- Project-led consumption remains largely absent

- Fresh enquiries remain limited across regions

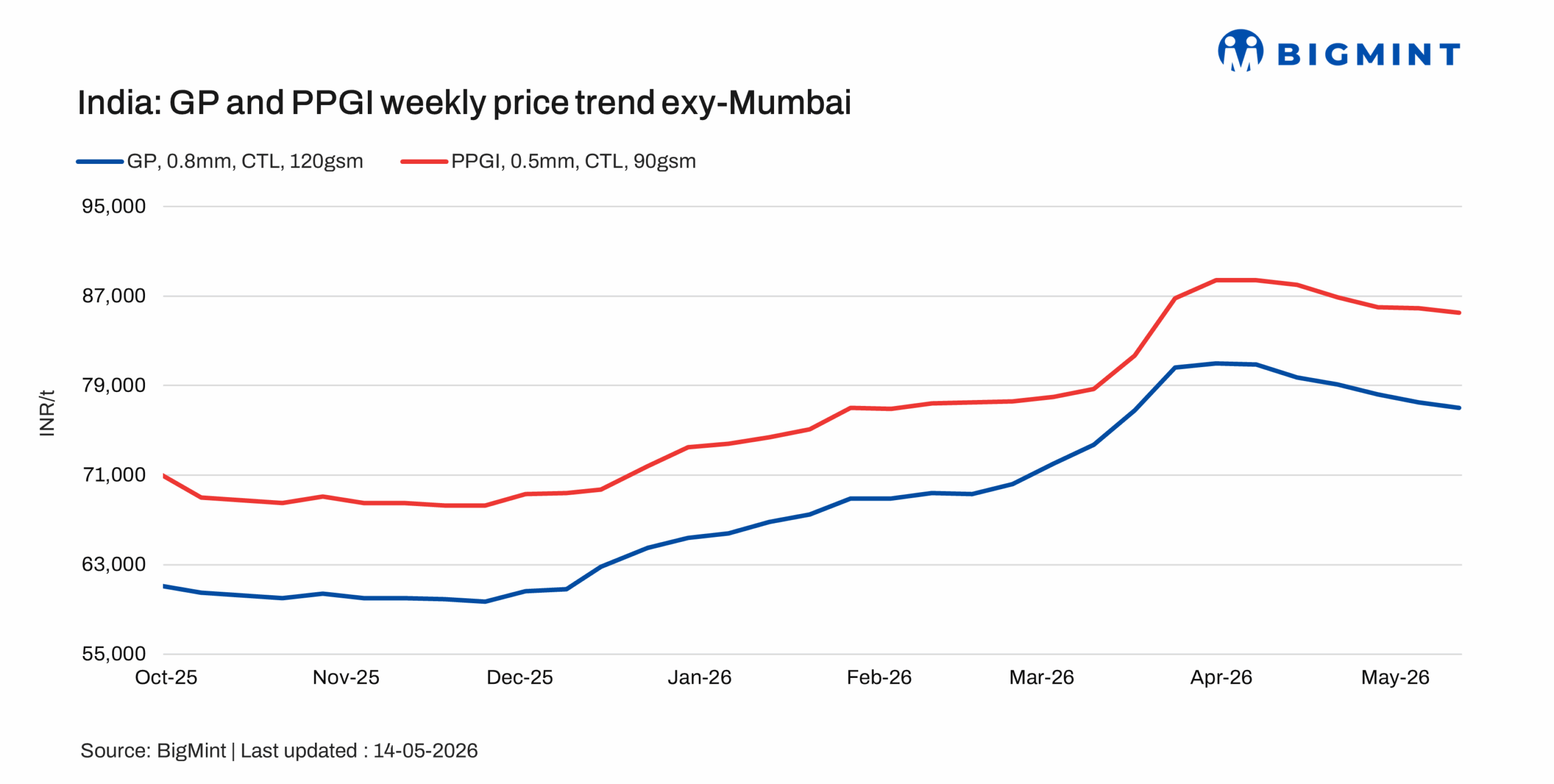

Indian coated flat steel prices declined further by INR 500-1,300/t w-o-w as of 21 May 2026, as poor demand conditions continued to weigh on the market. Trading activity across major consuming regions remained subdued, with low enquiry levels and limited bookings reported during the assessment period. Buyers continued to procure material only for immediate requirements, reflecting cautious market sentiment.

