- Firm Asian demand and DMO-led supply tightness support exports and HBA prices

- Higher RKAB output may lift supply, weak Indian demand limits near-term upside

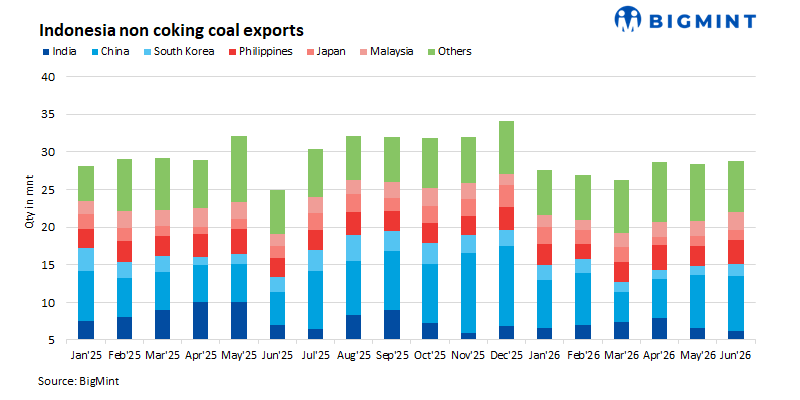

Indonesia’s non-coking coal exports increased by 1.8% m-o-m to 28.82 million tonnes (mnt) in June, compared with 28.32 mnt in May, while shipments were 15.6% higher year-on-year (y-o-y) than 24.93 mnt in June’25. The monthly improvement was supported by stronger demand from key Asian importers, particularly China and Southeast Asia, alongside improved cargo availability toward the end of the quarter.

Despite the recovery, H1’26 (January-June) exports declined 3.24% y-o-y to 166.59 mnt, reflecting the impact of tighter production controls and higher domestic coal allocation during the first half of the year. However, exports rebounded 6.12% quarter-on-quarter (q-o-q) to 85.77 mnt in Q2’26, indicating a gradual recovery in export activity.

Higher RKAB approval signals supply normalisation: Indonesia’s Ministry of Energy and Mineral Resources (ESDM) has approved over 600 mnt of coal production under the 2026 RKAB, up from 580 mnt approved in March, signalling a cautious easing of output restrictions to support exports while maintaining domestic energy security and long-term supply sustainability.

DMO policy restricts export availability: Indonesia’s Domestic Market Obligation (DMO) policy continued to constrain export availability as producers prioritised domestic supply to meet power sector demand. Limited RKAB allocations, stronger export economics, and delayed domestic payments kept spot coal availability tight despite higher production approvals.

China keeps buying momentum, Indian demand subdued

China maintained its position as the largest importer of Indonesian non-coking coal, with imports increasing 3.1% m-o-m to 7.32 mnt in Jun’26 and surging 65.43% y-o-y. During H1’26, exports to China climbed 17.80% to 36.83 mnt, while Q2 shipments increased 13.76% q-o-q to 19.60 mnt. Strong purchases were supported by stable coal-fired power generation, competitive Indonesian coal prices, and continued replenishment by Chinese utilities.

In contrast, exports to India declined 5.9% m-o-m to 6.18 mnt in June and fell 11.52% y-o-y, with shipments also declining across both quarterly and half-year comparisons. The weakness reflected abundant domestic coal availability, subdued industrial consumption during the monsoon season, and cautious procurement by power producers amid comfortable inventories.

Southeast Asian markets continue to strengthen

Demand from Southeast Asia remained resilient during June. Exports to the Philippines rose 20.7% m-o-m and 22.91% y-o-y, supported by seasonal power demand and sustained coal-fired generation. Similarly, shipments to Malaysia increased 19.6% m-o-m and 41.96% y-o-y, reflecting higher import requirements from utilities and industrial consumers. Although cumulative H1 exports to both countries remained below last year’s levels, quarterly improvements indicate strengthening regional demand.

North Asian demand remains mixed

Exports to South Korea rose 30.5% m-o-m to 1.54 mnt and Japan increased 9.5% m-o-m to 1.38 mnt, driven by short-term restocking. However, weaker annual and quarterly shipments reflected cautious utility buying and comfortable inventories. Exports to other destinations declined 9.9% m-o-m to 6.81 mnt amid softer spot demand, despite stronger H1 and Q2 volumes.

East and South Kalimantan dominate supply

Among producing regions, East Kalimantan remained Indonesia’s largest coal-exporting region, with shipments increasing 1.9% m-o-m to 13.30 mnt in Jun’26 and 14.08% y-o-y, supported by stable mining operations, efficient logistics, and sustained export demand. Despite the monthly improvement, H1’26 exports declined 4.74% to 77.35 mnt, reflecting the impact of tighter production allocations earlier in the year, while Q2 shipments recovered 6.65% q-o-q to 39.92 mnt.

South Kalimantan maintained stable monthly exports at 10.35 mnt, while recording strong 30.90% y-o-y growth, supported by higher regional production and improved cargo movements. H1’26 shipments increased 6.08% to 60.26 mnt, and Q2 volumes rose 3.86% q-o-q to 30.70 mnt.

Sumatra posted the strongest monthly growth among all regions, with exports rising 12.6% m-o-m to 4.19 mnt, driven by improved vessel loadings and stronger regional demand. However, cumulative H1’26 exports fell 13.89% to 22.77 mnt, indicating weaker performance earlier in the year, while Q2 shipments increased 14.21% q-o-q to 12.14 mnt.

In contrast, North Kalimantan exports declined 25.8% m-o-m to 0.98 mnt and were 4.77% lower y-o-y, reflecting weaker mining activity and reduced loading operations. H1’26 shipments decreased 18.07% to 6.32 mnt, while Q2 volumes eased 1.88% q-o-q to 3.13 mnt.

Major loading ports reflect improved export activity

Taboneo remained the leading loading port with 5.17 mnt (+4.9% m-o-m), supported by steady export demand. Balikpapan recorded the strongest monthly growth to 2.63 mnt (+32.2% m-o-m) amid improved vessel loadings, while Bunati reached 3.48 mnt (+43.99% y-o-y) on higher regional production. In contrast, Samarinda (3.49 mnt, -1.4% m-o-m) and Muara Pantai (2.10 mnt, -7.9% m-o-m) witnessed lower shipments due to softer cargo movements and loading schedules.

HBA benchmarks rise on tight spot availability

Indonesia’s Harga Batubara Acuan (HBA) thermal coal benchmarks increased across all calorific value categories during the first half of July 2026. The price gains were supported by tighter spot availability resulting from domestic supply prioritisation, firm demand from Asian utilities, and continued uncertainty surrounding Indonesia’s evolving production and export policies. The strengthening benchmark also reflects increased buying interest from importers seeking to secure cargoes amid concerns over near-term supply availability.

Outlook

Indonesia’s non-coking coal market is expected to remain neutral to slightly bullish. Higher RKAB approvals should gradually improve supply, but continued DMO enforcement is likely to keep export availability tight. Firm demand from China and Southeast Asia should support exports and benchmark prices, while Indian imports may remain subdued during the monsoon, limiting upside in the near term.

Leave a Reply