- Most tier-1 mills report crude steel production growth in Q2

- EBITDA margins hit due to weak steel prices, firm raw material costs

- Sustained CAPEX growth points to strong market fundamentals

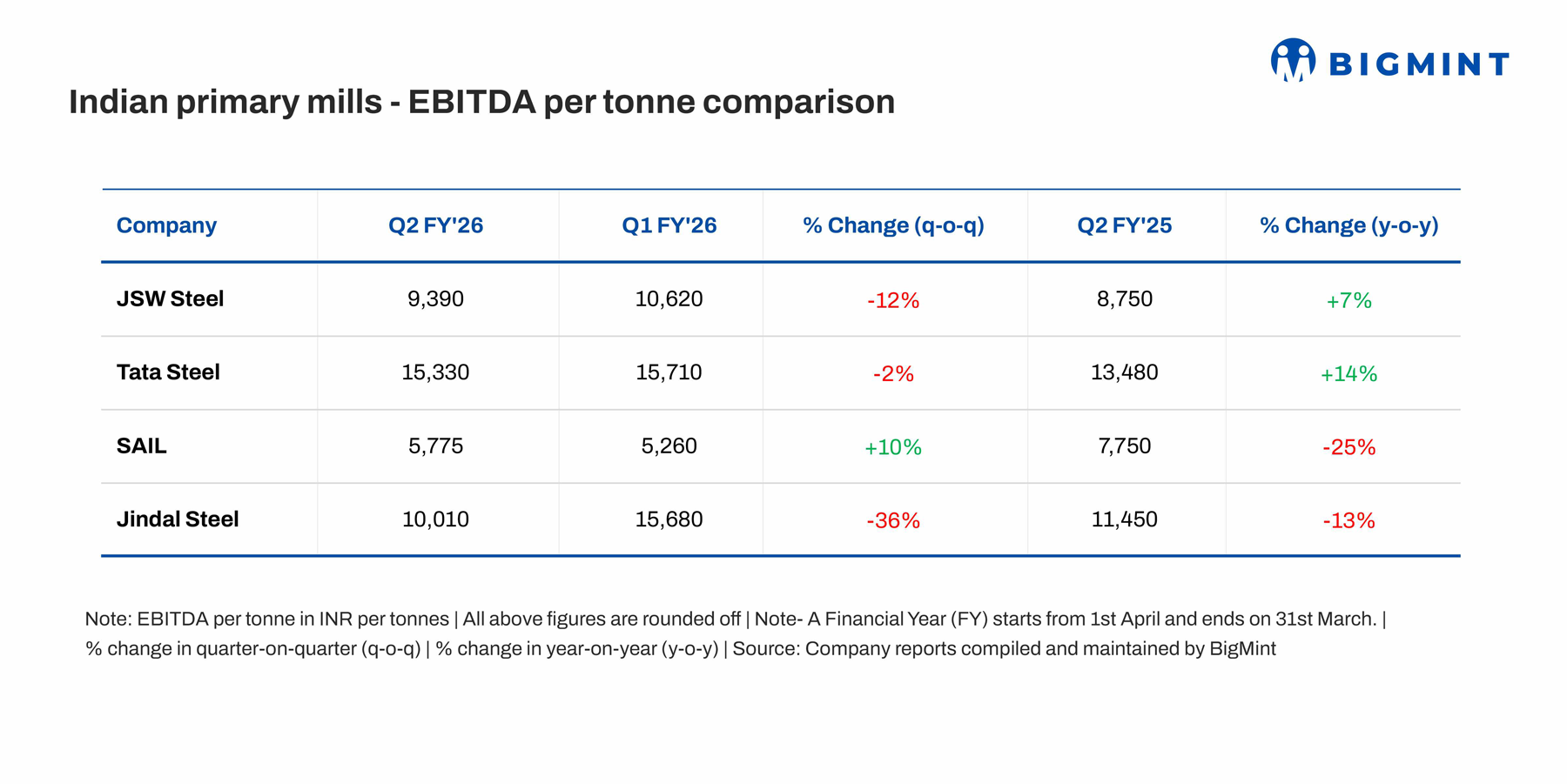

Morning Brief: In the Jul-Sep’25 quarter of the current fiscal (Q2FY’26) the primary steel mills in the country posted mixed results, with most of the Tier-1 companies reporting declines in EBITDA per tonne as domestic steel prices continued to trend down throughout the quarter amid monsoon blues, weak global sentiments and increasing inventories.

