- Operational challenges in Sumatra impact supplies

- Indian demand active for low- and mid-CV coal cargoes

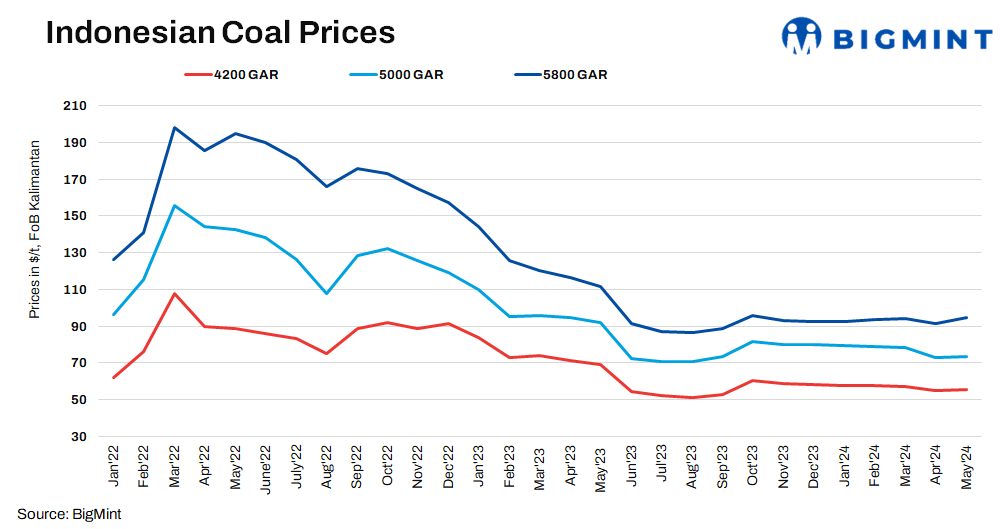

Indonesian thermal coal prices continued their uptrend last week. Prices of high-CV (5800 GAR) coal increased by $0.58/tonne (t), settling at $96.67/t. Indonesian mid-CV coal prices (4200 GAR) increased by $0.18/t to $56.43/t. Meanwhile, prices of low-CV (3400 GAR) coal increased by $0.14/t to $35.61/t. Prices mentioned are on FOB basis.

On the supply side in Indonesia, rain-related operational challenges persisted in Sumatra, resulting in fewer cargoes being offered from that region. However, production in the rest of Indonesia remained stable. Indonesian high-CV coal prices rose further due to limited availability of prompt-loading cargoes, with floods in parts of Sumatra and East Kalimantan supporting prices to some extent.

The scarcity of Indonesian high-CV coal led to increased offers. Pockets of demand for Indonesian high-CV demand were heard from Japan and Vietnam, which continued to somewhat support prices.

Demand in China increased as activities in some of China’s industrial sectors, including steel, improved after policymakers provided some stimulus to boost the property sector. These incentives helped create demand for high-CV coal from the cement and steel sectors.

According to market participants, Chinese imports of Indonesian coal increased in anticipation of further temperature rises. Buyers, especially stock-and-sale traders, are restocking in preparation for the expected rainy season. Southern China has been experiencing record-high rainfall this year which has weakened demand for coal-based electricity generation. However, the northern parts of the country are still quite sultry which is driving domestic coal prices in China and most enquiries are from northern China.

In India, demand fundamentals remained broadly unchanged, with power plants seeking low- to mid-CV coal due to the intense heatwave across the country. However, comfortable inventory levels at utilities have restricted the rise in bids. Limited buying interest was noted from the sponge iron and other industrial sectors.

Market participants reported fewer Indian enquiries for restocking last week due to the expected onset of rainfall in the first week of June and the completion of restocking activities. Buyers have adopted a wait-and-see approach for high-CV coal due to the disparity between bids and offers.

Decline in portside prices of Indonesian coal

Prices of 3400 GAR coal at Navlakhi Port stood at INR 5,200/t, while 4200 GAR at Kanlda Port was priced assessed at INR 6,350/t. This drop in prices can be attributed to sufficient stocks at power plants, leading to low enquiries and limited buying in India.

Outlook

In the coming weeks, it is expected that Indonesian coal prices may not increase further as restocking in India has come to an end. The arrival of monsoon in the first week of June, along with a drop in temperatures, will also reduce power demand. In China, rainfall starting in June is expected to affect demand. But if supply constraints worsen, the downtrend in prices may not continue.