- South African offers firm sharply; domestic sentiment weakens as buyers stay cautious

- Industrial slowdown limits imports despite tighter global supply conditions

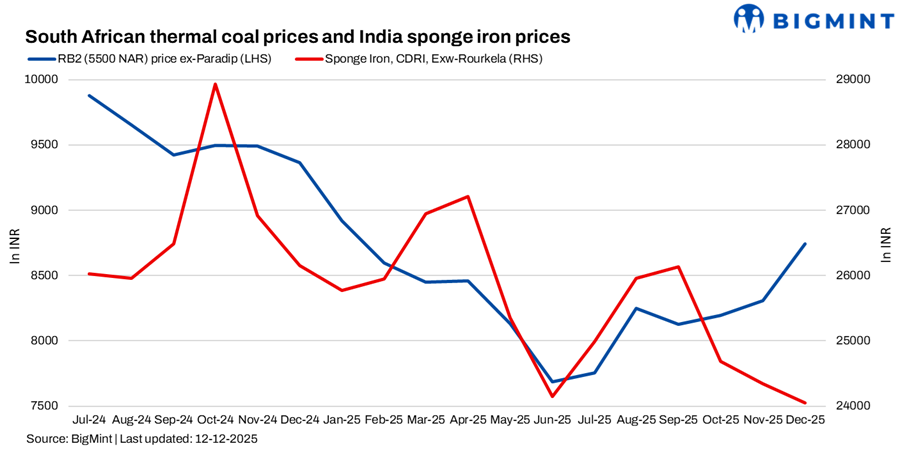

India’s coal market saw further divergence in the week ended 12 December, with South African thermal coal offers rising again even as domestic demand weakened across sponge iron and industrial sectors. Higher forex, tight supply from South Africa, and the operational disruption at RBCT continued to elevate offer levels, but Indian buyers showed limited acceptance amid subdued downstream markets and weak appetite for imports.

South African offers rise on tightened supply and RBCT disruption

South African RB2 (5,500 NAR) firmed w-o-w, with ex-Paradip and ex-Gangavaram rising to INR 8,900/t, while ex-Vizag increased to INR 8,850/t, up INR 100-200. RB3 (4,800 NAR) also strengthened, with ex-Paradip and ex-Gangavaram touching INR 7,500/t, and ex-Vizag at INR 7,400/t, also up INR 100-200.

Despite higher offers, Indian acceptance remained negligible as sponge iron and rebar demand softened.

Tightness deepened after crane damage halted operations at RBCT, delaying cargo availability owing to increased in demand from different destination until mid-February. As a result, RB2 CNF India offers climbed to $93-94/t and RB3 to $77/t, rising around $1 w-o-w. Traders reported higher offers due to limited cargo availability and further currency depreciation. However, India mills demand for South African coal yet to pick up on slow domestic market.

Portside inventories also drifted higher by 0.8% w-o-w to 13.05 mnt, adding to the oversupplied domestic landscape.

Domestic market weakens as SECL auction clears at lower bids

Domestic coal prices extended their decline, falling INR 150-250/t w-o-w, with 5,000 GCV at INR 5,800/t and 4,500 GCV at INR 4,900/t.

SECL’s 12 December auction (3.2 mnt) sold out fully, but final bids were INR 200-300/t lower than the last auction, confirming expectations of further price softening.

Sponge iron demand remains weak, curbing coal procurement

Sponge iron prices continued to fall, with CDRI ex-Rourkela down INR 650 w-o-w to INR 23,600/t, reflecting low finished steel demand. Buyers stayed cautious, expecting further reductions, and restricted purchases to immediate needs. No major bookings were reported, reinforcing a bearish near-term outlook for coal consumption.

Leave a Reply