- Long products witness deeper correction as order inflows remain limited

- Buyers defer purchases amid volatile nickel prices

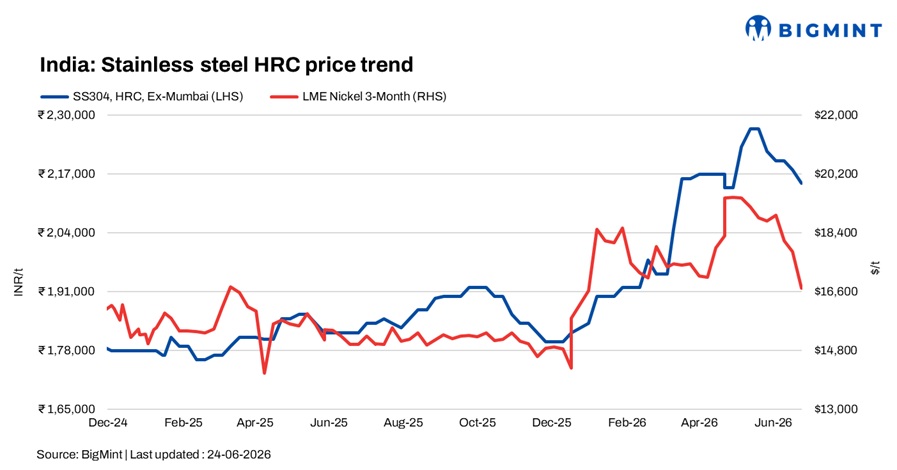

India’s stainless steel market remained subdued in the week ended 24 June 2026, as weak downstream demand, declining nickel prices, and persistent global uncertainties continued to weigh on sentiment. Market participants largely adopted a cautious stance, with mills focusing on the execution of previously booked orders while fresh booking activity remained limited. Buyers preferred to delay procurement decisions, anticipating further price corrections amid volatile raw material markets.

Finished flats market under pressure

The flat products segment remained under pressure as demand from key consuming sectors remained silent. Market participants reported limited spot transactions, with buyers restricting purchases to immediate requirements. Import activity also remained largely unviable due to elevated freight costs, reducing the competitiveness of overseas material.

Market participants noted that overall trading activity remained slow. Higher shipping costs continued to limit import opportunities, while expectations of further domestic price corrections encouraged buyers to remain on the sidelines.

According to BigMint’s assessment, 304-grade hot-rolled coil (HRC) prices declined by INR 3,000/t w-o-w to INR 215,000/t ex-Mumbai. Similarly, 316-grade HRC prices remained steady INR 398,000/t ex-Mumbai, amid soften molybdenum costs.

Longs segment witness downtrend

The stainless steel longs segment also witnessed a downtrend during the week. Weak consumption and lower nickel prices prompted some suppliers to offer aggressive discounts to secure orders. Enquiries were reported largely for small quantities, reflecting cautious buying sentiment across the market.

BigMint’s benchmark 304L black round bar prices declined by INR 4,000/t to INR 190,000/t ex-Mumbai. Meanwhile, 316L black round bar prices stood at INR 345,000/t ex-Mumbai, down by INR 5,000/t.

Export activity remained sluggish as geopolitical tensions in the Gulf region continued to affect buying interest and trading confidence. Indicative export offers for 304 bright bars were heard at $2,350-2,370/t FOB India, while 316 bright bars were reported at $4,150-4,180/t FOB India.

Raw material scenario

Outlook

India’s stainless steel market is expected to remain subdued in the near term, as weak downstream demand, ample inventory availability, and cautious procurement activity continue to weigh on sentiment. Market participants expect prices to come down with buyers largely adopting a wait-and-watch approach amid declining molybdenum costs and volatile nickel prices and uncertain market direction.

Leave a Reply