- BigMint’s benchmark HRC prices drop INR 200/t w-o-w

- BF rebar trade prices stable, some mills raise tags in early Sept

- Market waiting for leading mills to revise HRC prices for Sept

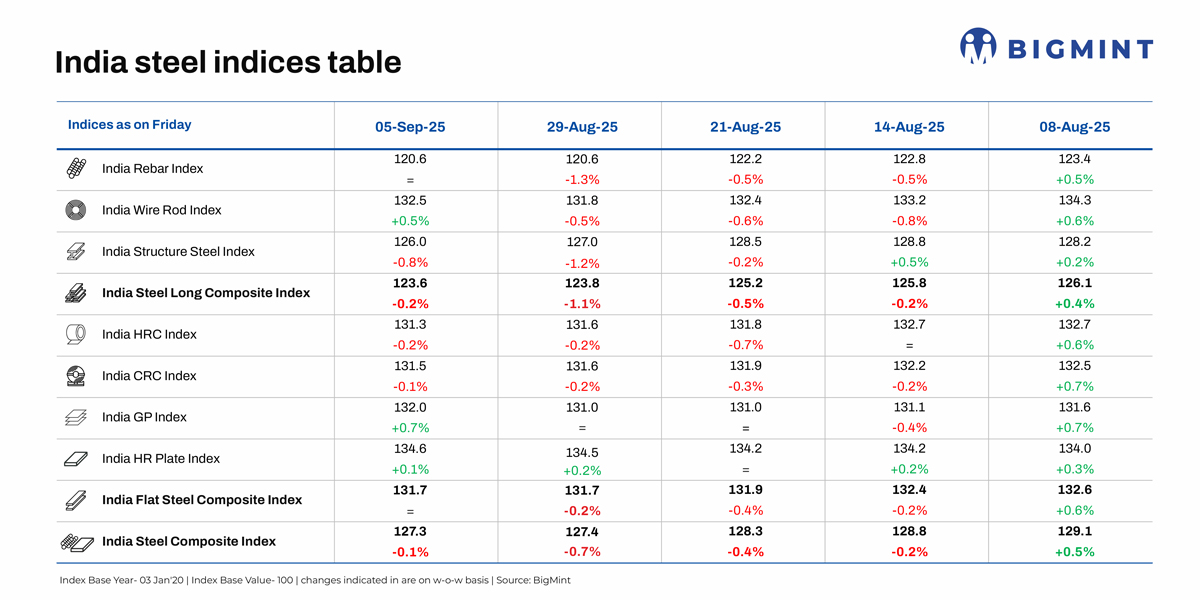

Morning Brief: BigMint’s flagship India steel composite index, a barometer of the domestic steel market, continued to decline w-o-w, remaining at nearly 5-year lows due to the steady downtrend in steel prices. Seasonal slowdown and global uncertainties have kept prices under pressure.

While the flat steel index remained stable w-o-w despite the 0.2% drop in the HRC sub-index, the longs index fell 0.2% w-o-w – dropping by two percentage points since mid-August 2025.

Steel price movements

HRC prices under pressure: BigMint’s benchmark assessment for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) fell by INR 200/t ($2/t) w-o-w to INR 49,500/t ($561/t) on 2 September against INR 49,700/t ($564/t) on 26 August. CRC (IS513, Gr O, 0.9 mm/CTL) prices fell by INR 200/t ($2/t) w-o-w to INR 56,800/t ($644/t) on Tuesday against INR 57,000/t ($646/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Sentiment in the trade-level HRC market remained subdued amid weak demand. Prices were rangebound w-o-w, further reflecting the lack of momentum in the market. The prevailing uncertainty prevented both buyers and sellers from making significant moves.

A source informed BigMint, “There is uncertainty regarding pricing, and the market is waiting for the mills to revise prices for September to get clearer market direction.”

Import volumes: India’s bulk imports of HRCs touched 381,189 t as of 30 August, based on vessel line-up data. Around 248,786 t of additional cargoes are expected by the end of September.

Notably, India’s total steel imports in July steel imports increased nearly 30% m-o-m in July to reach a nine-month high of 0.79 mnt. Although imports dropped 8% y-o-y in 4MFY’26, the surge in inflows in May and July shows that despite trade remedial measures such as the safeguard duty and AD duty on Vietnamese hot-rolled flat products, imports, overall, have been difficult to contain.

Mixed signals in rebar market: Trade-level BF rebar prices remained stable w-o-w at INR 47,300/t ($536/t) exy-Mumbai, as per BigMint’s assessment on 5 September. Prices are exclusive of GST at 18%. Demand remained sluggish in the trade channel last month, as heavy rainfall and waterlogging disrupted logistics and hampered market activity.

However, some of the leading primary mills increased prices by INR 1,000/t ($11/t) for early-September deliveries as against end-August, sources informed. Meanwhile, some mills rolled over their prices. Post-revision, list prices stood at INR 47,500-48,500/t ($538-549/t) on landed basis. It should be noted that mills had offered discounts/rebates to augment sales last month. Rebar inventories with Tier-1 mills remained largely unchanged m-o-m in early September.

Induction furnace (IF) rebar prices in key Indian markets witnessed a gradual decline in August amid subdued demand and monsoon-led disruptions. Demand remained largely need-based, with limited buying interest during the festive season. Manufacturers reduced list prices and offered discounts to clear inventory, which averaged 10 to 12 days across regions.

Outlook

Steel market fundamentals remain rock solid which is attested by the steady growth in crude steel production and consumption. Even imports have been going strong. The seasonal slowdown of the steel market has coincided with a phase of increased economic uncertainty, trade barriers and tariffs, as well as the gradual and deep slowdown that is being witnessed in major countries.

A pre-festive rebound in sentiment is surely awaited; however, amid abundant steel supplies in the domestic market and weak global steel prices, signs of a sustainable market recovery are still not in sight.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply