- Rising raw material prices support wire rod tags

- Prices to continue climbing on lower inventories

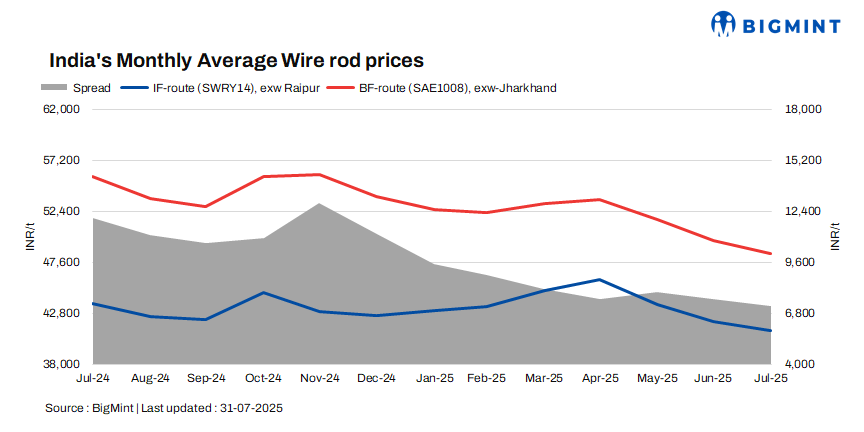

Indian wire rod prices showed a mixed trend in July 2025. In the induction furnace (IF) route segment, wire rod prices witnessed an increase of INR 300/tonne (t) ($3/t) to a monthly average of INR 40,800/t ($466/t) exw-Durgapur and plunged by INR 800/t ($9/t) to INR 41,100/t ($470/t) exw-Raipur as compared to June levels. Spot trade reference prices stood at INR 42,100/t ($481/t) exw-Raipur and INR 41,000/t ($468/t) exw-Durgapur as on 4 August 2025.

Notably, for IF-route wire rods, Raipur (central region) and Durgapur (eastern region) are the major supply centres catering to various other markets across the country. The cumulative daily wire rod production capacity in these two markets is around 20,000 t, as per data maintained with BigMint.

Wire rod prices (5.5-6mm, SAE1008) were assessed at INR 48,800/t ($558/t) exw-Jharkhand, as per BigMint’s assessment on 1 August 2025.

Factors behind market dynamics

Raw material prices show mixed trends: Indian steel billet and sponge iron markets witnessed mixed trends amid improvements in finished steel demand and trade activities, specifically from the latter half of the month. Rising raw material costs, such as those of iron ore and pellets, supported prices.

Considering the Raipur market as a benchmark, billet prices fell by INR 900/t ($10/t) m-o-m to INR 37,000/t ($423/t), while sponge iron (PDRI FeM 80% +/- 1) saw a surge of INR 900/t ($10/t) to INR 23,700/t ($271/t) exw. This was because some sponge iron manufacturers undertook maintenance shutdowns in mid-July, which led to material shortages in Raipur. (Prices are on a monthly average basis.)

Moderate buying seen throughout Jul’25: After sluggish inquiries in the first half of July 2025, buying interest for wire rods picked up sharply in Raipur and Durgapur, helped by strong downstream demand from galvanised and binding wire sectors. This allowed manufacturers to sustain elevated prices amid rising raw material costs.

By mid‑July 2025, major producers of wire rods in key hubs such as Raipur and Durgapur cleared a major backlog of previously booked orders and secured strong cover for upcoming demand. This freed them from the pressure of excess inventories and enabled price hikes.

Primary mills see weak demand: In the blast furnace (BF) segment, wire rod prices (5.5-6mm, SAE1008) dropped by INR 1,200/t ($14/t) m-o-m to an average of INR 48,400/t ($553/t) exw-Jharkhand in July.

Wire rod demand remained subdued last month due to the monsoon-led slowdown and weak offtake from the construction and auto sectors. Buyers largely stayed on the sidelines due to price volatility and market uncertainty. While prices trended down for most of the month, late-July saw a slight uptick as mills hiked list prices.

Outlook

It’s been expecting that prices to increase in the near future due to reduced inventory pressure. Additionally, the gradual retreat of the monsoon from different parts of the country in late August and a recovery in construction activity are expected to keep prices supported.

Leave a Reply