- Mills say firm input costs driving prices upward

- Domestic stainless longs demand remains weak

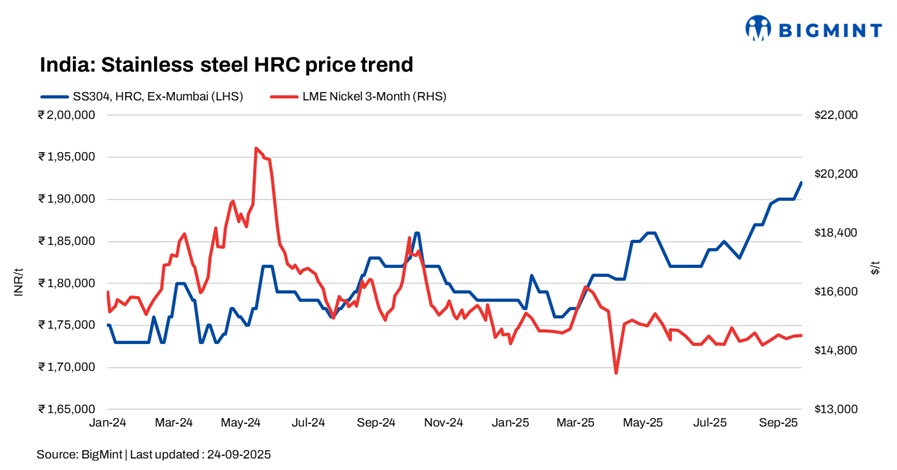

India’s stainless steel finished flats prices stayed firm w-o-w on the back of rising input costs, though demand remained moderate. Globally, major stainless steel producers announced mixed revisions in alloy surcharges for October 2025 deliveries.

- Acerinox cut 304 and 430 grades while lifting 316L and 201 series.

- Aperam raised surcharges on key grades, including a modest uptick in 304 and a stronger hike in 316L; its flat stainless steel capacity stands at 2.5 mnt annually.

- Outokumpu also raised 304 and 316L surcharges but lowered 430; the company has a melt capacity of 2.55 mnt.

BigMint’s assessed 304-series hot rolled coils (HRCs) at INR 192,000/t ex-Mumbai, up by INR 2000/t. While 304L black round bars (25-100mm) stood at INR 160,000/t, stable w-o-w.

In contrast, 316-series HRCs stood at INR 345,000/t and cold-rolled coils (CRCs) at INR 350,000/t, both steady w-o-w.

As per a market participant, “The stainless steel market remained sluggish, with US tariffs exerting only a limited impact. Weak demand continues to weigh on trade flows, keeping overall activity subdued.”

“The finished longs market remained largely silent, with demand continuing to stay dull. Production levels have been kept lower to match weak market activity, while the export market has also offered little support. Overall sentiment in the segment remains cautious, with limited buying interest from both domestic and overseas buyers”, a mill stated.

LME nickel tags remain range-bound w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,275/t, largely stable from last week’s $15,255/t. Nickel stocks at LME-registered warehouses stood at 230,454 t, up 1.8% compared to 226,434 t in the previous week.

Chinese stainless steel, NPI prices remain stable

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,500-13,900/t ($1,892-1,948/t) exw, while FOB tags of 304-grade CRCs were firm at $1,930/t.

Chinese portside prices of nickel pig iron (NPI) (8-12%) remained firm w-o-w at RMB 955/t ($133/t). Meanwhile, Indonesian FOB prices of NPI (12-14%) stood at $118/t.

Global trends

Stainless steel prices are expected to rise as nickel stabilizes around $15,000/t, providing a steady cost base ahead of the fourth-quarter peak season.

Market participants noted improving pricing power, with Tsingshan lifting export prices and boosting sentiment across Asia. Additional support is likely from Indonesia’s tighter control over production permits, which could limit supply.

Speculative fund activity in the nickel market may further lift prices, raising stainless production costs. Demand from downstream industries including home appliances and machinery remains firm. In China, stainless consumption rose 8.73% in August, underscoring recovery momentum. Looking ahead, the global stainless steel market is projected to expand at a 9.6% CAGR through 2031, supported by favorable policies and technological advancements.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices witnessed a slight decline of INR 26,000/t ($293/t) as compared to the previous assessment on 24 September. This was primarily due to a drop in global and LME futures prices along with fewer inquiries in the domestic market.

As per BigMint’s assessment on 24 September, ferro molybdenum prices in India were INR 3,084,000/t ($34,744/t) exw-India.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices rose INR 1,500/t w-o-w to INR 119,300/t ($1,344/t) exw-Jajpur.

At OMC’s ferro chrome auction, 1,650 t out of 3,300 t offered was sold. The material sold came from the larger lot (Cr:60-64%, 10-100 mm) at the base price of INR 117,500/t ($1,331/t) exw, according to officials. BigMint assessed ferro chrome (HC60%, 10-150 mm) prices at INR 117,800/t ($1,334/t) exw-Jajpur on 19 Sep’25.

Additionally, Vedanta-FACOR will conduct an auction for high-carbon ferro chrome chips (10-20 mm) on 24 September, with a minimum bid quantity of 25 t. BigMint assessed ferro chrome (HC 60%, Si: 4%, 10 -150 mm) prices at INR 117,800/t exw-Jajpur on 19 July.

Ferro silicon: Indian ferro silicon (70%) prices stayed largely stable last week, edging down slightly by INR 600/t ($7/t) as compared to the previous assessment on 15 September. Trading was largely quiet, as the majority of sellers were out of the market.

Ferro silicon prices in India were INR 88,400/t ($996/t) exw-Guwahati, as per BigMint’s assessment on 22 September. Bhutan’s prices too held steady w-o-w at same levels.

Ferrous scrap: India’s imported scrap market stayed weak and largely inactive, weighed down by poor steel demand, domestic DRI availability, and rupee volatility. Containerised shredded scrap offers were assessed at $360-365/t and bids around $350-355/t, leaving a wide gap.

Mills continued favouring local inputs like DRI and HMS, which were available at competitive prices, reducing reliance on imports. Traders noted no urgency for booking of fresh cargoes as subdued sentiment and weak currency kept buyers cautious. Compared to neighbouring markets like Pakistan, where tradable levels were higher, India’s market lagged behind, reflecting muted demand fundamentals and a wait-and-watch stance among buyers.

Outlook: Stainless steel prices are expected to increase in the near term due to currency fluctuations and rising raw material costs.

Leave a Reply