- China remains largest producer but output falls by 4% m-o-m

- Tight Indonesian bauxite quotas restrict global alumina growth

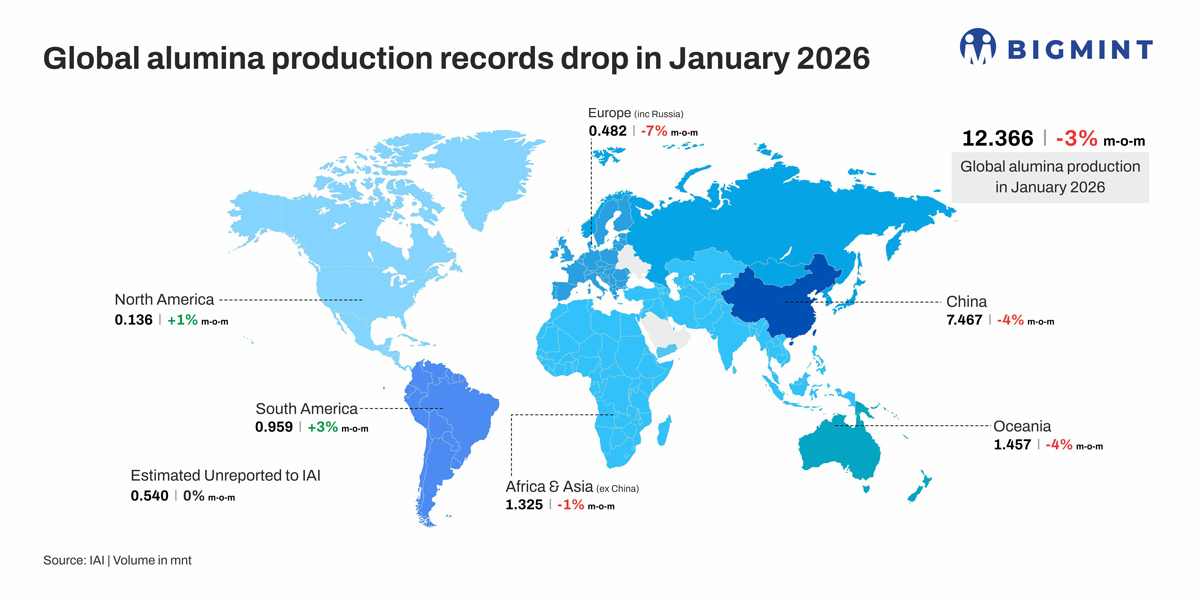

Global metallurgical alumina production declined by 3% m-o-m to 12.366 million tonnes (mnt) in January 2026 from 12.755 mnt in December 2025. The moderation reflects lower output levels at the start of the year compared to the previous month, driven by raw material constraints and the slow ramp-up of additional capacities.

On a y-o-y basis, production increased by around 1.1% from 12.231 mnt in January 2025, indicating relatively stable global refinery operations despite the month-on-month decline.

Factors influencing the drop in output

Global metallurgical alumina production declined by 3% m-o-m to 12.366 mnt in January 2026 from 12.755 mnt in December 2025. The contraction was largely attributed to raw material constraints and the slower ramp-up of newly commissioned capacity across several regions. A number of refinery projects, particularly in Indonesia and other emerging producers, remain in early commissioning stages and have yet to achieve stable operating levels. Tight bauxite availability — especially in Indonesia, where mining quotas remain insufficient to support expanding refining capacity — further restricted feedstock supply. As a result, the average overseas operating rate edged lower to 79.37%, leading to softer monthly output despite steady underlying demand. On a y-o-y basis, however, global production remained higher, reflecting relatively stable broader refinery operations.

In Indonesia, new capacity development continues, with PT Kalimantan Alumina Nusantara constructing a 1-1.2 mnt per year refinery in West Kalimantan, expected to begin phased production in late 2026 or early 2027. However, Indonesia’s bauxite quota remains capped at 18 mnt, sufficient mainly for the country’s existing 7 mnt of operating alumina capacity. With an additional 2 mnt of refining capacity under development, estimated bauxite demand could rise to around 24 mnt, potentially constraining the ramp-up of new facilities due to limited raw material supply.

In the Middle East, Saudi Arabia is preparing for structural changes in its aluminium value chain. Chuangyuan Metal plans to develop an integrated aluminium industrial park, including alumina refining, aluminium smelting, power generation, and downstream processing. Phase I includes 500,000 t of aluminium smelting capacity, with construction expected to begin by end-2026 and production targeted before end-2028. Saudi Arabia currently operates a single 2 mnt per year alumina refinery, primarily serving domestic smelting requirements, with surplus volumes exported regionally. The addition of new smelting capacity is expected to gradually alter regional alumina trade flows.

In Africa, Ghana has advanced plans for its first large-scale alumina refinery, aiming to transition from raw bauxite exports to value-added processing. The proposed refinery would directly supply alumina to the Volta Aluminium Company (VALCO), supporting domestic aluminium production and broader industrial cluster development. The project is expected to commence in 2026, with a target to restore VALCO’s annual capacity to above 200,000 t by the end of 2028.

In the United States, a $450 million investment was announced to support the country’s only remaining alumina refinery and establish a domestic gallium supply chain. The refinery will process imported Jamaican bauxite into alumina, targeting annual output exceeding 1 mnt, which could meet nearly 40% of US demand. The project also includes the construction of a gallium extraction line with a planned capacity of up to 50 t per year, strengthening supply security for defense, aerospace, and high-tech industries.

Outlook

Global metallurgical-grade alumina production is expected to moderate in February compared with January, while remaining slightly higher than the same period last year. The operating rate is projected to ease marginally, reflecting softer monthly output levels. The anticipated decline is primarily attributed to the shorter calendar month, along with the fact that some newly commissioned capacity is still in the ramp-up phase and has yet to reach stable utilisation levels.

Leave a Reply