- Benchmark HRC trade prices rise by INR 300/t w-o-w

- IF rebar softens, market fails to digest earlier list price hikes

- Weak export demand, declining Chinese production weigh on prices

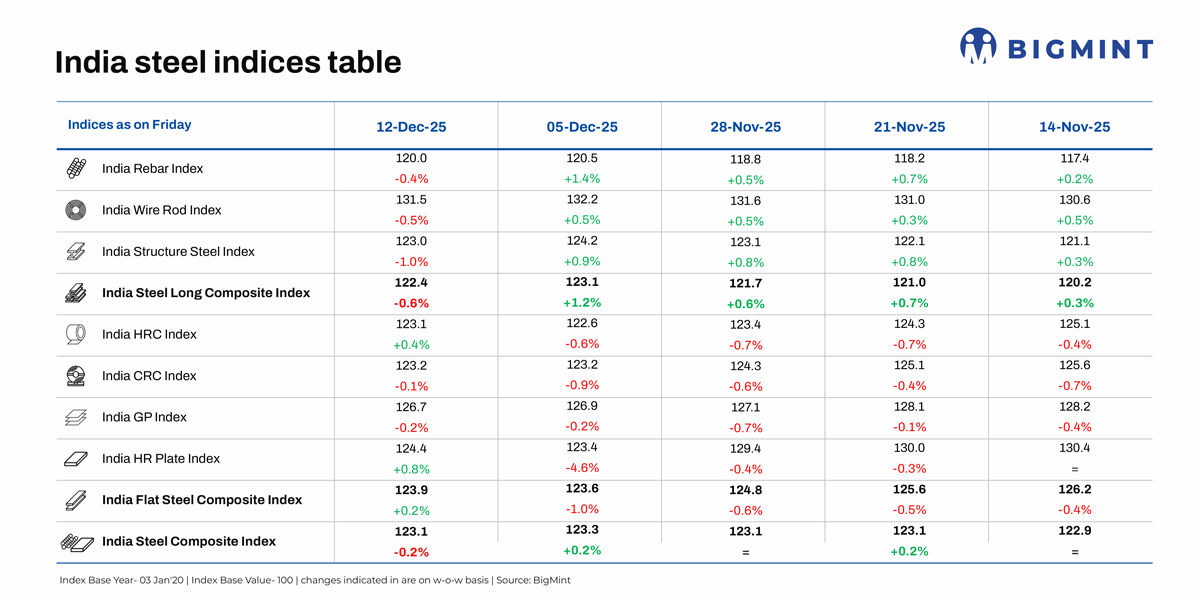

Morning Brief: BigMint’s India steel composite index pared gains witnessed last week to fall back to late-November levels, as per latest assessments on 12 December 2025, with steel market conditions remaining weak. Domestic billet prices across markets dropped in the range of $3-11/t w-o-w last week, and sponge iron and metallics, too, saw a decline.

The flats composite index rose marginally after declining 1% last week while the longs index saw a correction of 0.6% w-o-w. With domestic iron ore and global coking coal prices staying very firm, mills are under margin pressure.

Highlights of price movements

HRC prices stable w-o-w: BigMint’s bi-weekly assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) saw a slight correction of INR 100/t ($1/t) w-o-w on 9 December but edged up by INR 300/t on 12 December, settling at INR 46,000/t. Trade prices reflected stability, albeit at historically low levels, after the Tier-1 mills rolled over HRC list prices for December.

The CRC index, however, shed 0.1% last week compared to 0.9% the previous week.

The domestic HRC market continues to see moderate activity but exports are subdued, with European quotas already exhausted and no new offers emerging, while demand in the Middle East remains lacklustre.

No fundamental recovery in rebar market: On a weekly basis, IF-route rebar prices decreased up to INR 1,000/t across regions except in Mumbai where prices increased by INR 500/t, as per BigMint assessment. Buyer activity was limited as they preferred need-based procurement. Manufacturers preferred to lower their offers or increase trade discounts. Mill inventories are currently assessed at around 8 to 12 days across regions.

Trade-level BF rebar prices increased by INR 500/t ($6/t) w-o-w to INR 47,500/t ($525/t) exy-Mumbai on 12 December. Prices increased as mills raised offers despite weak demand. Buyers were reluctant to accept the higher offers resulting in slow trade activity. Market participants informed BigMint that buyers were struggling to absorb the price hike by mills earlier in the month. Amid limited procurement and cautious purchases overall sentiment was subdued.

The BF-IF rebar price gap narrowed w-o-w to around INR 5,500-6,000/t ($64-70/t) in Mumbai. IF rebar has a dominant market share in India.

Outlook

The main drag on steel prices is, of course, weak global sentiments and the decline in Chinese production, which might weaken further in December and early-January due to off-season and construction sector slowdown. Export sentiments remaining weak for long due to regulatory uncertainties and weak demand in key countries is also not offering any support to domestic steel prices.

However, with around 8% y-o-y growth in domestic consumption, mills will try to offset margin pressure due to declining prices by achieving higher domestic sales.

Leave a Reply