- Manufacturing PMI hits decadal highs in July, Aug

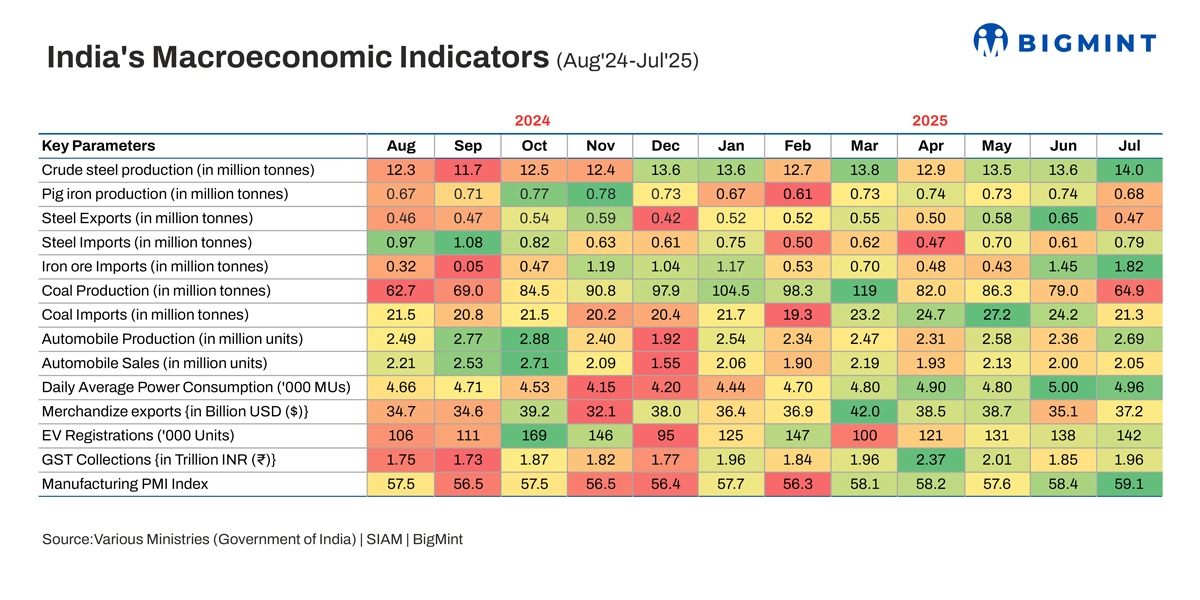

- Crude steel production rises 14% y-o-y in July

- GST reforms to boost consumer confidence ahead of festive season

Morning Brief: Despite global uncertainties and tariff- and trade-related turmoil, the Indian economy showed great resilience in April-July of the current fiscal (4MFY’26), especially in July, which points to the innate growth potential of the economy overcoming all external headwinds. India’s GDP growth accelerated to a robust five-quarter high of 7.8% in Q1FY’26 from 7.4% in Q4FY’25.

In Q1, the secondary sector, comprising manufacturing, electricity, gas, water supply and other utility services and construction posted strong gains, with manufacturing (7.7%) and construction (7.6%) both crossing the 7.5% growth mark. The Index of Industrial Production (IIP), which measures the change in the physical volume of output in the industrial sector over a specific period, witnessed an impressive 3.5% growth in July against 1.5% in June, driven by a 5.4% growth in the manufacturing sector.

BigMint tracks the domestic steel industry’s performance in July against the backdrop of key macroeconomic indicators:

Crude steel output surges

India’s crude steel production edged up by 3.3% m-o-m in July to 14 million tonnes (mnt), as per BigMint data. July output was almost 14% higher y-o-y, which shows the rapid expansion of production in the sector at a time when steel production in major economies, including China, is on the decline.

Production of crude steel during April-July was 54.19 mnt, an increase of 11.1% from the corresponding period of last year, as per steel ministry data. Finished steel output stood at 51.46 mnt, an 8.8% increase from the same period of last year.

However, merchant pig iron production contracted in July to 0.68 mnt against 0.74 mnt in June due to seasonal slowdown in the domestic market, cost and margin pressure amid strengthening coal and coke prices and tight met coke availability in the domestic market.

Steel exports drop, imports up m-o-m

India’s steel exports fell sharply m-o-m in July to 0.47 mnt against a high base in June. June recorded steel exports at 0.65 mnt, a 14-month high. In fact, Indian mills raised exports by 20% in 4MFY’26. However, exports dropped 19% y-o-y in 7MCY’25. In 4MFY’26, exports edged up y-o-y mainly due to the 26% surge in shipments to the EU despite the summer holidays and weak demand. The decline in Indian flat steel export prices and elevated offers of domestic EU mills turned Indian exports attractive.

