- Exports slide 7% m-o-m, 13% y-o-y in Oct’25

- Average export prices increase by 0.8% m-o-m

- Billet shipments drop by 21% m-o-m, 4% y-o-y

Morning Brief: China’s steel export growth stood at 6% y-o-y in January-October 2025, softening from the 9% increase seen over January-September. Reduced outflows during October pulled down the overall growth rate, with shipments during January-October totalling 97.7 million tonnes (mnt).

It is to be noted that the y-o-y percentage increase in January-October 2025 remains much lower than the 22% growth recorded in the year-ago period.

However, the fact that China has been able to sustain steel export growth in January-October 2025, despite a wave of trade safeguards and already massive export flows in 2024, continues to cause deep concern. Both importing nations and competing exporters have struggled to handle the surplus supply from the world’s leading producer.

Notably, 10MCY’25 exports are around 22 mnt higher than the 75 mnt recorded in 2023.

Factors influencing China’s steel exports in Oct’25

In October, China’s steel exports totalled 9.8 mnt. Volumes were down by 7% m-o-m and 13% y-o-y.

Fewer working days: The m-o-m decrease in steel exports in October was due to the week-long National Day holidays, which took place over 1-7 October. This effectively reduced the number of working days last month.

High base effect: Moreover, the y-o-y decrease, while substantial, can be partially attributed to a high base effect. Notably, exports in October 2024 had surged by 41% y-o-y to 11.18 mnt, the second-highest level on record in a single month, exceeded only by September 2015’s 11.25 mnt. So far, in CY’25, exports have not yet exceeded 11 mnt in a single month.

Stricter tax regulations, lower crude steel output: Other factors that could have contributed to the decline include (1) frontloading of shipments before China’s stricter export tax regulations kicked in from 1 October and (2) a 12% y-o-y decline in crude steel production, which could have taken edge off the domestic supply glut.

Rise in export prices: Lower price competitiveness could have also pressured demand. Average export prices increased by 0.8% m-o-m to $684.4/tonne (t), reflecting higher offers in August-September. To illustrate, hot-rolled coil (HRC) export prices averaged around $480/t FOB Rizhao, an increase from $464/t in July and $445/t in June, fuelled by higher raw material costs. Japan’s offers of $470/t and Russia’s $457/t, both FOB, were much lower than Chinese prices.

However, Indian offers (FOB main port) of $552/t for Europe and $508/t for the Middle East and Southeast Asia exceeded Chinese offers during the period.

Lower billet exports: Billet shipments, which have been one of the key drivers of China’s export momentum, plunged by a steep 21.4% m-o-m and 4.3% y-o-y in October to 1.12 mnt. As per a SteelOrbis report, a narrow price differential between Russian and Chinese billets and policy changes in Turkiye, a major market, led to reduced offtake. Importantly, Turkiye has mandated that 25% of its raw material requirements be sourced domestically.

Besides this, the persistent supply-demand imbalance in the domestic market and concerns about US tariffs continued to push manufacturers to offload excess volumes in overseas regions.

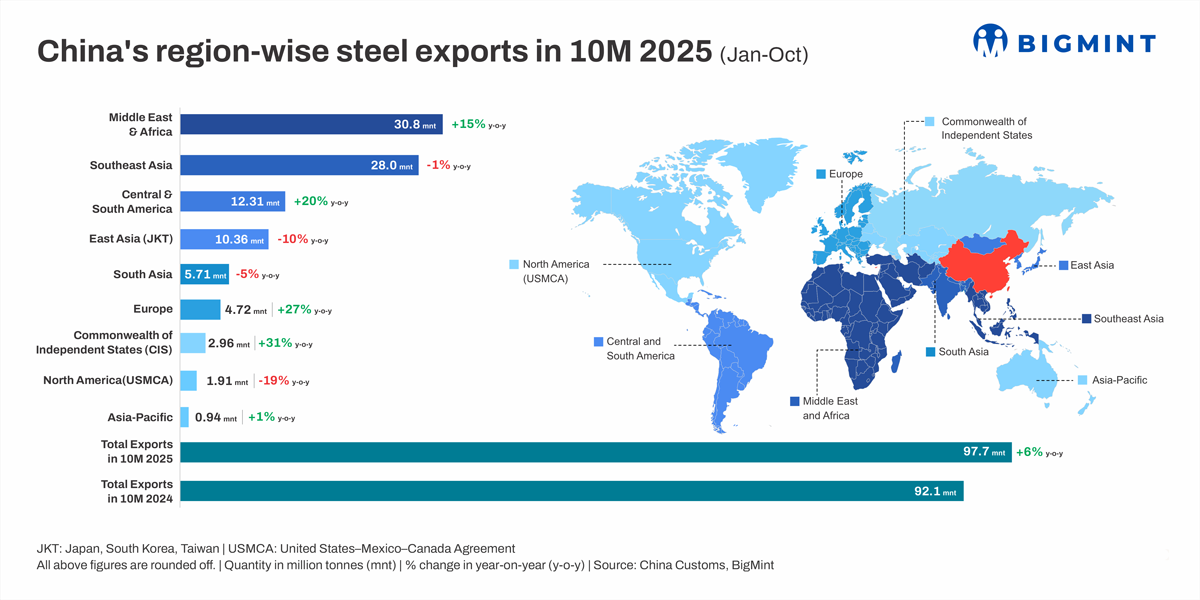

Region-wise steel exports

Exports to most regions, such as the Middle East and Africa, South Asia, and East Asia declined m-o-m in October 2025.

Meanwhile, on a y-o-y basis, all regions, except for Southeast Asia, East Asia, South Asia, and North America, continued to register growth in January-October.

Exports to the Middle East and Africa rose by 15% y-o-y. In this region, only Turkiye and Egypt recorded reduced shipments y-o-y from China, likely due to trade barriers.

Southeast Asian volumes were down by a minor 1%, stemming from a 26% decline in Vietnam, again due to trade restrictions.

Exports to Central and South America surged by 20% y-o-y. Exports to only Brazil slipped by 3%.

East Asia recorded a 10% fall y-o-y, on the back of decreased intake by South Korea and Taiwan.

While South Asia as a whole registered a 5% fall, India was the only country to reduce its imports (-34%) from China.

Europe and CIS countries witnessed growth of 27% and 31% y-o-y, respectively. Shipments to North America were down 19%, but the US, with which China has been in a heated tariff war, logged a moderate 10% drop.

China’s Region-wise steel exports in 10M 2025 (Jan-Oct)

Outlook

China’s steel exports in November 2025 may remain higher y-o-y due to three factors. First, exports during November 2024 were at 9.3 mnt, a low level that has not been reached this year yet, barring January and February, for which monthly data is not available. Secondly, weak domestic demand in China during the November winter may keep mills’ export enthusiasm high. Thirdly, global manufacturing confidence improved slightly during October, as per the latest S&P Global Business Outlook. This, coupled with optimism around potential US Fed rate cuts, may help support demand for Chinese steel products.

However, generally, the winter months of November and December witness sluggish activity due to the year-end, which may weigh on export volumes. Heightened trade barriers may also drag down demand for Chinese steel.

Overall, October’s decline should not be considered a sign of an abatement in export urgency. It is more that Chinese exports have not been able to catch up to the record peak of October 2024.

That apart, indirect steel exports, in the form of automobiles and electrical appliances, are expected to grow, considering China’s price competitiveness. In fact, research firm Langesteel projects that by 2026, China’s direct and indirect steel exports will account for one quarter or more of domestic crude steel production.

Leave a Reply