- Indian mills delay purchases amid price drop expectations

- Indian met coke prices stay supported, BF rebar tags drop

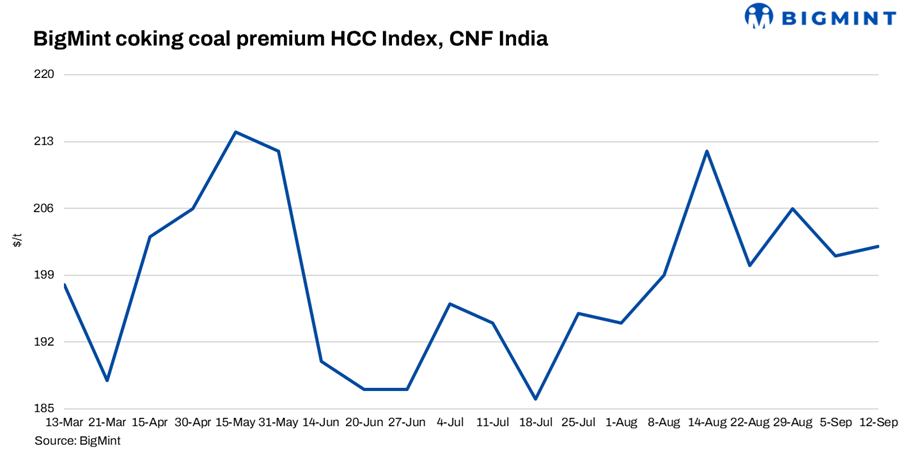

BigMint’s premium hard coking coal (PHCC) index was assessed at $202/tonne (t) CNF Paradip, India, on 12 September 2025, up by $1/t against the previous assessment on 5 September 2025. Limited market activity kept prices stagnant.

Two deals were concluded by Indian mill this week at $201-203/t CFR India, stated some market players. Most mills were understood to have bid at $200-203/t CFR India.

“The market has been range-bound in the past couple of weeks, with Australian PHCC offers hovering at around $186-188/t FOB, which would translate to $201-203/t CFR India. Indian mills are expecting price softness in the near term. Hence, they are slightly delaying their purchases,” stated a mill source.

India’s coking coal imports fell 10% m-o-m to 5.5 million tonnes (mnt) in August 2025 from 6.1 mnt in July. Notably, July’s imports, at 6.1 mnt, were higher than the usual monthly average, owing to restocking needs and the arrival of vessels booked earlier, when prices had witnessed a drop.

Rationale

BigMint’s coking coal index is derived using data points, i.e., trades, offers, bids, and indicative prices.

A deal was heard concluded but confirmation was not received. Hence, it was considered for index computation and given a weightage of 0%.

Nine (09) firm offers, bids, and indicative prices were heard. Out of these, eight (8) were considered for price calculation and given 100% weightage.

BigMint has consolidated its Prime Hard Coking Coal (PHCC) CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia – normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors impacting imported coking coal prices

1. Indian met coke prices remain supported w-o-w: The Indian met coke market remained largely stable during the week ending 11 September 2025. BF-grade (25-90 mm) met coke was assessed at INR 29,500/t ex-Jajpur, reflecting a slight increase of INR 500/t w-o-w. Prices in western India held firm, with ex-works Gandhidham offers assessed at INR 30,000/t.

2. China’s coke market turns sharply bearish: Meanwhile, China’s coke market entered a bearish phase after 8 September. Steelmakers in Shandong reduced purchase prices of Quasi Grade I coke to RMB 1,445/t for wet-quenching and RMB 1,695/t for dry-quenching, delivered with VAT. This sharp roll-back marked the failure of producers’ eighth consecutive attempt to raise prices, highlighting mounting bearish sentiment. A combination of weak steel demand, limited procurement from mills, and rising cost pressures collectively fuelled the decline, leaving China’s coke producers under significant stress.

3. BF-rebar trade prices drop w-o-w amid weak buying activity: India’s trade-level blast furnace (BF) rebar prices dropped w-o-w across major markets. Major mills either increased their discounts or reduced list prices due to subdued market sentiments. Trade-level BF rebar prices edged down by INR 100/t ($1/t) w-o-w to INR 47,200/t ($534/t) exy-Mumbai, as per BigMint’s assessment on 12 September 2025. Prices are exclusive of GST at 18%. Inventories at mills rose slightly by around 8% in mid-September, compared with levels seen at the beginning of the month.

Leave a Reply