- BigMint’s benchmark 304-series HRC stays unchanged w-o-w

- Export demand steady while domestic sentiment weakens

India’s stainless steel market remained largely muted this week, with soft demand and slow offtake keeping activity subdued across both flats and longs. Prices remained largely range-bound as mills continued limited raw material procurement, while active import inflows from Southeast Asia added pressure on domestic offers. Despite announcements of new capacities and firmer sales at select producers, overall market sentiment remained weak.

Demand in the 300-series stayed subdued, though minor shortages were reported in select sizes. The 400-series showed gradual improvement, supported by firmer inquiries. 200-series continued to witness healthy demand amid tight availability of imported material.

Despite ongoing capacity announcements and improved sales across mills, overall sentiment in the domestic stainless steel market remained subdued.

Finished flats market remain soft

India’s stainless steel flat market remained soft, with mills operating cautiously and buyers limiting purchases due to weak end-use demand.

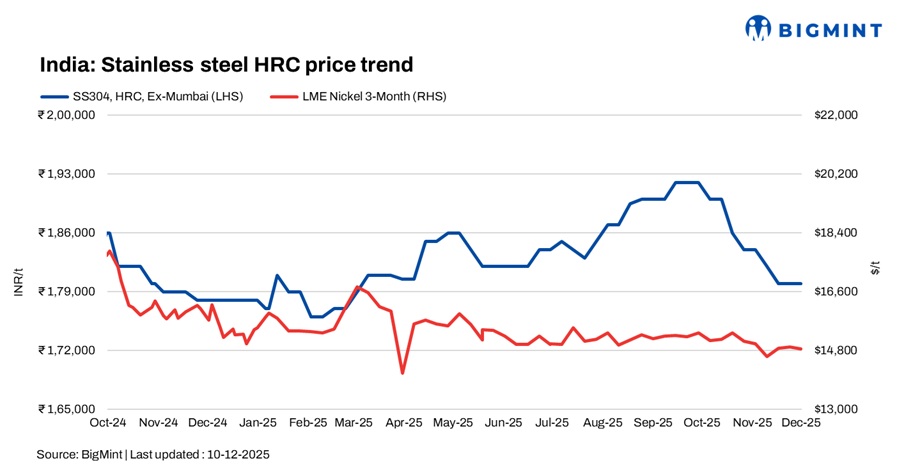

BigMint’s benchmark assessment for 304 HRC stood at INR 180,000/t ex-Mumbai, unchanged w-o-w.

Market activity at major mills stayed muted due to weak finished steel demand. 316-grade material witnessed deeper softness, whereas 304-grade consumption showed relatively stable buying interest.

One participant noted, “Prices in the market are down by INR 2,000-3,000/t. Unwanted, non-licensed imports from China were heard. Chinese materials are nearly 15% cheaper than Vietnam and Thailand.”

Similarly, BigMint’s SS 316 HRC was assessed at INR 333,000/t ex-Mumbai, down INR 4,000/t w-o-w.

Additionally, market sources reported that a leading stainless steel coil producer reduced prices across key grades-cutting 304 coils by INR 3,000/t, 316 coils by INR 6,000/t, JT hot-rolled by INR 6,000/t, and JT cold-rolled coils by INR 3,000/t.

Finished longs see mixed trends

Stainless steel longs remained under pressure, with sentiment weighed down by sluggish downstream movement and muted demand, resulting in mixed price trends across key grades.

BigMint’s benchmark assessments for stainless steel 304L (25 to 100 mm) black round bars was INR 155,000/t ex-Mumbai, stable w-o-w. Meanwhile, SS 316L black round bars were at INR 270,000/t ex-Mumbai, down INR 4,000/t w-o-w.

Exports continued to move steadily, according to mill sources. However, domestic sentiment weakened further due to panic selling. A trader added, “304 billets were recently sold around INR 135,000–137,000/t. With the dollar moving up, importers may now be facing losses.”

LME nickel range-bound w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $14,855/t, largely range-bound compared to last week’s $14,920/t. Nickel stocks at LME-registered warehouses stood at 252,528 t, down slightly compared to 253,074 t t in the previous week.

Chinese stainless steel & NPI prices

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,300/t ($1,883/t) exw, while FOB tags of 304-grade CRCs were firm at $1,860/t.

Indonesian FOB prices of nickel pig iron (NPI) (8-12%) were at $111/t and NPI (10-14%) stood at $112/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices remained largely stable, edging down by INR 7,000/t ($78/t) w-o-w to INR 2,607,000/t ($29,011/t) exw on 10 December, according to BigMint’s assessment. Despite stable prices, market activity remained quiet due to sluggish end-user demand and a drop in LME prices.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices dropped by INR 1,200/t w-o-w to INR 109,500/t ($1,217/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices remained largely stable, edging up by INR 300/t ($3/t) on 8 December compared with the 1 December assessment. According to BigMint, prices in India stood at INR 98,300/t ($1,093/t) exw-Guwahati on 8 December. In Bhutan, prices also edged up by INR 500/t ($6/t) w-o-w to INR 99,000/t ($1,101/t) exw.

Ferrous scrap: Imported scrap demand in India stayed muted, with buyers resisting current HMS, busheling, and shredded prices amid inventory pressures, resulting in selective bookings. Australian-origin offers were heard at $320-322/t for HMS 80:20, $325-326/t for HMS 1, $338-340/t for shredded, and $342-345/t for PNS, while Israeli tin-can bundles were at $250-255/t CFR Chennai. A mild pickup in inquiries was noted as some buyers moved to complete winter restocking ahead of Western holiday shutdowns.

Outlook

India’s stainless steel finished market is expected to remain subdued in the near term, with weak end-use demand and year-end caution limiting trading activity. Price pressure is likely to persist amid adequate inventories, ongoing import competition, and slow downstream offtake.

Leave a Reply