- Stronger demand for lower-CV coal driven by cost-conscious Asian utilities

- Higher-CV coal under pressure amid cautious buying and ample supply

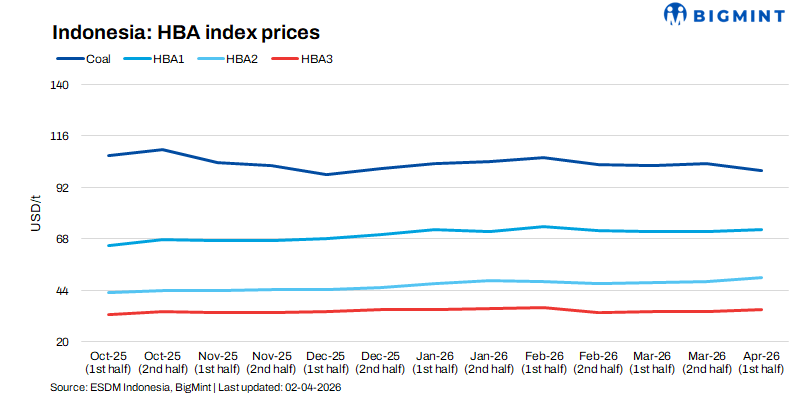

The thermal coal benchmark prices released by Indonesia’s Ministry of Energy and Mineral Resources (Ministry of Energy and Mineral Resources (ESDM)) for the first half of April 2026 indicate mixed price movements across calorific value (CV) segments, mirroring evolving demand patterns within the broader Indonesian coal market.

While higher-calorific coal experienced a mild correction, lower-CV grades continued to strengthen, reflecting changing procurement preferences among key Asian importers and the competitive positioning of Indonesian coal in the seaborne market.

Mild pressure on higher-calorific Indonesian coal

The benchmark price for 6,322 kcal/kg GAR coal declined by around 3% from the second half of March to $99.87/t. The moderation largely reflects subdued demand for higher-CV Indonesian coal as buyers remain cautious amid comfortable inventory levels and increased availability of alternative supplies in the seaborne market. In addition, utilities in several importing countries have been increasingly focused on cost optimisation, reducing their reliance on higher-priced, high-energy coal and placing downward pressure on premium-grade Indonesian cargoes.

Stable demand supports mid-CV coal

The HBA-I benchmark for 5,300 kcal/kg GAR coal increased marginally by 1% to $72.28/t, suggesting stable demand for Indonesia’s mid-calorific coal segment. This grade continues to serve as a key blending component for many power producers across Asia, supporting steady procurement interest. However, buying activity has remained measured as utilities balance fuel procurement with inventory management and evolving electricity demand.

Stronger gains for lower-CV Indonesian coal

Lower-calorific Indonesian coal segments recorded comparatively stronger gains during the assessment period. The HBA-II benchmark for 4,100 kcal/kg GAR rose by 3.5% to $49.99/t, while the HBA-III benchmark for 3,400 kcal/kg GAR increased by 2.9% to $35.23/t compared to the second half of March.

The upward movement reflects sustained demand from price-sensitive markets in South and Southeast Asia, where utilities are increasingly opting for lower-cost coal to manage generation expenses. Indonesia remains the dominant supplier of such lower-CV coal in the seaborne market, enabling its producers to maintain strong export competitiveness despite broader market uncertainties.

Outlook

Indonesia’s coal market is likely to see stronger demand for lower-CV coal due to its cost advantage among Asian utilities. Higher-CV grades may remain under pressure amid cautious buying and ample supply, keeping benchmark prices largely range-bound.

Leave a Reply