- Imports drop 7% m-o-m and 17% y-o-y in Aug

- South African exports drop to a 2-year low on weak DRI market

- Coal-fired generation declines 2.6% y-o-y in Jan-Aug’25

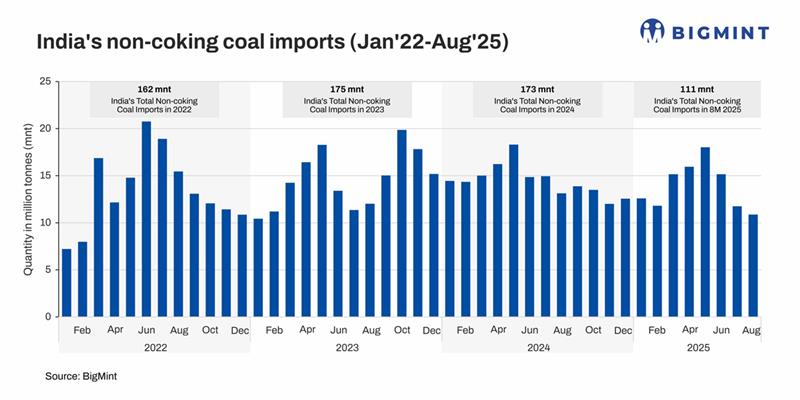

Morning Brief: India’s imports of non-coking coal dropped to 10.87 million tonnes (mnt) in August 2025, down from 11.61 mnt in July, a decrease of around 7% m-o-m. As per BigMint data, non-coking coal imports have dropped to the lowest level since December 2022. Notably, imports fell by over 17% y-o-y from 13.13 mnt in August 2024.

Coal imports fell to two-and-a-half-year lows despite domestic production remaining under pressure due to heavy monsoon rains throughout the country. This shows significant improvement in terms of lessening coal import dependency which happens to be a key plank of government policy in the sector.

The leading shippers in August were Indonesia, which raised exports to India by over 13% m-o-m to 7.7 mnt, and South Africa with just 1.2 mnt, a sharp drop of 37% m-o-m. While US imports were recorded at nil in August, shipments from Mozambique and Australia edged down m-o-m. Imports from Russia increased marginally.

Why did imports drop in Aug’25?

Coal-fired generation falls in Aug & 8MCY’25: India’s coal-fired power generation dropped 1.3% m-o-m in August and, strikingly, by 2.6% y-o-y in January-August of the current year. Lower peak demand due to early onset and above-average monsoon led to only a slight 1.5% y-o-y increase in power demand in 8MCY’25. Power consumption in August dropped lower than July.

Domestic production rises, enough stocks at power plants: India’s coal production surged 8.5% m-o-m to 50.4 mnt, with dispatches up 6% m-o-m. However, production and dispatches are still marginally lower y-o-y.

Sufficient stocks of over 20 days at power plants despite monsoon disruption to coal mining and transportation kept demand for imported coal on a tight leash. The coal stock at domestic coal-based thermal power plants as on 31 August was 47.45 mnt as compared to 37.19 mnt in the same period last year with a growth of 27.59%. At the level of actual consumption, this stock is sufficient for 22 days.

Imports from South Africa drop to 2-year low: Coal imports from South Africa stood at 1.24 mnt in August, a 2-year low. Increased blending of domestic coal has been reported, especially after sponge iron prices fell to multi-year lows. Some players were heard blending domestic to imported coal in a ratio of 90:10.

Domestic sponge prices remained largely rangebound m-o-m. In August the average price was assessed at INR 24,100/t exw Raipur versus INR 23,750/t in July. Domestic coal remained the preference amid fluctuating global prices and hike in vessel freight rates. Freights for Panamax carriers from RBCT to Paradip rose from $13.6/dry metric tonne (DMT) in early July to $15 in end August.

Nil imports from US: Imports from the US came to a halt in August as against 1.09 mnt in July, reflecting weaker demand for cargoes due to costlier ocean freights which were recorded at $43/t on 8 September, $3/t higher than the beginning of last month. Drying up of imports from the US weighed on total volumes.

Outlook

India’s non-coking coal imports reached 89 mnt in H1CY’25 compared with 93 mnt in the corresponding period of last year, a decrease of over 4% y-o-y. July and August have seen imports declining further. With sufficient stocks at plants and CIL increasing allocation for the non-regulated sector, this trend is likely to continue. A festive spurt in electricity consumption and coal requirement during the Navratri-Diwali period may be expected, but imports are unlikely to increase much.

The replacement of the erstwhile cess of INR 400 on coal by an overall 18% GST slab is expected to slash coal prices in both the domestic and import markets. Traders are clearing stocks before the new regulations kick in on 22 September. Electricity prices, too, are expected to get marginally cheaper. This may provide support to the domestic and import coal market.

Leave a Reply