- South African offers firm amid cargo tightness, but Indian buying stayed muted

- Sponge iron weakness continued to cap near-term coal demand

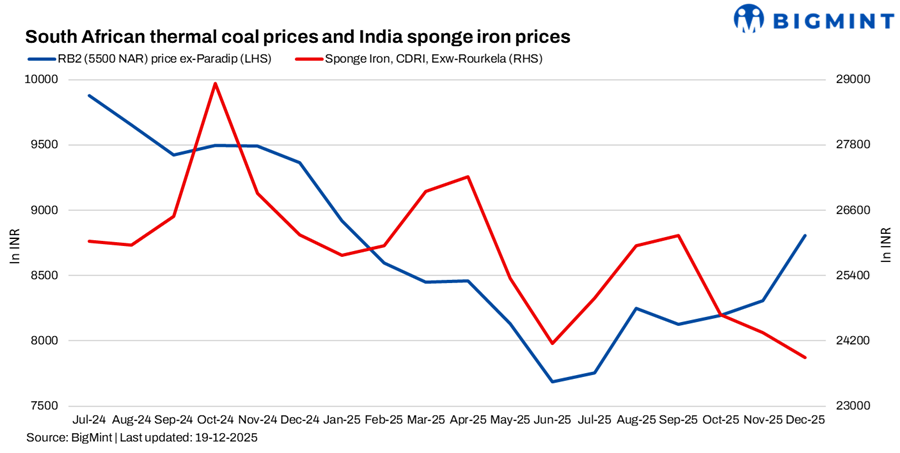

South African thermal coal offers strengthened furtherin the week ended 19 December despite limited buying interest. Offers for RB2 (5,500 NAR) ex-Paradip, Vizag and Gangavaram rose to INR 9,200-9,250/t exw levels this week, however, active trades at these levels are yet to be concluded.

RB2 (5,500 NAR) price assessment of BigMint ex-Paradip, Vizag and Gangavaram rose to INR 8,900-8,950/t w-o-w, while RB3 (4,800 NAR) increased to around INR 7,550/t, up INR 50-150/t. Portside offers firmed due to low inventories at select ports, including Kandla and Mangalore, and persistent cargo tightness following extended maintenance and loading constraints at Richards Bay Coal Terminal. CNF India offers remained high amid elevated seaborne prices, firm freight and forex pressure. Despite this, portside inquiries were largely absent, as buyers resisted higher replacement costs.

Demand remains fragile

Indian buyer appetite stayed weak as downstream sponge iron and steel markets remained under pressure. Although select trades were reported, including RB3 ex-Vizag at INR 7,600/t for 20,000 t and limited volumes ex-Mangalore, overall acceptance of South African material was minimal. High raw material costs, weak finished steel demand and thin margins continued to restrict procurement. Market participants indicated that several sponge iron producers were evaluating temporary shutdowns if margins failed to improve, further clouding near-term coal demand.

Domestic coal stays comfortable

Domestic coal prices softened marginally w-o-w, with 5,000 GCV assessed at INR 5,750/t and 4,500 GCV at INR 4,800/t, down INR 50-100/t. Coal availability remained comfortable across key consuming regions, keeping buying largely need-based. SECL’s 12 December 2025 auction reinforced supply comfort, with around 2.80 mnt allocated out of 3.22 mnt offered, reflecting strong participation but measured bidding behaviour.

Sponge iron gives mixed signals

India’s sponge iron market showed divergent regional trends. CDRI ex-Rourkela edged up INR 200/t w-o-w to INR 23,800/t, supported by selective restocking in parts of southern India. However, eastern and central regions continued to face subdued demand, with prices easing INR 50-200/t amid slow steel offtake. The uneven sponge iron outlook kept coal procurement cautious, as buyers prioritised inventory control over fresh commitments.

Portside stocks stable w-o-w

India’s portside thermal coal inventories remained broadly stable at around 13.07 mnton 15 December, compared with 13.05 mnt in the previous week. While stocks stayed balanced overall, uneven distribution and low availability at select ports added to localised price firmness.

Market outlook

The coal market remained uncertain, caught between firm imported offers and weak domestic consumption. With Christmas holidays approaching, trading activity was expected to thin further. Any meaningful pickup in demand is likely to hinge on stabilisation in sponge iron and steel prices, while sustained cargo tightness from South Africa may continue to support offer levels in the near term.

Leave a Reply