-

Prices rise about 40% in CY’25 on tight inventories, speculative positioning

-

Miners favour existing assets, acquisitions over greenfield investment

-

China’s copper demand shifting towards policy-driven energy, technology sectors

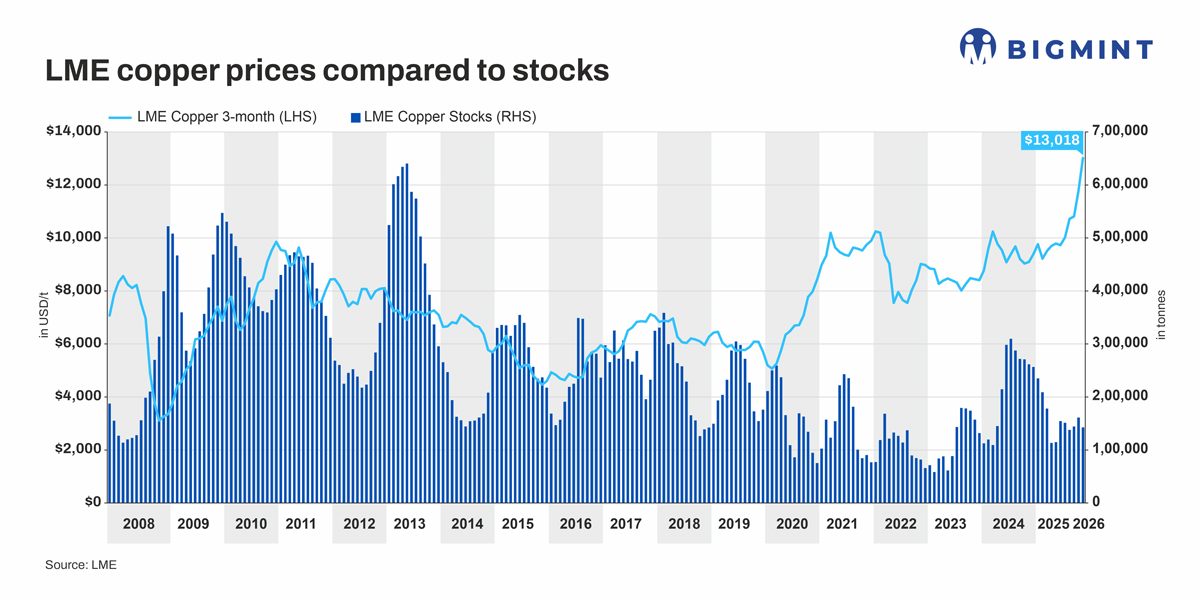

Morning Brief: Copper prices have risen sharply over the past year and the first month of 2026, touching a record of $13,310/t on 14 January, on the London Metal Exchange (LME) and reviving talk of a new supercycle. Visibly tight inventories, repeated supply disruptions and the long-term promise of electrification have combined to create a powerful narrative of scarcity.

Yet the recent price action also reflects a set of short-term distortions and cyclical forces that are easy to overlook when momentum is strong. The result is a market that looks convincingly tight on the surface, but far less secure underneath, raising doubts about whether current price levels can be sustained.

China still dominates demand picture

China remains central to the copper story, but its role is evolving in ways that complicate the bullish case. The country still accounts for roughly half of global copper consumption, which means any improvement in sentiment around Chinese growth has an outsized impact on prices. Over the past year, government support for power grids, renewable energy, and advanced manufacturing has helped stabilise demand after a prolonged slowdown in its property and construction sectors.

However, the composition of Chinese copper demand is changing. Traditional uses linked to real estate and heavy infrastructure are no longer expanding at the pace recorded in previous cycles. In their place, demand growth is coming from cleaner energy systems, electric vehicles, and digital infrastructure. These sectors are structurally important but also more sensitive to policy shifts, profitability pressures, and overcapacity. Market estimates say that Chinese refined copper demand has fallen by 8% y-o-y in the fourth quarter of 2025, suggesting that stimulus effects recorded at the beginning of the year have begun to fade, even as prices have continued to rise. This disconnect is important, because China still sets the tone for the global market.