On the other hand, steel imports increased nearly 30% m-o-m in July to reach a nine-month high of 0.79 mnt. Although imports dropped 8% y-o-y in 4MFY’26, the surge in inflows in May and July shows that despite the trade remedies such as the safeguard duty and DGTR proposal of AD duty on Vietnamese hot-rolled flat products imports have been difficult to contain. This is due to high domestic demand (which rose nearly 8% y-o-y in Q1FY’26) and weak demand in other countries, as well as higher imports of semis.

Iron ore, pellet imports hit 6.5-year high

India’s iron ore and pellet imports rose sharply to 1.82 mnt in July, hitting a six-and-a-half-year high. The last time imports crossed this level was in January 2018 (1.95 mnt) and, prior to that, in February 2015. The drop in global iron ore prices supported imports. However, the key reasons were competitive offers for high-grade pellets from the Middle East, supply bottlenecks in key production hubs, and high freight costs from central India to the western mills. This cost disadvantage, especially when compared to falling global prices, tilted the scale in favour of pellet imports.

Coal production, imports decline

Overall coal production in July was 64.83 mnt as compared to 74.01 mnt during the same period of last year and close to 79 mnt in June, as per data from the Ministry of Coal. This was on account of early arrival of monsoon and excessive rains. The rainfall in Q1FY’26 was 156% which was 507% higher than Q1 of last year in some of the CIL subsidiaries, which impacted coal mining operations, according to a note from the coal ministry.

Despite the decline in coal production in July, coal imports edged down. In fact, non-coking coal imports fell to a two-year low on marginal drop in coal-fired generation, high stocks at power plants and ports, as well as the downtrend in the sponge iron sector.

Moreover, generation from renewable sources surged. Hydropower recorded m-o-m growth of 30%, while nuclear power generation, too, increased in July. The share of solar and wind remained stable. The growth in renewable power generation was responsible for reducing dependence on imported thermal coal.

Mixed trends in auto industry

India’s automobile industry witnessed a mixed trend in July, with total production and passenger vehicle (PV) sales registering modest growth, while two-wheelers remained largely flat and tractors posted a decline. The market dynamics reflected a combination of factors, including the monsoon’s uneven progress, festive season pipeline adjustments, and base effect from last year.

According to data released by the Federation of Automobile Dealers Associations (FADA), total vehicle retail sales in July rose marginally by 2.3% y-o-y to 17.58 lakh units, compared to 17.18 lakh units sold in July 2024. Moreover, EV registrations continued to show steady growth, increasing by 10% y-o-y.

Average power demand drops

Average daily power consumption dropped marginally m-o-m in July, reflecting subdued growth due to early monsoon rains. Cooler weather reduced demand for cooling appliances, impacting overall electricity usage. Peak daily power supply also dipped to 220.59 GW from 226.63 GW in July 2024, signalling softer consumption patterns compared to last year.

Merchandise exports up

Despite an uncertain global policy environment, India’s merchandise exports recorded a growth of $2.1 billion m-o-m in July and in 4MFY’26 have grown substantially and much higher than the global export growth. Major drivers of merchandise exports included engineering goods, electronics goods, drugs and pharmaceuticals and organic and inorganic chemicals.

GST collections rise

Fiscal and revenue trends were mixed in July. GST collections increased in July supported by higher gross import revenues. However, India’s fiscal deficit has widened sharply, reflecting weaker non-tax revenues and a surge in interest payments.

Manufacturing PMI at 16-month high

Business activity indicators remained robust in July. Manufacturing PMI climbed to a 16-month high of 59.1, supported by stronger new orders, output, and inventories. The services PMI also rose to an 11-month high of 60.5, indicating sustained momentum across both sectors.

Outlook

The HSBC India Manufacturing Purchasing Managers’ Index (PMI) climbed to 59.3 in August from 59.1 in July, reaching the highest level in 17-and-a-half years. This was on account of ongoing improvements in demand continuing to underpin robust increases in factory orders and production. Therefore, growth in overall manufacturing and steel production will continue on the back of strong demand.

Similarly, auto production and sales will receive a boost, with Onam signalling the onset of the festive season beginning late-August. Consumer demand is also set to tick up ahead of the festive season. Moreover, the indirect impact of the landmark GST reforms on the steel sector is expected to be largely positive and will be closely watched.

Leave a Reply