- Finished steel inventory holding periods hit 20-25 days

- Mills to focus on clearing existing stocks till mid-Jan’26

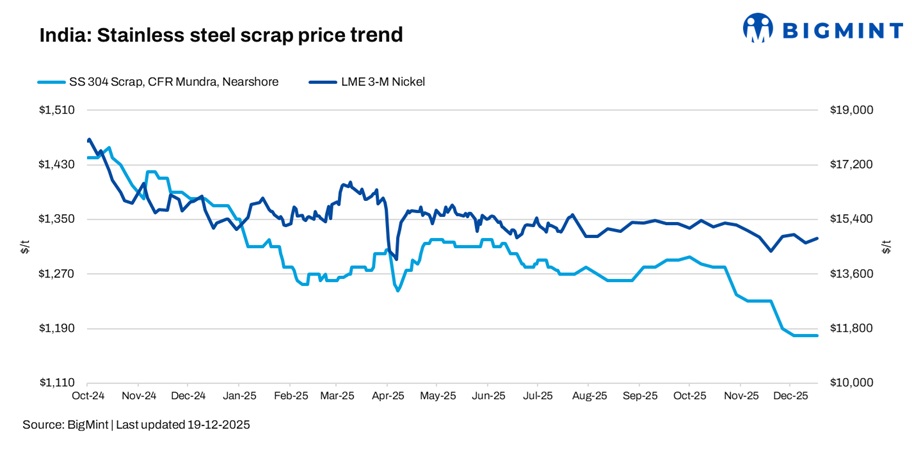

India’s stainless steel scrap market remained subdued in the week ending 19 December, driven by weak finished demand, with mills holding sufficient inventories and refraining from fresh bookings. Market conditions continued to be challenging, as wide bid-offer disparities limited deal closures and kept trading activity muted.

Market sentiments

Domestic 304-grade scrap was assessed by BigMint at INR 106,000/tonne (t) DAP Delhi, down INR 1,000/t, while imported 304-grade scrap prices from nearshore origins were at $1,180/t CFR Mundra, steady w-o-w.

Market participants indicated that finished stainless steel demand has weakened significantly in recent weeks, leading mills to scale back from scrap procurement. With mill inventories currently covering around 20-25 days of requirements, the immediate focus remains on liquidating existing stock through mid-January. Owing to the absence of demand for finished goods, scrap buying activity has remained largely muted.

According to mill sources, order bookings for 300-series stainless steel have declined sharply, prompting producers to scale back raw material procurement. Mills are currently refraining from purchasing 300-series scrap, including from captive yards, while restricting buying activity to 400-series and 201-grade scrap. Plants were heard to be adequately stocked with scrap, limiting near-term procurement requirements.

BigMint’s scrap assessments

- Nearshore-origin SS 316 scrap (loose): $2,380/t, down $20/t w-o-w.

- Nearshore-origin SS 201 scrap (loose): $620/t, steady w-o-w.

- Nearshore-origin SS 430 scrap (loose): $560/t, steady w-o-w.

- SS 316 scrap DAP Delhi: INR 206,000/t, down INR 1,000/t w-o-w.

- SS utensil DAP Delhi: INR 58,000/t, down INR 1,000/t w-o-w.

Global sentiments

US stainless steel scrap exports edged higher in September after several months of decline, though the rebound appears largely technical and limited in scope. Census Bureau data showed shipments rising 19.2% m-o-m to 24,000 t, marking the first increase since June. Despite the uptick, market participants remain cautious, citing weak domestic and export demand, seasonal headwinds, and thin margins, with a meaningful recovery unlikely before early 2026.

LME nickel

Benchmark three-month contract nickel prices on the London Metal Exchange (LME) were at $14,540/t on 19 November, down slightly by 0.4% from $14,604/t in the previous week. LME-registered nickel stocks stood at 253,938 t, a marginal 0.4% increase compared to the 253,032 t in the previous week.

Outlook

Stainless steel scrap prices are expected to remain under pressure in the rest of the month, as weak finished steel demand and cautious buying continue to limit trading activity. Prices are likely to remain at current levels, with any meaningful recovery deferred until demand fundamentals show clearer improvement.

Leave a Reply