Supply constraints are real but uneven

On the supply side, the arguments for higher prices appear more convincing at first glance. Global mine production has struggled to grow, and output has been repeatedly hit by operational issues at large assets.

World copper mine production rose about 1.2% in the 10 months to October 2025, compared to the same period in the previous year, while mine production rose about 2.6% to 22.3 mnt for 2024, with miners operating at about 80% of total capacity. At the same time, the industry is contending with a gradual but relentless decline in ore grades. Lower quality ore requires more material to be processed to produce the same amount of copper, driving up energy use, water consumption and operating costs. Over time, this erodes supply resilience and reinforces the perception of structural tightness.

Yet supply tightness is not uniform across the market. Scrap availability tends to improve quickly when prices rise, and recycled copper has already begun to offset some of the pressure on refined metal. This response does not solve longer term supply challenges, but it does soften the immediate balance and limits how far prices can run in the short term.

Why miners are not rushing to invest

Perhaps the clearest signal that prices have moved ahead of fundamentals is the muted response from miners. Despite copper trading well above historical incentive levels, there has been no surge in approvals for large new greenfield projects. Instead, companies have focused on maximising output from existing assets, pursuing incremental brownfield expansions and looking to mergers and acquisitions as a way to secure future copper exposure. While miners have operated at about 78% of total capacity in 10MCY25, utilisation rates have averaged about 81% over 2021-24.

This restraint reflects hard lessons from past cycles, when aggressive investment at the top of the market destroyed shareholder value. It also reflects today’s operating reality. New copper mines face long and uncertain permitting processes, rising opposition from local communities and increasing environmental scrutiny. In many producing countries, resource nationalism has become a material consideration, with governments seeking higher taxes, royalties or greater state involvement in mining projects. Together, these factors raise the cost of capital and make long-dated investments difficult to justify, even in a high price environment.

Distorted signals from inventories and policy

Recent price strength has been amplified by factors that have little to do with underlying consumption. The threat of tariffs on refined copper imports into the United States has distorted global trade flows, pulling material into US warehouses and creating a sharp premium between American and international prices. This has left inventories outside the US unusually tight, reinforcing the perception of scarcity even as stocks within the US have climbed to elevated levels.

Speculative activity has added another layer of volatility. Copper has attracted a disproportionate share of inflows into base metals, reflecting its strategic appeal and strong momentum. In a market that is smaller and less liquid than oil, such flows can push prices well beyond levels implied by near-term supply and demand, increasing the risk of a sharp reversal when sentiment shifts.

Long-term demand story remains intact

None of this undermines copper’s importance over the next two decades. Demand growth linked to electrification, renewable power, electric vehicles and grid expansion is likely to be substantial, and copper has few viable substitutes in many high-performance applications. Efficiency gains and material substitution can slow demand growth at the margin, but they are unlikely to offset the scale of new uses implied by energy transition targets.

That said, high prices are already influencing behaviour. Greater scrap collection, product redesign and selective substitution with aluminium are becoming more common, particularly in wiring and automotive applications. These responses do not negate the long term bull case, but they do cap near term demand and make sustained price spikes harder to maintain.

Outlook

Copper’s rally has been driven by a powerful mix of genuine long-term concerns and short-term distortions. Stagnating mine supply, declining ore quality and rising political risk all point to a structurally tighter market over time. At the same time, current prices reflect optimistic assumptions about demand, particularly in China, and are being supported by inventory dislocations and speculative flows that are unlikely to persist indefinitely.

The most likely outcome is a period of correction and consolidation rather than a collapse. Prices above current levels look difficult to sustain without clearer evidence of persistent deficits, but a sharp and lasting downturn also seems unlikely given the strength of the long-term demand story. Copper remains a metal with a compelling future, but the present rally appears to have run ahead of what near term fundamentals can comfortably support.

Leave a Reply