Ample inventory availability across the supply chain and competitive spot offers continued to exert pressure on prices, while labour shortages in downstream segments further impacted raw material demand. Market chatter suggests that the current weak demand conditions and subdued sentiment are likely to prevail, keeping the overall sentiments bearish.

Price Update:

Galvanised plain (GP) coil (exy-Mumbai, India; 0.8mm / CTL, 120 GSM, IS 277) was assessed at INR 77,000/t, down by INR 500/t w-o-w, amid continued weak demand conditions. Tradable offers were heard in the range of INR 76,500-78,500/t.

Pre-painted galvanised iron (PPGI) (exy-Mumbai, India; 0.5mm / CTL, 90 GSM, IS 14246) was assessed at INR 85,500/t, down by INR 400/t w-o-w. Offers were reported in the range of INR 85,000-86,000/t, while bookings remained slow amid subdued market activity.

Galvalume/bare galvalume (BGL) (exy-Mumbai, India; 0.5mm / CTL, 1220mm, AZ150) was assessed at INR 89,300/t, stable w-o-w. Offers were indicated in the range of INR 88,500-90,000/t, while trading activity remained moderate.

Raw material prices

India’s zinc ingot (99.995%) prices increased sharply w-o-w by INR 11,900/t to INR 373,800/t ex-Delhi on 19 May 2026, supported by stronger global prices and aggressive producer-led hikes, although downstream demand continued to remain largely cautious. Market participants largely restricted procurement to immediate requirements amid subdued consumption trends.

The domestic market continued to track Hindustan Zinc Limited, which increased its zinc ingot prices by INR 9,200/t on 18 May to INR 382,600/t, in line with elevated LME zinc prices and firm global sentiment. The company also raised its lead ingot prices by INR 400/t to INR 228,100/t during the same revision.

BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) held stable w-o-w at INR 58,700/t ($608/t) as of 19 May.

However, CRC (IS513, Gr O, 0.9 mm/CTL) prices decreased by INR 500/t ($5/t) to INR 66,000/t ($683/t) on 19 May from INR 66,500/t ($688/t) on 12 May. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market update

Market sentiment across the northern, western, and southern flat steel markets remained dull during the week, as prices continued to decline further amid weak demand conditions. Trading activity stayed slow across major regions, with market participants reporting limited fresh enquiries and subdued spot bookings. The slowdown was mainly attributed to the absence of major project-related demand, cautious buying sentiment, and relatively high price levels, which continued to impact procurement activity.

Demand for galvanised plain (GP) products remained weak across most regions, while the pre-painted galvanised iron (PPGI) segment witnessed comparatively better movement in select markets. However, overall regional demand for coated flat steel products continued to remain sluggish.

Inventory levels across the supply chain remained elevated, which further weighed on spot market activity and discouraged aggressive restocking by buyers. In addition, labour shortages persisted in certain regions, affecting downstream processing activity and overall consumption trends.

On the other hand, galvalume/bare galvalume (BGL) prices remained relatively stable, supported by comparatively lower inventory availability and limited spot material in some markets.

Outlook

Indian coated flat steel market sentiment is expected to remain weak in the coming weeks, as there are currently no signs of meaningful demand recovery across major regions. Trading activity is likely to stay slow, with buyers continuing to procure material only for immediate requirements amid cautious market sentiment.

Demand for GP products is expected to remain subdued, while PPGI movement may also stay limited despite some regional enquiries. Overall, market participants expect weak demand conditions and sluggish market activity to persist in the coming week.

Leave a Reply