- Indian SS finished market sees sustained price pressure

- Indonesia tightens nickel curbs, global supply crunch looms

India’s stainless steel (SS) finished flats and longs prices remained stable w-o-w amid moderate demand.

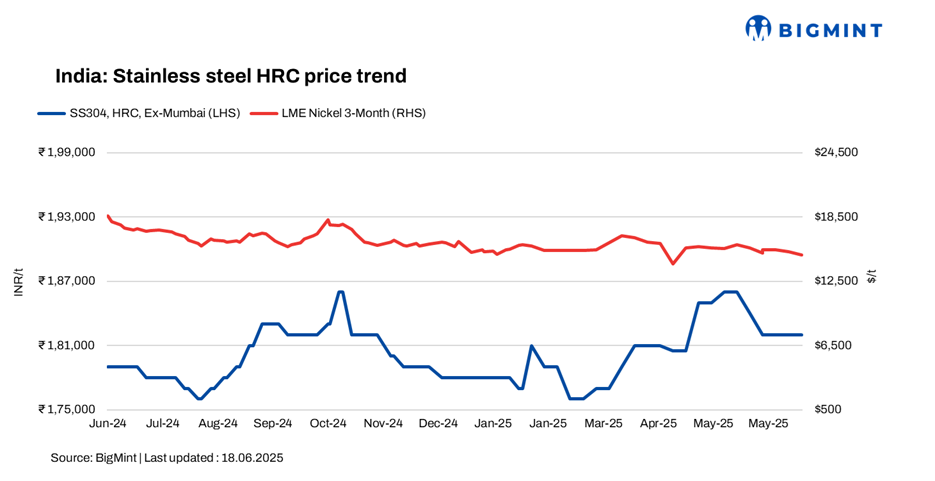

BigMint’s benchmark assessment for stainless steel 304 series hot-rolled coils (HRCs) hovered at 182,000/tonne (t), while 304L (25-100 mm) black round bars stood at INR 156,500/t, dipping by INR 500/t, both ex-Mumbai.

LME nickel, Asian NPI dip w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $14,975/t, down 1.7% against last week’s $15,240/t. Nickel stocks in LME-registered warehouses stood at 204,936 t, a 3.5% drop compared to 198,126 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) stood at RMB 935/t ($130/t). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $113/t.

Market insights

Additionally, as per BigMint’s assessment, SS 316 HRCs stood at INR 325,000/t and 316 cold-rolled coils (CRCs) at INR 333,000/t ex-Mumbai, both stable w-o-w.

Stainless steel finished market continues to face sustained pressure, especially in longs demand, with weak performance persisting for the past 3-4 months.

According to market participants, “Prices continue to down-trend, with only limited, low-volume deals reported last week. Mounting financial pressures on smaller and mid-sized mills are intensifying speculation about potential consolidations and mergers as liabilities continue to grow.

Adding to the challenges, the pace of infrastructure and government projects has slowed considerably. With these projects moving at a sluggish rate, demand is expected to stay low through the monsoon season.

Global updates

Indonesia tightens nickel market control: Indonesia is tightening its control over the global nickel market by curbing production, enforcing stricter environmental regulations, and suspending several mining projects. These measures have led to a significant supply squeeze, increasing uncertainty for stainless steel producers who rely on nickel as a key input. As Indonesia enhances its influence over supply, the resulting supply constraints are expected to impact global stainless steel production and influence future market dynamics.

Chinese stainless steel prices

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 13,850/t ($1,926/t) exw, marginally down w-o-w, while FOB tags of 304-grade CRCs were at $1,910/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices rose by INR 19,000/t ($220/t) to INR 2,674,000/t ($30,969/t) exw-India, as per BigMint’s assessment on 18 June, in comparison to the previous assessment on 11 June. Prices went up following an uptrend in LME futures prices which triggered the increase.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,800/t ($1,179/t) exw-Jajpur, remaining range-bound w-o-w.

Odisha Mining Corporation (OMC) has scheduled an auction for 76,000 t of chrome ore on 19 June. The offered quantity was reduced by 17,100 t m-o-m. However, base prices of all grades edged up by 1-2% (INR 51-373/t). The overall price stability comes amid a steady trend in the ferro chrome market, which has seen minimal fluctuations in recent weeks.

Ferro silicon: Indian ferro silicon (70%) prices dropped by INR 2,800/tonne (t) ($33/t) as compared to the previous assessment on 9 June. Prices reached their lowest point since September 2024, dragged down by subdued demand. End-users preferred imported silicon metal in place of ferro silicon, limiting domestic inquiries.

Ferro silicon prices in India were at INR 89,200/t ($1,036/t) exw-Guwahati, as per BigMints assessment on 16 June. In Bhutan as well, prices dropped by INR 1,600/t ($19/t) w-o-w to INR 90,400/t ($1,050/t) exw.

Ferrous scrap: India’s imported ferrous scrap market remained subdued this week due to weak steel demand and a wide bid-offer gap. Mills showed little interest, resisting current offer levels. Containerised shredded was offered at $360-363/t CFR Nhava Sheva, with tradable levels at around $355-360/t. HMS 80:20 softened to $342/t CFR.

Bulk scrap activity was limited, with no major offers seen from the US or Australia. Mills continued to bid well below expectations. With falling domestic steel prices and seasonal slowdown, buyers stayed cautious and focused on cheaper alternatives.

Outlook

In the short term, the stainless steel market is likely to stay sluggish amid muted demand during the monsoon season. Slower progress in infrastructure and government-led projects is expected to further dampen consumption through this period.

Leave a Reply