However, production and sales volumes showed some improvement on a q-o-q basis for most of the Tier-1 steel mills reflecting strong fundamentals. Despite domestic steel prices languishing at a 5-year low the country’s steel production has witnessed growth at a rate of over 12% in 7MFY’26, while consumption has surged at around 8% y-o-y.

Production performance

In Q2, the leading steel players, except SAIL and Jindal Steel, recorded growth in crude steel output. JSW Steel’s India operations produced 7.66 million tonnes (mnt), up 16% y-o-y. On a q-o-q basis, production increased by 9% due to fewer planned maintenance shutdowns compared to Q1.

Tata Steel’s crude steel production climbed up by 7% q-o-q to 5.4 mnt in Q2 from 5.07 mnt in the previous quarter. Similarly, on a y-o-y basis, the same increased by 7% as compared with 5.06 mnt in Q2FY’25.

SAIL’s crude steel output fell by 6% q-o-q to 4.6 mnt in Q2 from 4.9 mnt in Q1. Y-o-y, production fell by 4% from 4.8 mnt in Q2.

While AM/NS India’s production remained flat at around 1.8 mnt, Jindal’s production dipped by 4% q-o-q to 2 mnt in Q2 compared with 2.09 mnt in Q1FY’26. However, on a y-o-y basis, production inched up by 2% from 1.97 mnt recorded in Q2FY’25. Performance was impacted due to a prolonged monsoon as well as planned shutdowns.

Sales performance

Most of the Tier-1 mills recorded strong sales performances in Q2 reflecting sustained growth in steel consumption. Steel sales volumes reached 7.07 mnt, up 19% y-o-y. Q-o-q, sales rose by 10% from 6.43 mnt in the previous quarter. The share of exports stood at 10%. Sales of value-added and special products contributed 64% to the total.

Tata’s sales volumes surged 17% to 5.55 mnt in Q2 as against 4.75 mnt in the last quarter. The same went up by 9% from 5.11 mnt in Q2. SAIL reported saleable steel production growth of 4% q-o-q at 4.9 mnt in Q2 compared with 4.7 mnt in Q1, with sales increasing by 7% y-o-y from 4.6 mnt in Q2FY’25.

Similarly, Jindal Steel’s steel sales stood at 1.87 mnt in Q2, marking a 2% decline from 1.9 mnt in Q1. However, y-o-y, sales registered a marginal rise of 1% from 1.85 mnt recorded in Q2FY’25. AM/NS, too, recorded a y-o-y growth in sales from around 1.88 mnt in Q2FY’25 to 1.93 mnt in the last quarter.

EBITDA margins hit

The leading primary steel players reported declines in EBITDA per tonne due to the prevailing downward trend in domestic steel prices. JSW’s consolidated operating EBITDA for Indian operations in Q2 stood at INR 6,881 crore, which was an 8% decline q-o-q from the previous quarter’s INR 7,496 crore.

Tata Steel’s EBITDA jumped by 16% to INR 8,394 crore in Q2 from INR 7,263 crore in Q1. On a y-o-y basis, the same increased by 25% from INR 6,734 crore in Q2.

Notably, Jindal’s EBITDA stood at INR 1,875 crore in Q2, reflecting a 37% decline from INR 2,984 crore in Q1. Y-o-y, EBITDA was lower by 12% compared with INR 2,124 crore reported in Q2FY’25.

EBITDA margins were impacted due to the decline in steel prices and the sustained firmness in raw material prices. BigMint’s benchmark monthly average HRC prices in the domestic market declined by 3.4% q-o-q to around INR 47,800/t in Q2.

At the same time most of the key players reported a surge in raw material costs. Tata Steel’s raw material costs rose by 10% q-o-q to INR 12,961 crore in Q2 against INR 11,822 crore in the last quarter. SAIL’s Imported coal prices averaged around INR 17,300/t in October, up INR 700/t from August levels due to rupee depreciation against the USD. The coal index increased from 187 in September to 194 in October, reflecting firm market conditions. Higher iron ore prices added to cost pressures: even as NMDC announced price reductions, OMC auction prices continued to stay elevated despite weaker steel prices.

Outlook

Notably, despite shrinking of EBITDA margins, the steel majors reported significant expansion plans being undertaken. For example, Jindal’s commissioning of a second state-of-the-art blast furnace in Angul, Tata Steel’s Kalinganagar expansion, SAIL’s ISSCO expansion and JSW’s foray into the electrical steel space as well as green hydrogen.

This shows the inherent confidence in sustained growth in the sector. In Q3, most of the steel majors expect a spurt in net sales realisations and EBITDA margins with the expected improvement in steel market conditions.

Leave a Reply