- Mills offer discounts, rebates to boost sales; imports add pressure

- Mills shift to 316 grade production amid favourable cost dynamics

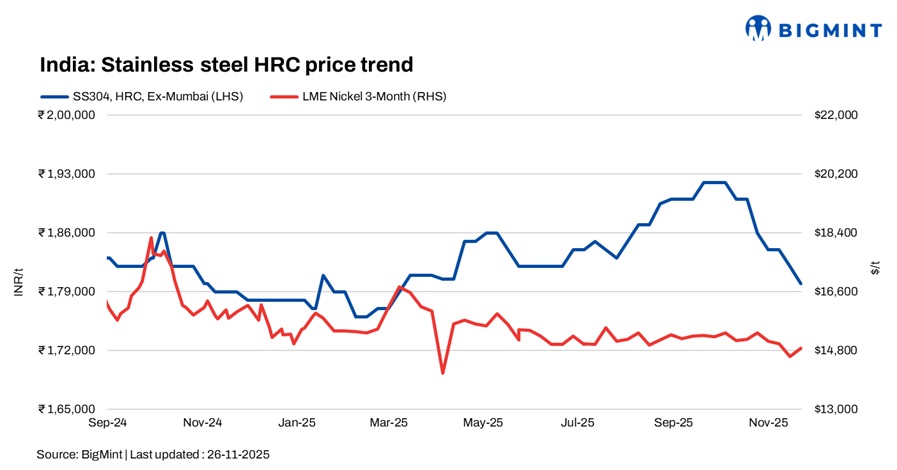

India’s stainless steel market remained sluggish, weighed down by persistent weak demand and limited sales across the value chain.

Finished flats prices ease as market sentiment weakens

BigMint’s benchmark assessment for stainless steel 304 hot-rolled coils (HRCs) stood at INR 180,000/t, ex Mumbai, down by INR 2,000/t w-o-w.

Finished stainless steel flats prices softened w-o-w amid a weak trading environment and heavy stockpiles across the value chain. According to a market participant, “Leading mills have begun reducing offers and providing discounts and rebates to stimulate bookings.”

Following the QCO extension for stainless steel flat products till 31 March 2026, import activity remained firm. Vietnam-origin 2-mm cold-rolled coils (CRC) were heard at $1,950/t (wide coil) and $1,850/t (narrow coil) CFR India, keeping competitive pressure on domestic mills.

Market sources also indicated that several producers are shifting from 304 to 316 grade production, supported by easing molybdenum prices, which has improved the cost dynamics for 316-grade melting.

Finished longs prices soften as demand remains subdued

BigMint’s benchmark assessments for stainless steel 304L (25 to 100 mm) black round bars were at INR 155,000/t, ex-Mumbai. Meanwhile, SS 316L black round bars were at INR 275,000/t, ex-Mumbai. Both were down INR 1,000/t w-o-w.

Finished longs prices edged lower w-o-w as overall stainless steel demand remained weak across domestic and export markets. Market participants noted that the slowdown in finished product offtake continued to weigh on sentiment, keeping trading activity muted.

Some mills also imported billets recently at around $1,525/t, underscoring subdued buying interest and sustained pressure on domestic producers. Additionally, in the longs segment as well, mills are increasingly shifting from 304 to 316 grade production, supported by softer molybdenum prices and more favourable cost dynamics for 316 production.

According to a mill source, “The market is not performing well, and exports are dull. The November-December outlook appears bleak. Weak trends persist, with no visible support from infrastructure-led demand.”

Indicative FOB prices of stainless steel longs were as follows: Indian 304 bright bars were at $2,050-2,100/t and 316 bright bars at $3,600-3,650/t, while Vietnam’s 304 bright bars were quoted at $1,880-1,950/t and 316 bright bars at $3,400-3,450/t.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices dropped by INR 92,000/t ($1,031/t) w-o-w from the previous assessment on 19 November 2025. The decline was driven by weak demand and fewer inquiries, while a drop in global prices further weighed on overall market sentiment.

According to BigMint’s assessment on 26 November, ferro molybdenum prices in India stood at INR 2,683,000/t ($30,060/t) ex-works.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices dropped by INR 1,200/t w-o-w to INR 113,500/t ($1,272/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices witnessed an uptick of INR 1,500/t ($17/t) as compared to the assessment on 17 November. Prices increased, as sellers in both northeast India and Bhutan kept their offers firm, backed by limited supplies.

As per BigMint’s assessment on 24 November, ferro silicon prices in India were at INR 98,500/t ($1,104/t) exw-Guwahati. In Bhutan, prices edged up by INR 300/t ($3/t) w-o-w to INR 97,800/t ($1,096/t) exw.

Ferrous scrap: India’s imported scrap market remained muted as buyers favoured cheaper domestic sponge, scrap, and HBI, making imported offers largely unworkable. HMS 80:20 was heard around $330/t CFR, HMS 90:10 at $340-345/t, shredded near $355/t against softer bids, and PNS at $350-360/t. Weak finished steel sales and a declining USD added to caution, keeping trade interest thin through the week.

Outlook

The stainless steel market is likely to remain under pressure in the near term, with prices expected to see further corrections amid weak demand and abundant domestic supply. With import competition resurfacing, additional price softening appears increasingly likely.

Leave a Reply