in obtaining Bureau of Indian Standards (BIS) certifications, despite the existing Free Trade Agreement (FTA) between the two countries.

Auto sector performance

Overall automobile retail sales saw a 4% y-o-y increase in the first five months of 2025, to 10.8 million units. Out of the total, retail passenger vehicle (PV) sales grew in 5MCY’25 to around 1.7 million units. Aligning with rising sales, production also saw a 4% y-o-y increase in 5MCY’25, reaching 12.2 million units compared to 11.7 million units in 5MCY’24.

Looking at the monthly scenario, retail sales dipped 3% m-o-m to 2.21 million units. Out of the total, retail PV sales fell by 9,694 units y-o-y in May to around 302,214 units, also marking a decline from April 2025. High dealer inventories and increased discounts reflected subdued demand. The India-Pakistan conflict and heavy rains impacted sales, especially in northern India.

Maruti Suzuki highlighted a 6% y-o-y drop in May dispatches, citing supply calibration amid weak urban demand, though rural demand stayed strong.

Outlook – Will ADC12 prices hold in July?

Alloy prices strengthened in June and are expected to remain elevated through July across both north and south India, driven by rising scrap costs domestically and internationally. The uptrend is also supported by LME aluminium prices, which surpassed the $2,600/t mark in early July, amid ongoing geopolitical tensions and tight scrap availability. These factors continue to lend strong support to ADC12 pricing.

Leave a Reply