- India’s leading coil maker hikes 300 series tags

- Nickel prices surge on China’s higher SS output

Domestic stainless steel finished flat prices in India increased w-o-w, following a hike in tags by a major coil manufacturer, attributed to rising raw material costs. However, long product prices remained stable w-o-w. Notably, demand was subdued due to the upcoming Holi festival.

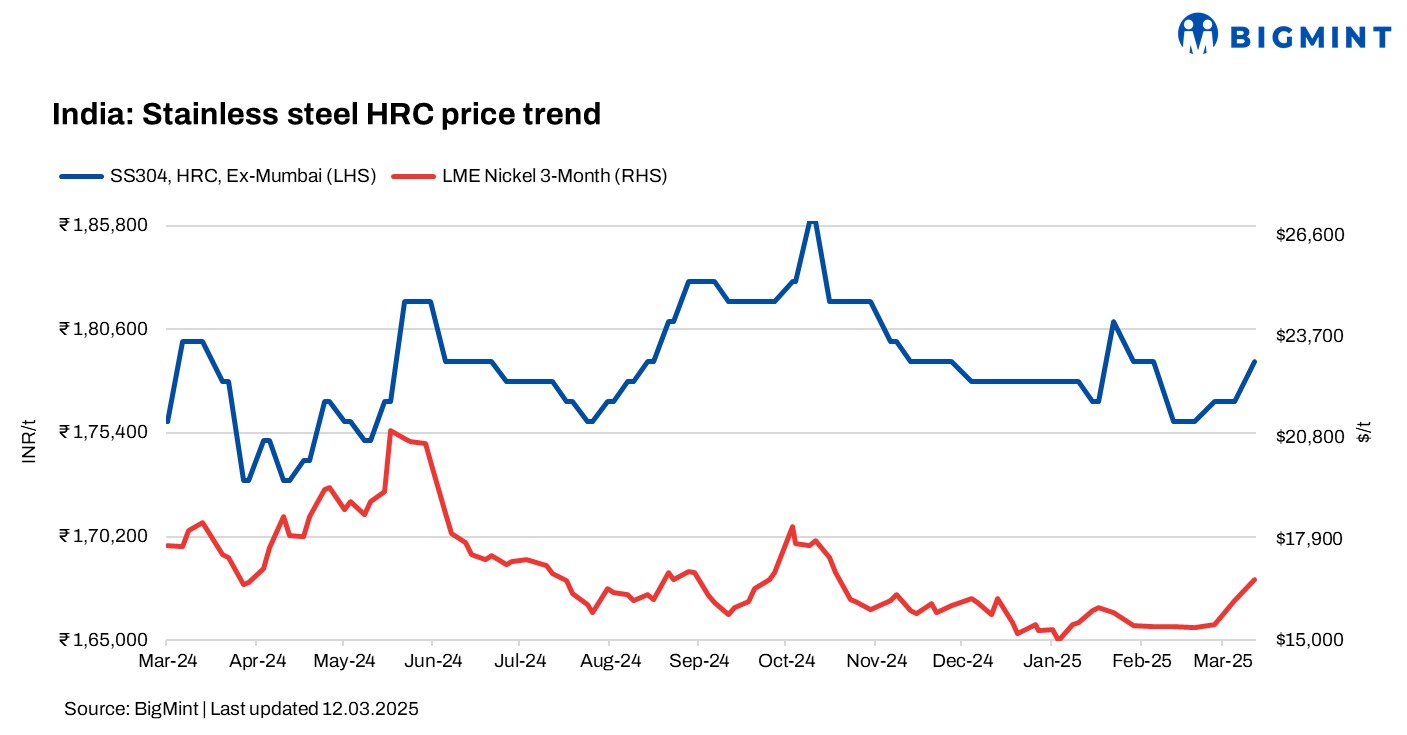

BigMint’s benchmark assessment for stainless steel (304 series) hot-rolled coils (HRCs) stood at INR 179,000/tonne (t), up by INR 2,000/t w-o-w, while 304L (25-100 mm) black round bars remained steady w-o-w at INR 160,000/t, both ex-Mumbai.

