- China remains largest import market despite slight Oct slowdown

- Flexible product mix, capacity expansions sustain export momentum

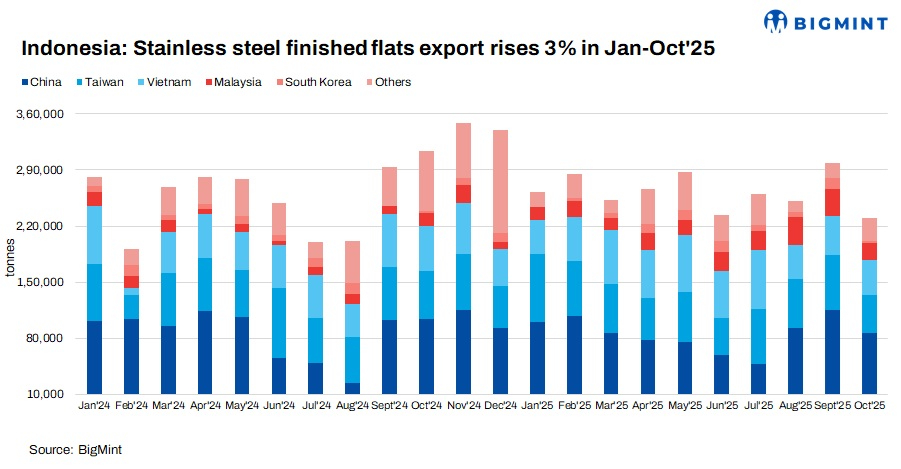

Indonesia’s stainless finished flat steel exports reached 2.63 million tonnes (mnt) during January-October 2025, up 3% from 2.56 mnt in the same period of 2024, according to BigMint data. The growth reflects steady demand from key Asian markets alongside continued downstream expansion within Indonesia’s stainless steel sector.

Indonesia further strengthened its position in Asia’s stainless steel trade, capturing a significant share of China’s import market during the first ten months of 2025, reaffirming its status as a leading regional exporter.

Country-wise performance

China remained the leading importer, accounting for 0.85 mnt of total exports in January-October 2025, down 1% y-o-y. Shipments to China also declined 25% m-o-m in October to 86,700 t, reflecting a short-term slowdown.

Taiwan was the second-largest market, importing 0.62 mnt, largely stable as 2024. Despite a 32% m-o-m dip in September, Taiwan continues to be a key growth market for Indonesia.

Vietnam imported 0.56 mnt, up 11% y-o-y, supported by rising downstream stainless steel production and robust infrastructure spending.

Malaysia recorded the sharpest growth, rising 92% y-o-y to 0.22 mnt, driven by increased consumption in construction and consumer goods sectors.

South Korea saw imports fall sharply, down 76% m-o-m to 3,300 t from 13,900 t in September, while other destinations collectively declined 24% y-o-y to 0.29 mnt, as trade volumes normalized following strong inflows in 2024.

Port-wise exports

Bahodupi Port remained the primary export hub, handling 2.59 mnt, up 3% y-o-y from 2.52 mnt, cementing its role as Indonesia’s key stainless steel shipping point.

Tanjung Perak Port contributed 34,576 t, slightly down 1% y-o-y from 35,017 t, while other minor ports managed 4,592 t, marking a 164% increase over the previous year.

Factors supporting rise in exports

Capacity expansion and production ramp-up: Indonesia’s stainless steel output continues to grow as major producers expand operations. PT Krakatau Posco maintains strong production at its 1.5 mnt/year hot-rolling mill in Cilegon, while Tsingshan Group has further boosted output at the Morowali Industrial Park, reinforcing its role as the country’s largest stainless producer.

The Tsingshan-Jindal Stainless joint venture, PT Glory Metal Indonesia, is set to add 1.2 mnt/year of stainless capacity by 2026, while PT Jindal Stainless Indonesia is upgrading its 150,000 t/year cold-rolling facility. New entrants, including New Asia International, have commissioned additional rolling mills, collectively lifting Indonesia’s stainless steel production potential.

Raw material cost advantage: Indonesia’s abundant nickel ore reserves continue to provide a competitive edge. Local nickel availability at lower costs allows mills to produce stainless steel more efficiently, supporting higher output and exports compared to countries dependent on imported raw materials.

Strategic product mix and trade adaptability: Unlike previous months, October saw a surge in hot-rolled stainless steel slab shipments to the EU, which offset a decline in cold-rolled finished product exports. This demonstrates Indonesia’s ability to adapt its export mix in response to global trade challenges, including EU anti-dumping and countervailing duties on finished products. At the same time, Asian markets, particularly China, Vietnam, and Malaysia, continued to absorb high volumes of finished flats, supporting overall growth.

Outlook

Indonesia’s stainless steel exports are expected to remain resilient, supported by ongoing capacity expansions, competitive nickel-based production costs, and a flexible product mix. Asian markets, particularly Vietnam and Malaysia, will continue to absorb finished flats, while EU-bound slab shipments may help navigate trade barriers ensuring overall export growth and reinforcing Indonesia’s position as a leading regional stainless steel exporter.

Leave a Reply