- Stainless steel capacity to reach 9.3 mnt by 2030

- Mills to rely on blended scrap, NPI optimisation

Rising domestic demand, increasing long product consumption, and recycling adoption are positioning India as a resilient and strategic stainless steel market.

At the session on stainless steel recycling during the International Material Recycling Conference (IMRC) 2026 in Jaipur, India, industry leaders discussed how global trade shifts, carbon policies, and raw material availability are reshaping stainless steel production and recycling. Key themes included demand outlook, scrap availability and quality, global supply chain disruptions, and the role of technology and policy in strengthening the recycling ecosystem.

Global trade and European market insights

Joost Van Kleef, Commercial Director, Oryx Stainless Steel, described Europe as facing tight margins, high import penetration, and contracting flat product consumption. With CBAM fully operational from January 2026, low-carbon, scrap-based production will be incentivised while nickel pig iron (NPI) and billet imports may face carbon-related costs. Van Kleef highlighted the shift toward regionalised trade patterns and the growing importance of compliance and sustainability.

Mahiar Patel, Managing Director, Cronimet Singapore, noted that US and European scrap retention policies are tightening export flows. He emphasised that high-quality scrap, blended inputs, and Zurik remain critical to maintaining production flexibility, particularly as NPI supply fluctuates and nickel prices remain volatile.

India: Strong domestic growth, technical advancement

Gopal Gupta, Managing Director, Laxcon Steel, highlighted stainless steel as a critical material for infrastructure, defense, and industrial projects. Long products such as rebars, fasteners, and seamless tubes are seeing accelerated demand driven by tunnels, coastal projects, and government initiatives. India’s per capita stainless consumption remains 3.4 kg, below the global average of 5.8 kg, indicating substantial growth potential. Despite challenges of low capacity utilisation (~65%), energy costs, and logistics inefficiencies, the market is expanding steadily.

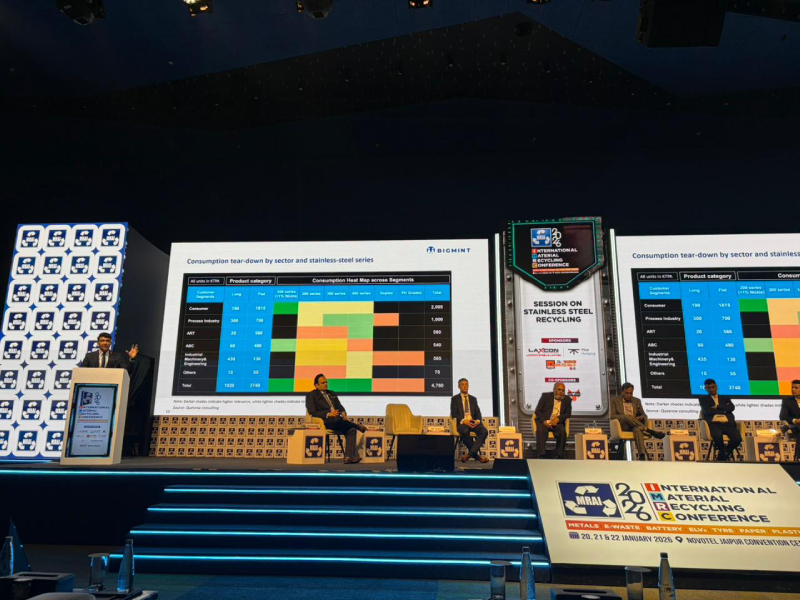

Dhruv Goel, CEO, BigMint, presented production and capacity data: installed capacity was 7.7 mnt, melt production 4.2 mnt, and consumption 4.9 mnt in FY’25. Long products represent 20% of consumption, flat 80%. SS scrap imports reached 1.3 mnt, domestic generation was 0.6 mnt. Ferro chrome consumption was 0.8 mnt, ferronickel/NPI 0.5 mnt, and other alloys 0.1 mnt. India’s capacity is expected to rise to 9.3 mnt by 2030, with 300-series remaining dominant. Tightening export regulations in supplier countries may challenge scrap availability.

Rohit Kumar, Executive Director, ISSDA, discussed technological advancements enabling Indian mills to produce high-performance grades (super-austenitic, duplex, super-duplex and 400-series). NPI feed is typically 8-20%, depending on nickel content, and blended scrap use allows flexibility in maintaining grade specifications for aerospace, defense, and process industries.

Rajamani Krishnamurti, President, ISSDA, emphasised stainless steel as both a strategic material and sustainability enabler. Lifecycle cost (LCC) procurement ensures infrastructure projects are durable, with minimal maintenance, reducing fiscal and environmental burden.

Akshay Agarwal, Director, CMR Green Technology, highlighted Zurik scrap’s strategic role for induction furnaces, despite small volumes. He noted that blended and shredded scrap is increasingly important amid supply scarcity and rising global NPI usage. Indian mills are slowly adapting to flexible scrap feeds as prices rise and availability fluctuates.

Market dynamics and outlook

India’s stainless steel production is projected to reach 9.3 mnt by 2030, supported by domestic scrap, imports, and NPI. Long product adoption is growing rapidly in infrastructure, defense, and industrial applications. Circular economy initiatives, technical sophistication, and policy alignment, including CBAM awareness and lifecycle costing, will enhance competitiveness, sustainability, and global leadership. Supply risks from geopolitical uncertainties, volatile nickel prices, and export controls in key source countries are likely to persist, reinforcing the importance of blended scrap and NPI optimisation for Indian mills.

Leave a Reply