- Chinese mills eye ninth round of met coke price hike

- Domestic coke market remains stable amid sufficient supply

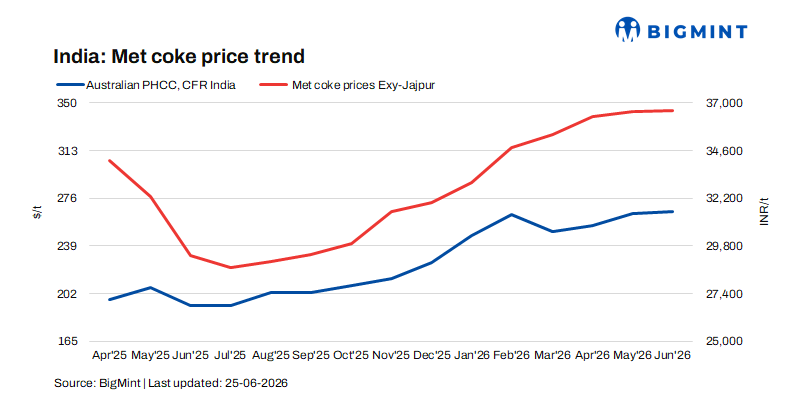

India’s imported met coke market showed a marginal recovery during the week ended 25 June 2026, supported by firm international coke prices and rising raw material costs.

BigMint’s assessment for Indonesian BF-grade coke (65/63 CSR) increased by around $1/t w-o-w to nearly $319/t CFR India, as suppliers raised offers amid improving global sentiment. FOB offers were reported around $294-295/t, with freight levels at $24-25/t; however, spot deals remained limited as buyers await clarity on the government’s upcoming anti-dumping duty announcement.

Market participants highlighted that “prices remain at comfortable levels, with demand steady but supply availability relatively tight. While end users are showing interest in securing bulk imports in advance, buying activity is expected to remain moderate during July-August due to monsoon-related seasonal slowdown.”

China coke market

China’s coking coal and coke markets remained resilient w-o-w, supported by constrained supply and stable steel mill demand. Slow mine restarts, frequent safety inspections, and limited supply recovery continued to support coking coal prices, while high raw material costs pressured coke producers and led some plants to restrict output.

Improved blast furnace operations and higher pig iron production kept steel sector demand firm, resulting in low coke inventories. The ongoing supply-demand imbalance has supported, notably the eight round of price hike was accepted with hike amounting to RMB 55/t($ 7/t), the initiation of the ninth round of coke price hikes, keeping the near-term outlook positive

Domestic market stable amid comfortable availability

Contrary to the imported market, India’s domestic BF-grade met coke prices remained stable due to balanced supply-demand conditions and comfortable inventory levels. Eastern India BF-grade coke prices remained steady at around INR 36,500/t ex-Jajpur, while western India prices held at INR 34,000/t ex-Gandhidham due to regional demand support.

Foundry-grade coke prices also remained unchanged at INR 36,400/t ex-Rajkot, supported by consistent foundry demand. Stable domestic availability has limited the scope for price increases despite rising international cost pressures.

Pig iron market: Firm fundamentals support sentiment

Australian Premium Hard Coking Coal (PHCC) prices edged higher by $1/t w-o-w to $244/t FOB Australia, reflecting steady supply-side support. In the pig iron market, demand showed some moderation due to cautious downstream buying; however, improved auction participation indicated stronger sentiment.

In the recent SAIL-Bokaro auction on 24 June, 14,000 tonnes of steel-grade pig iron were fully booked at an average of INR 36,400/t ex-works, up by INR 800/t from the previous auction, indicating improved buyer confidence and firm underlying fundamentals.

Outlook

The met coke market is expected to remain firm in the near term, supported by elevated international coke prices, tight supply conditions in China, and firm raw material costs. Imported coke prices may remain supported ahead of the anti-dumping duty decision, while domestic prices are likely to stay range-bound due to comfortable availability. However, monsoon-related demand moderation and cautious buying behaviour may limit significant upside in July-August. Overall, the market is expected to remain balanced with a positive undertone.

Leave a Reply