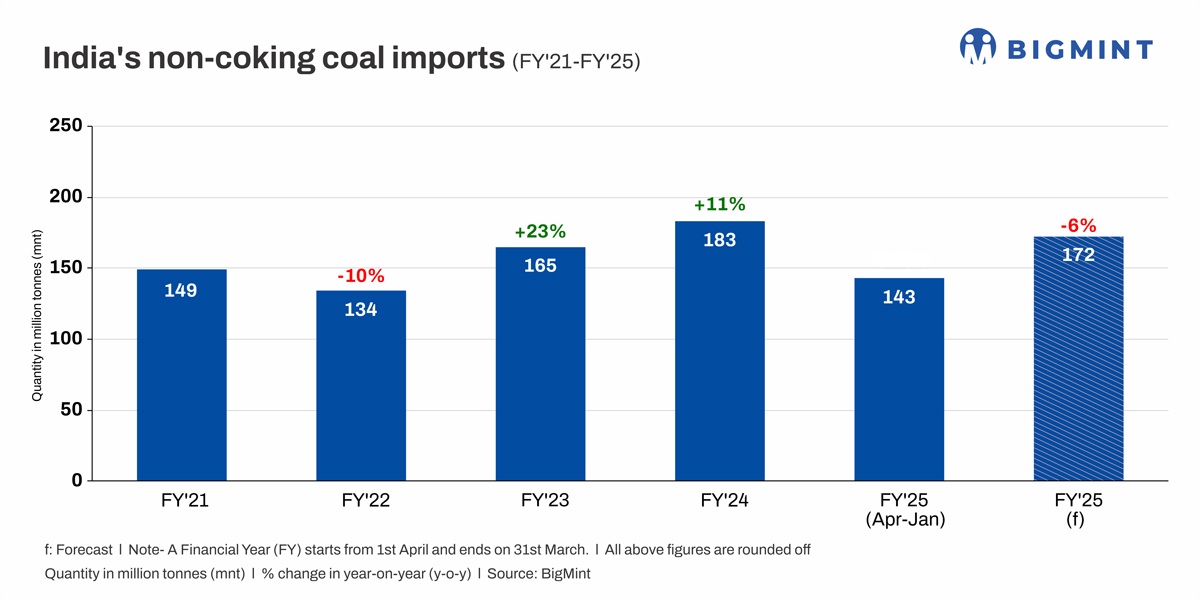

- Imports projected to fall to 172 mnt vs. 183 mnt in FY’24

- Domestic production to grow over 6% y-o-y to nearly 1 billion tonnes

- Indonesia to see slight decline in shipments in contrast to South Africa

Morning Brief: India’s imports of non-coking coal, including coal used in the power sector as well as for industrial purposes, are projected to drop around 6% y-o-y in financial year 2024-2025 (FY’25), as per provisional data with BigMint. Non-coking coal imports, mainly low-ash and high-CV coal, are expected to fall to 172 million tonnes (mnt) in the current fiscal from 183 mnt recorded in FY’24.

Total imports declined by around 1.3% y-o-y to around 173 mnt in 2024, as BigMint reported earlier.

India: country-wise imports

India: country-wise imports

Indonesia will emerge as the top non-coking coal exporter to India in FY’25, although total shipments are estimated to shrink by over 4% y-o-y to around 107 mnt from 112 mnt in FY’24. Indonesia’s share in total imports is expected to be around 62%.

Among the other major importers, shipments from South Africa are projected to rise by roughly 3 mnt y-o-y to reach 33 mnt in FY’25 from 30 mnt in the previous fiscal.

While non-coking coal imports from Australia and Russia are projected to edge down y-o-y, US exports to India are expected to remain largely flat.

Factors shaping coal import trends

*Growth in domestic coal production: Non-coking coal production in India is set to increase by 6.5% y-o-y, as per provisional data, to reach around 992 mnt in FY’25 from 931 mnt in FY’24. State-run CIL may have revised its production guidance to 806-810 mnt from 838 mnt earlier due to lower volumes from SECL and BCCL, but the guidance is still higher by around 4% y-o-y from production of roughly 774 mnt in FY’24.

On the other hand, production from captive, commercial mines in April-November 2024 rose 33% to 100.08 mnt from 75.05 mnt in the year-ago period, according to Coal Ministry data. Likewise, total dispatches from captive and commercial coal mines during the period rose to 107.81 mnt from 80.23 mnt.

*Drop in share of imported coal for blending: Notably, the government’s mandate on imported coal blending for power plants ends in February. Notably, the mandate has been revised several times since 2020. Also, Coal Ministry data reveal that, as of January, the share of imported coal for blending in power plants has fallen by 23.56% y-o-y.

Higher domestic production apart, increasing efficiency of domestic thermal power plants, efficient blending strategies of power producers and government mandate on 5% biomass co-firing in thermal plants are also some of the key reasons why coal imports are projected to edge lower.

*Higher domestic availability: In a major boost to domestic coal availability, CIL has reduced the Earnest Money Deposit (EMD) for its e-auctions from INR 500/t to INR 150/t. This decision aims to boost participation and competitiveness, as e-auction premiums have dropped significantly from 252% in FY’23 to 29% in FY’25. By lowering entry barriers, CIL seeks to stimulate bidding activity and cater to a larger segment of buyers.

Therefore, the government’s push to make domestic coal available and efforts at closing the gap between peak coal demand and actual supply have led to reduced dependence on imports.

*Increased generation from renewables: The country’s cumulative generation of power has increased at a faster pace than thermal generation during the current fiscal. Government data show that total generation from renewable energy sources (excluding large hydro) climbed by over 12% y-o-y to 192 billion units (BU) in April-January 2024 compared with 171 BU in the corresponding period of last fiscal. Solar generation increased by over 21% in 3QFY’25 (April-December) to 102.139 BU, as per Central Electricity Authority (CEA) data, while thermal generation rose by just 3% during the period.

*Increased generation from renewables: The country’s cumulative generation of power has increased at a faster pace than thermal generation during the current fiscal. Government data show that total generation from renewable energy sources (excluding large hydro) climbed by over 12% y-o-y to 192 billion units (BU) in April-January 2024 compared with 171 BU in the corresponding period of last fiscal. Solar generation increased by over 21% in 3QFY’25 (April-December) to 102.139 BU, as per Central Electricity Authority (CEA) data, while thermal generation rose by just 3% during the period.

So, although coal remains the mainstay in terms of baseload and flexibility, higher share of renewables is definitely a long-term trend gradually leading to reduced dependency on thermal power.

Leave a Reply