- Vietnam leads on strong demand, mills’ expansions

- Korea volumes fall amid focus on domestic scrap

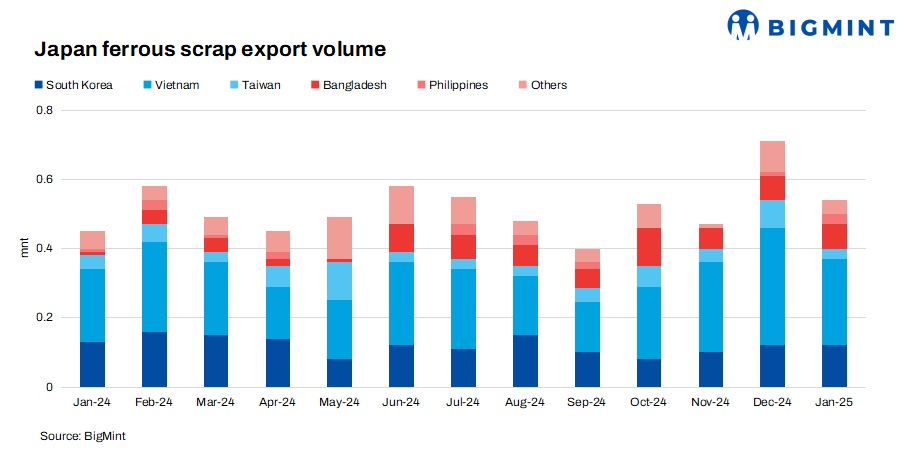

Japan’s total ferrous scrap exports in calendar year 2024 (CY’24) fell to their two-year lows at 6.29 million tonnes (mnt), marking a 5% y-o-y decline from 6.59 mnt in CY’23. The drop reflects overall weaker demand from key importing nations, particularly South Korea and Taiwan.

The steepest y-o-y decline in a month was seen in January 2024, of 21%, to 440,000 t from 560,000 t in the same month in CY’23. In contrast, December 2024 recorded the largest rebound, rising by 22% y-o-y to 710,000 t compared to 580,000 t in the same month CY’23, signalling renewed demand momentum at the year-end.

In January 2025, Japan’s scrap exports fell to 540,000 t, down 24% m-o-m from 710,000 t in December 2024. However, on a y-o-y basis, exports rose 23% compared to 440,000 t in January 2024, indicating a stronger start to the year.

Other updates

Crude steel production: Japan’s crude steel production in CY’24 dropped to 84.01 mnts, down 3% y-o-y from 87.01 mnt in CY’23.

Japan pig iron production: Pig iron production declined by 3% y-o-y in CY’24 to 61.03 mnt from 63.04 mnt in CY’23.

Average H2 scrap export prices:

- In CY’24, average scrap export prices stood at $329/t, down 4% ($13/t) from $342/t in CY’23, FOB Japan.

Country-wise break-down

Vietnam: In CY’24, Vietnam emerged as Japan’s largest ferrous scrap buyer, with imports rising by 55% y-o-y to 2.6 mnt from 1.68 mnt in CY’23.

The sharp increase was supported by strong construction activity and expanding steelmaking capacity from major mills.

Growing adoption of EAF technology among Vietnamese steelmakers over the blast furnace route further boosted demand for imported scrap, especially for its consistent quality and reliable supply chain.

South Korea: Exports dropped sharply by 43% y-o-y to 1.46 mnt from 2.54 mnt in CY’23.

The decline was primarily due to subdued domestic steel demand in South Korea, increased reliance on locally sourced scrap, and a strategic shift by Korean mills toward more cost-effective alternatives.

Additionally, firm Japanese FOB prices (in H1) and elevated logistics costs made Japanese scrap less competitive, prompting buyers to explore other regional and domestic sources.

Taiwan: Scrap exports to Taiwan fell by 33% y-o-y to 620,000 t in CY’24 from 920,000 t in CY’23.

The reduction is attributed to Taiwanese buyers shifting away from Japanese-origin scrap due to a drop in containerised scrap prices from the US West Coast. Additionally, weak domestic steel demand in Taiwan and low-cost billet offers from China led buyers to limit their ferrous scrap imports.

Bangladesh: This country saw a modest 19% increase in imports, rising to 620,000 t in CY’24 from 520,000 t in CY’23.

Despite a sluggish market, especially in the Japanese H2 segment, the increase in import volume was largely driven by strong buying from financially stable Chattogram mills, followed by prompt shipment advantage from nearby regions like East Asian countries, which had better access to letters of credit (LC) facilities despite economic uncertainty.

Leave a Reply