- Freight activity strengthens across basins amid mixed routes

- BDI surges on Capesize demand; freight outlook remains firm

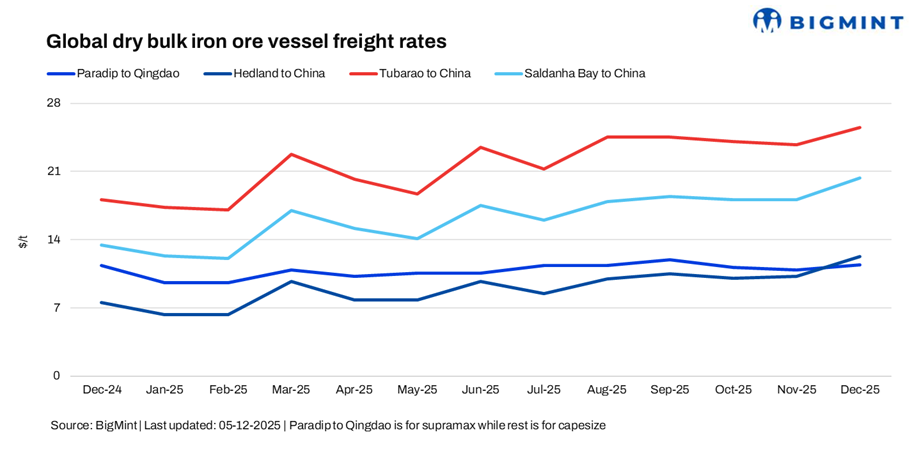

Iron ore freight rates increased across key Capesize and Supramax routes in the week ended 5 December, supported by strong Chinese demand, rising chartering activity, and tightening vessel supply. Market sentiment remained upbeat in both the Atlantic and Pacific basins, as mills continued winter restocking while forward demand visibility improved. Increased cargo inquiries and firm fixture momentum underpinned overall freight resilience.

Capesize market surges on strong charters and limited tonnage

Capesize rates surged this week amid a sharp uptick in charterer demand and constrained vessel availability. The Australia-China route continued to firm, driven by improving activity in Western Australia and sustained restocking demand. The South Africa-China route also saw strong gains backed by tight tonnage lists and a jump in fresh fixtures. The Brazil-China long-haul market posted a notable w-o-w upswing as inquiry levels and confidence rebounded after recent softness.

Indian Ocean Supramax market maintains upward momentum

The Supramax market in the Indian Ocean held firm, with freight on the India (Paradip)-China route extending gains. Steady minor bulk volumes, balanced vessel supply and demand, and healthy chartering interest continue to keep rates supported.

Freight strong, but mixed bunkers and winter risks keep caution

Despite overall freight strength, market caution lingers as bunker prices remain mixed and macro-outlook uncertainty builds ahead of peak winter. While freight fundamentals continue to tighten, some operators remain conservative in forward positioning due to fluctuating demand expectations and persistent operating cost pressure.

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China rose by $0.3/t w-o-w to $11.6/dry metric tonne (dmt) on 5 December.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China inched up by $1.54/dmt w-o-w to $12.52/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments were up by $1.19/dmt w-o-w at $25.82/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao increased by $1.94/dmt w-o-w to $20.65/dmt.

Market highlights

- Baltic index continues its upward momentum w-o-w: The Baltic Exchange’s dry bulk index (BDI) rose 335 points this week to 2,815 as of 05 December. The Capesize segment led the gains with a sharp jump of 1,083 points to 5,319, while the Panamax index slipped by 99 points to 1,863 and the Supramax index inched up 4 points to 1,441. The overall strength was supported by elevated Capesize chartering demand and tightening tonnage availability, partially offset by softer sentiment in the Panamax market, while mid-size segments remained relatively stable.

- Brent crude oil futures decline w-o-w: Brent crude oil futures slipped marginally by around $0.02/barrel (bbl) w-o-w to $63.15/bbl on 04 December 2025 from $63.17/bbl on 27 November, as easing geopolitical concerns and persistent inventory builds continued to weigh on market sentiment.

- DCE iron ore futures dip w-o-w: Iron ore futures on the Dalian Commodity Exchange (Jan’26 contract) closed at RMB 785/t ($111/t) on 05 December, marking a w-o-w decrease of RMB 10/t ($1.4/t) amid weakening procurement appetite and cautious steel mill restocking ahead of winter demand uncertainties.

Outlook

Iron ore freight rates are expected to remain firm in the near term on the back of sustained Chinese demand, tightening vessel supply, and robust chartering momentum in the Pacific and Atlantic basins. Capesize sentiment remains upbeat as Australia and South Africa shipments continue to accelerate, while Brazil-China rates are likely to hold steady with a mild bullish bias. Supramax levels in the Indian Ocean are projected to stay supported by consistent minor bulk flows and balanced fleet positioning.

Leave a Reply