- Export growth, quality issues, import reduction may cap stock build-up

- Prices down 16% since Jun’24, possibility of further drops remain limited

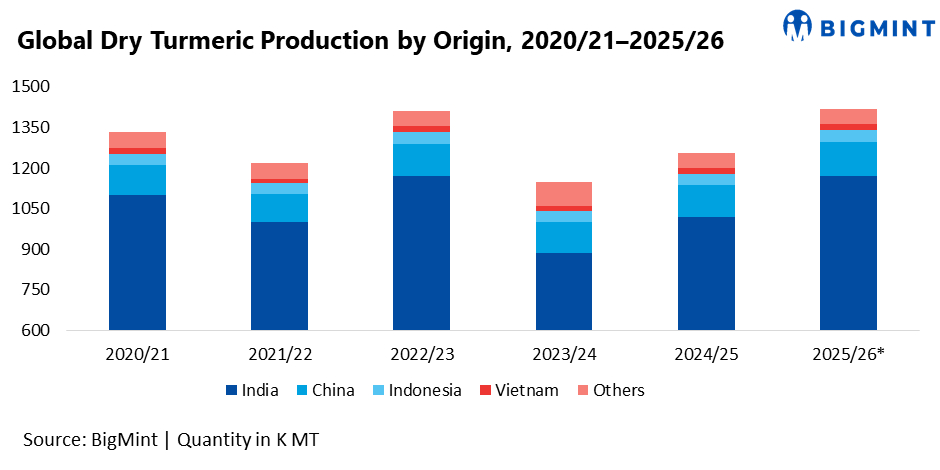

India’s turmeric cycle is shifting from deficit-driven tightness to a rebuilding phase in 2025-26. As presented at the International Spice Conference 2026 (ISC), India accounts for nearly 80% of global dry turmeric production, making domestic crop swings the dominant global price driver. After a sharp production dip in 2023-24, output is recovering strongly, but inventories remain below comfort levels.

Indian dry turmeric production moved from 1.10 million tonnes (mnt) in 2020-21 to 1.00 mnt in 2021-22, rose to 1.17 mnt in 2022-23, then fell sharply to around 0.90 mnt in 2023-24 due to adverse weather. Production recovered to roughly 1.02 mnt in 2024-25 and is projected at about 1.17 mnt in 2025-26 — a 15% y-o-y increase. The rebound is acreage-led, with area expansion estimated at nearly 20%, especially in Maharashtra. However, excess rains reduced yields by about 5% and raised aflatoxin concerns, affecting quality-sensitive export markets.

Globally, dry turmeric production is projected at around 1.41-1.42 mnt in 2025-26, up from roughly 1.26 mnt last season. Since India contributes close to four-fifths of world supply, a 100,000-150,000 t swing in Indian production significantly alters global availability and price direction.

On the demand side, domestic consumption remains structurally strong, supported by food processing, masala blends, oleoresin extraction, and nutraceutical demand. Based on the stock-versus-consumption data presented, domestic usage has been broadly in the 800,000-900,000 t range in recent seasons. Export demand also remained firm in 2025, with shipments rising 11%, while imports declined sharply by 53%. The combination of stronger exports and limited imports restricted domestic availability and prevented meaningful stock rebuilding.

The small 2023-24 crop of 0.90 mnt triggered a sharp drawdown in inventories and pushed prices higher. Even though the 2024-25 crop recovered above 1.0 mnt, stocks continued to decline due to export growth and weak imports. As a result, carry-forward stocks entering 2025-26 remain in the lower band compared to 2020-22 levels, and the stock-to-consumption ratio has not yet returned to historical comfort zones. Low stock ratios have historically attracted speculative participation, increasing volatility.

Prices have corrected about 16% since June 2024 as production expectations improved, but the downside remains limited unless inventories rebuild meaningfully. Structural demand for higher-curcumin varieties continues to support value-added segments, as curcumin content (0.5-8%) determines suitability for food, pharma and nutraceutical buyers. Rising regulatory scrutiny is also increasing compliance requirements, with pesticide parameters expanding to 521 by 2026, pushing exporters toward traceable and residue-free supply chains.

Looking ahead, the 1.17 mnt crop theoretically allows rebuilding of 100,000-150,000 t of stocks if exports stabilise and domestic consumption does not accelerate further. However, if exports continue growing at double-digit rates and quality issues restrict effective supply, stock rebuilding may remain slower than expected. The market direction in 2026 will therefore depend less on acreage and more on how quickly the stock-to-use ratio improves.

In summary, turmeric has moved out of an acute deficit phase, but it has not yet reached surplus comfort. Production recovery is visible, yet carry-forward stocks remain tight. For traders and processors, close monitoring of arrivals, export pace and stock levels will be critical, as inventory rebuilding — not just output — will determine price stability in the coming cycle.

Leave a Reply