- Australia-India rates at 6-month low on ample vessel availability

- Baltic index declines to 1-month low on falling Panamax rates

Global dry bulk coal freight markets witnessed a notable softening this week, with key routes to India under pressure amid falling cargo volumes, abundant vessel availability, and cautious buying sentiment. Rates across the Australia-India, South Africa-India, and Indonesia-India routes declined, dragging Panamax and Supramax indices to multi-week lows.

“The coal freight market has turned slightly bearish, as reduced cargo volumes across both the Pacific and Atlantic basins have weakened demand for tonnage. Slower fixing activity, cautious buying behaviour, and growing vessel availability have prompted owners to soften rate expectations, keeping freight sentiment under pressure despite stable port operations in some regions,” stated a major shipping giant to BigMint.

Another ship-broker said, “The Baltic Dry Index fell to a one-month low as freights weakened across all vessel sizes. Panamax losses dragged down the index, despite firmer iron ore prices. In agri-markets, wheat prices hovered near eight-week lows after China cancelled several US cargo purchases, reinforcing concerns over weak global demand and intense export competition. Ample supply with major exporters, coupled with aggressive pricing from Black Sea origins, continued to pressure the market, limiting any recovery attempts.”

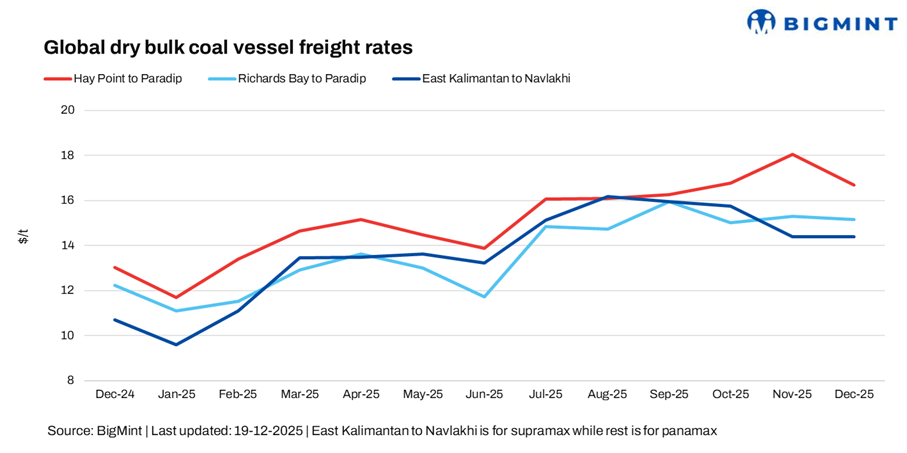

Coal freights on the Australia-India route fell sharply this week to around a six-month low, as already thin activity weakened further and spot enquiries dried up. The limited momentum seen last week failed to carry through, with fixtures reported at much lower levels, reflecting ample vessel availability. Softer sentiment in India’s domestic steel market continued to weigh on cargo demand, as prices remained under pressure and high inventories discouraged near-term buying. Overall, weak downstream fundamentals and poor cargo visibility reinforced the bearish tone on the route, with little immediate catalyst for a near-term recovery.

Freights on the South Africa-India route slid to around a four-month low this week. The pullback was driven by subdued cargo demand and a growing list of open vessels, which eroded the earlier tonnage tightness that had supported rates. With limited fresh enquiries and charterers adopting a more cautious stance, owners were compelled to trim rate ideas to secure vessels. Weaker downstream fundamentals in India and muted fixing activity further reinforced the softer tone, leaving the route under pressure with little near-term support.

Similarly, Supramax freights on the Indonesia-India route fell to over a one-month low this week, as the brief firmness seen earlier gave way to weaker sentiment. Activity remained muted, with no major fixtures reported and limited fresh enquiries from Indian charterers, while a growing list of open tonnage added pressure on owners.

Another source told BigMint, “Asia-Pacific Supramax freights weakened across both the Pacific and Indian Ocean basins, although market visibility remained limited due to a lack of reported fixtures during the day.”

Softer crude, weak demand pull bunker prices lower

Bunker prices declined this week across major global bunkering hubs, reflecting softer crude oil prices, ample fuel availability, and muted demand from the shipping sector. However, the benefit of cheaper bunkers was largely offset by weak freight fundamentals, as sluggish cargo volumes and abundant vessel supply continued to pressure earnings, limiting any meaningful improvement in market sentiment.

Rising tonnage availability shifts market back in favour of charterers

Demand-supply dynamics in the vessel freight market loosened this week, with rising tonnage availability and weaker cargo volumes tipping the balance back in favour of charterers. In the Pacific, the earlier tightness for prompt vessels eased as fewer Australian and Indonesian cargoes entered the market, leading to longer open lists and renewed pressure on rates. The Atlantic basin also saw softer fundamentals, with export activity slowing and vessel supply remaining ample, limiting owners’ ability to defend levels.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India fell by around 2.7/dry metric tonne (dmt) w-o-w to $14.4/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route edged lower by $0.7/dmt w-o-w to $14.3/dmt. “Fixing activity out of South Africa remained limited during Asian trading hours, with only scant market information reported,” said a Mumbai-based ship-broker.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $13.76/dmt, a decrease of $0.24/dmt w-o-w.

Meanwhile, the Baltic Exchange’s dry bulk index for Panamax and Supramax vessels witnessed a significant fall this week, with the Panamax index falling sharply by around 335 points w-o-w to 1,389 and the Supramax index decreasing by 129 points to 1,258. The indices fell this week due to weaker cargo volumes and soft demand across key routes. Rising vessel availability and longer open tonnage lists gave charterers leverage, forcing owners to reduce rates. Seasonal slowdowns and cautious buying from Indian and Northeast Asian importers further pressured the market, with Panamax earnings dropping more sharply than Supramax.

Outlook

In the next week, dry bulk coal freights to India are likely to remain under pressure, particularly across the Pacific and South Africa-India routes. Seasonal slowdowns in Indian steel and power demand, alongside cautious buying ahead of price announcements, may further restrain fixing activity, preventing any meaningful upside in rates.

However, occasional short-term support could emerge from temporary disruptions — such as port congestion, weather-related delays, or sudden demand spikes from Indian mills. Overall, the market is expected to stay stable to soft, with freight levels sensitive to shifts in cargo flows, tonnage availability, and regional buying sentiment over the coming weeks.

Leave a Reply