- Indonesia top exporter in Apr-Sep’25 at 0.82 mnt

- Imports drop sharply in Aug, Sep after QR extension

- Import curbs likely to spur merchant coke production

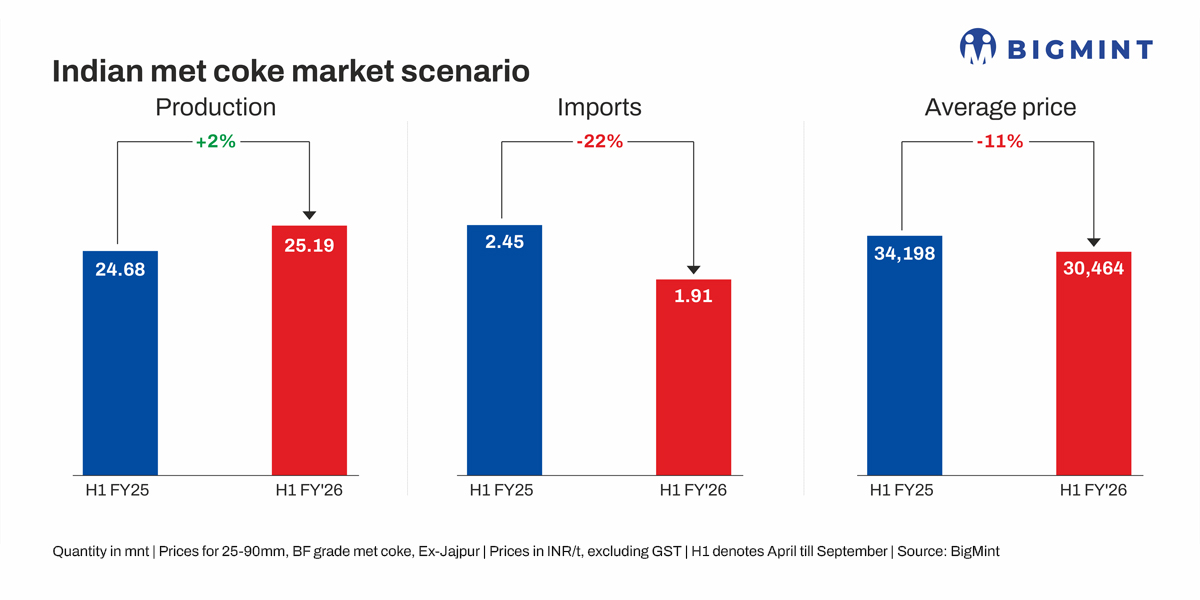

Morning Brief: India’s imports of metallurgical coke were recorded at 1.91 million tonnes (mnt) in April-September 2025 (H1FY’26) in comparison with 2.45 mnt in H1FY’25, as per provisional data maintained with BigMint. Coke imports decreased by nearly 22% y-o-y despite the 10-11% growth in domestic crude steel production during the period. This was due to regulatory interventions aimed at controlling the quantity of coke imported per country.

India’s coke imports in CY’24 were over 4.8 mnt, an increase of 24% y-o-y. Met coke production stood at 49.28 mnt in FY’25, and imports were recorded at 4.8 mnt. However, after the government put restrictions, imports started edging down sharply. In September, coke imports dropped over 43% y-o-y to just 0.18 mnt – the lowest monthly imports in over two years barring the record low volumes recorded in February this year.

Key import sources

India’s imports of coke were mainly from Indonesia, which supplied 0.82 mnt in H1FY’26 compared to 0.86 in H1 last fiscal. Among the other top exporters were Poland with 0.26 mnt compared to 0.36 mnt in H1FY’25 and Colombia at 0.25 mnt.

The top importers of coke in H1 were AM/NS India (0.44 mnt), JSW Steel (0.2 mnt) and Tata Steel (0.13 mnt).

Why did coke imports fall in H1FY’26?

Govt imposes QR restrictions for entire CY’25: In end-December 2024, the Director General of Foreign Trade (DGFT), Government of India, sanctioned the imposition of “quantitative restrictions” on imports of low-ash metallurgical coke (LAM coke) into India. The country-wise quantitative restrictions on coke were announced for two quarters of 2025, i.e. January-March and April-June with the total volume pegged at 713,583 t in each quarter.

Later in July the QR was extended till December of this year. The restrictions apply to specific HS codes and include country-wise quotas for imports. For the period of July-September, a total of 713,583 t was permitted, with an equal amount for October-December, resulting in a total import quota of roughly 1.427 mnt, with allocations for all the key exporters.

Domestic met coke production rises: India’s met coke production, as per provisional data, reached 25.2 mnt in H1 from 24.7 mnt in the same period last fiscal. Both captive and merchant production witnessed an increase. This may not directly have contributed to lessening coke imports but may work toward lowering dependence on imports in the long term. All the leading steel producers (captive coke producers) are expanding crude steel and coke-making capacity.

On the other hand, growth in domestic crude steel capacity and curbs on import volumes boosted domestic merchant coke production. Cost-competitive imports, especially from Indonesia, were found to be hurting the domestic industry. Now, with quantitative curbs in place, the merchant producers are likely to increase domestic production and coking coal purchases.

Increase in coking coal imports: India’s coking coal imports in H1 increased to 33 mnt from 30 mnt in H1FY’25 due to the surge in hot metal production. Moreover, BigMint’s coking coal index, CNF India, started the fiscal year at around $204/t in April and has remained flat at around $206/t CNF Paradip in October. The absence of volatility and sharp price spikes in the coking coal market this year has paved the way for increased coking coal imports and, by extension, lower imports of met coke.

Notably, apart from rapid growth in surplus coke production capacity in some Asian countries, volatility in coking coal prices in the past has been the key reason for higher imports of more competitively-priced coke from certain countries which offered lower prices due to their relative isolation from global trends on account of state support.

Outlook

The Tier-1 mills are investing in coke-making capacity and merchant coke output is expected to rise. A notable recent example was the takeover of Saurashtra Fuels and its 800,000 t plant in Gujarat by Dubai-based investment firm Synergy Capital. Such initiatives will boost domestic production and minimise reliance on imports. That apart, the quantitative curbs till 31 December will also keep imports in check.

Leave a Reply