LME nickel, Asian NPI rise w-o-w

At the time of reporting, three-month London Metal Exchange (LME) nickel prices stood at $16,750/t, reflecting an increase of over 3.5% from last week’s $16,130/t. Nickel stocks in LME-registered warehouses inched up by 2% to 199,308 t compared to 194,420 t in the previous week.

Nickel prices have surged recently, driven by China’s increased stainless steel production in February, which boosted market sentiment. February 2025 saw a 0.1% m-o-m and 15% y-o-y rise in China’s stainless steel output. Additionally, the Indonesian government has proposed raising royalties for operators across multiple commodities, including nickel, leading to expectations of higher prices of the same from the region.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) also witnessed an increase of RMB 10/mtu ($1/mtu) w-o-w to RMB 998/mtu ($137/mtu). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $119/mtu, up by $2/mtu w-o-w.

Finished flats prices rise w-o-w

As per market participants, prices of flat products, particularly the 300 series, increased, as raw material costs rose and a major coil maker hiked its tags. This increase occurred despite sluggish market activity.

Meanwhile, prices of 316 HRCs and cold-rolled coils (CRCs) remained supported amid a supply shortage, as heard from market participants.

As per BigMint’s assessment, tags of 316 HRCs rose by INR 2,500/t w-o-w to INR 323,000-325,000/t ex-Mumbai.

A source stated, “Domestic demand for finished stainless steel remains weak, with little expectation of improvement this month. As the Holi festival approaches and the financial year-end nears, major players are likely to focus on book closing, which may limit market activity. While nickel prices continue their uptrend, potentially impacting mills’ offer prices, the response of the domestic market in the coming days remains uncertain.“

However, another source stated that demand for 200 series and 400 series coils remained steady.

Longs maintain stability w-o-w

BigMint’s assessment of SS 316L (25-100 mm) black round bars stood at INR 269,000-271,000/t ex-Mumbai. Prices of SS 316L (25-100 mm) bright bars stood at INR 287,000-289,000/t ex-Mumbai, stable w-o-w.

A mill source noted, “Demand for finished products is currently weak, and we do not foresee any improvement this month. Most major mills have maintained stable offers for argon oxygen decarburisation (AOD) grade material.”

Prices of SS 304 wire rods (5-16 mm) were at INR 155,000/t, ex-Mumbai, unchanged w-o-w.

Chinese stainless steel prices rise

In China, domestic prices of 304-grade stainless steel CRCs were at RMB 13,950/t ($1,926/t) exw, reflecting a w-o-w increase of RMB 100/t ($14/t). FOB prices of 304-grade CRCs stood at $1,890/t.

Raw materials overview

Ferro molybdenum: Indian ferro molybdenum prices saw a drop of INR 29,000/t ($332/t) w-o-w on 12 March in comparison to the previous assessment on 5 March. Prices edged down, as market activities slowed down during the previous week.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 101,350/t ($1,162/t) exw-Jajpur, range-bound as compared to previous week.

Additionally, India’s chrome ore dispatches surged by 32% to 253,290 t in January 2025, from 192,011 t in December 2024. Odisha Mining Corporation (OMC) led the increase with a 56% m-o-m rise, dispatching 100,364 t in January. Tata Steel’s dispatches also climbed 63% to 53,499 t, while Indian Metals and Ferro Alloys (IMFA) registered a 16% increase to 63,248 t. However, dispatches from Vedanta-Ferro Alloys Corporation (FACOR) saw a drop of 36% m-o-m to 11,521 t in January.

Outlook

Demand for finished goods remains subdued, with limited improvement expected this month due to the Holi festival and fiscal year-end. Transaction volumes are likely to be restricted to essential needs, impacting market activity.

Leave a Reply