- Portside and seaborne iron ore trades improve weekly

- Simandou supply growth adds long-term market pressure

Mysteel Global: Imported iron ore prices in China are facing renewed downward pressure as the stricter measures rolled out by the world’s largest ore buyer to address overcapacity in its steel industry point to further constraints on the country’s medium- to long-term demand for the steelmaking ingredient, Mysteel Global notes.

To add new facilities, since 2015 Chinese steelmakers have needed to meet the country’s “capacity swap” regulations which demand that whenever new iron- or steelmaking capacity is introduced, old facilities in operation at the time need to be stopped and eventually scrapped.

On Monday, China’s Ministry of Industry and Information Technology (MIIT) issued a revised version of its steel capacity swap guidelines, aiming at stricter replacement requirements, more targeted policy incentives, and stronger oversight mechanisms, as reported.

Particularly, the new guidelines stipulate that the nationwide replacement ratio for both ironmaking and steelmaking capacity must be no less than 1.5:1 – meaning that a firm wanting to build a 10 million tonnes/year steel plant must scrap the equivalent of 15 million t/y of outdated or surplus capacity – while the ratio for projects involving mergers and acquisitions has been raised to no less than 1.25:1.

The tougher rules reflect the central government’s determined efforts to close loopholes that have allowed surplus steel capacity to persist – and capacity to even expand – despite oversupply and weak profits, according to industry insiders. While the impact on actual steel production is still yet to be seen, sentiment has already turned slightly negative for iron ore and other feed materials following the release of the guidelines.

In the derivatives market, the most-traded iron ore contract on the Dalian Commodity Exchange (DCE) for September delivery recorded a loss of 1.1% during Monday’s daytime trading session, and it closed Tuesday lower at Yuan 798.5/tonne ($117.4/t), marking its lowest level so far in May.

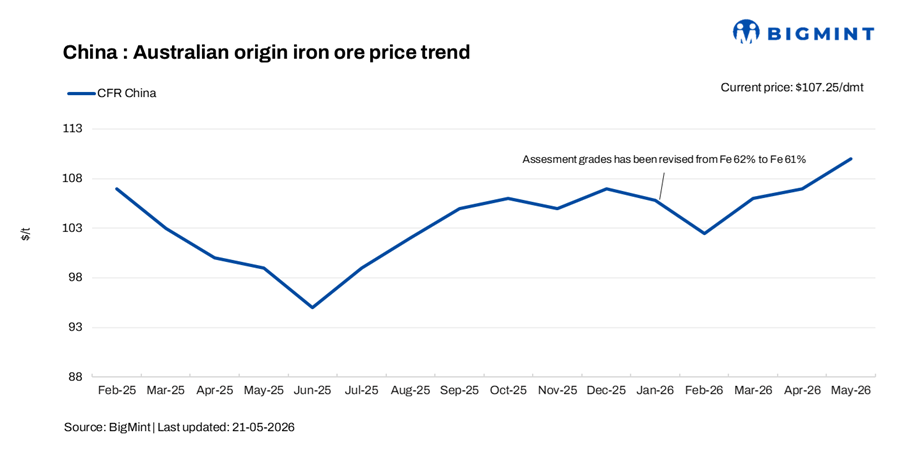

By Tuesday, Mysteel SEADEX 61% Australian Fines had slipped $2.5/dmt on week to $107.8/dmt CFR Qingdao, while Mysteel Portside 61% MNPJ Index also declined by Yuan 21.6/dmt on week to Yuan 844.8/dmt FOT and including the 13% VAT.

In the short term, prices for imported iron ore in China are expected to remain underpinned by steady demand from domestic steelmakers as they maintain high hot metal output amid improved profit margins.

During the first two days of this week, transaction volumes of seaborne iron ore cargoes in China jumped 13.9% on week, and the traded volume at Chinese ports also leapt 22.9% from the same period last week, according to Mysteel’s tracking data.

In the medium to long term however, downside pressure on iron ore is set to build, sources say. They cite contracting steel demand in China, against expanding output from major mainstream miners and additional supply from the massive Simandou project in Guinea in West Africa in which Chinese firms including China Baowu Steel Group are major shareholders. The first commercial shipment of Simandou ore arrived in China in mid-January, as reported.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply