The tier-I steel mills announced an increase in their list prices of hot-rolled coil (HRC), HR-Plates and, cold-rolled coils (CRC) by INR 1,500/tonne (t) for May 2024 sales. The rise in raw material prices and easing of supplies in the market due to maintenance undertaken by mills seem to be the direct reasons.

The effective list price levels for May 2024 sales are as below for public and private mills:

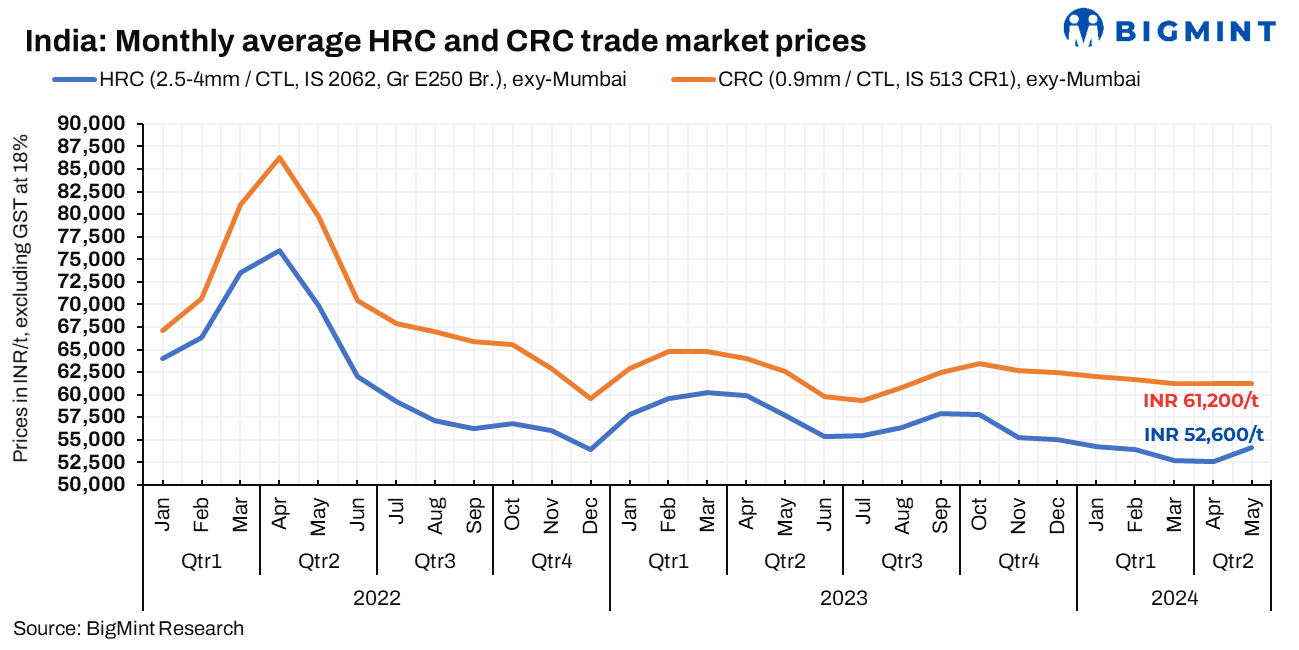

HRC (IS2062, Gr- E250 BR, 2.5-8mm)– INR 54,500-55,000/t exy-Mumbai

CRC (IS513, Gr-O/1, 0.9mm)– INR 59,800-61,500/t exy-Mumbai basis

Coil-to-coil prices, INR 750/t extra for cut to length (CTL). Excludes GST at 18%.

Market updates:

1. Volatile raw material prices: In April, in the ferro alloys market, the price of silico manganese (60:14 grade) in Raipur rose by 9% to INR 71,860/t driven by higher raw material prices and robust export demand amid disruptions in Australian supplies.

Iron ore fines from Odisha decreased by 3% in April to INR 4,780/t, while lumps rose by 1% to INR 6,580/t. Pellet prices, specifically DAP Raipur (Fe63%), increased by 5% to INR 9,680/t.

However, Australian premium HCC coking prices declined by 13% to $260/t CFR India due to price volatility, reducing India’s coking coal imports, as buyers became cautious amid decent inventory.

2. Maintenance shutdown at HSM: Indian mills have temporarily halted exporting HRC to Southeast Asia and the Middle East due to maintenance runs impacting output from hot strip mills (HSM). A few mills took up a 15-day long maintenance in April, while one private mill opted for downtime in its cold rolling mills (CRM). The mills planned this strategically to counter low buying interest in both domestic and overseas markets, shared a few industry sources.

A major private steel producer is likely to take a maintenance shutdown at its HSM soon, or may delay it a little further into May, shared a few sources.

3. Export, import trends: There has been a slowdown in exports of bulk hot-rolled coils (HRC) and plates, according to recent data from BigMint’s vessel line-up data. Meanwhile, imports are nearing levels seen in the previous month.

BigMint’s weekly assessment, the HRC (SAE1006) export index, remains unchanged at $560/t FOB east coast. This index primarily focuses on offers to the Middle East (ME) and Vietnam. This suggests that mills are prioritising the domestic market over exports.

Similarly, global tensions in the Mediterranean region and sluggish end-user consumption have instilled caution among distributors and spot buyers. Consequently, many are opting for smaller, more frequent purchases to mitigate price risks in the EU. Indian mills are refraining from exporting to the region, with price indications for HRC (S275, 3mm) at $625-635/t CFR Antwerp.

4. Need-based procurement in domestic market: In the domestic market, a trend of need-based procurement is evident among traders, wherein buyers are making smaller, immediate purchases tailored to specific requirements. Distributors are adjusting their offers upwards due to supply constraints, although they encounter resistance from buyers seeking to negotiate lower prices.

A market participant said, “Demand remains subdued in the traders’ segment, with buyers procuring only essential quantities and pushing for discounts despite attempts by sellers to raise prices.”