- Lower bids continue to dictate trade settlements

- Odisha iron ore fines prices remain stable w-o-w

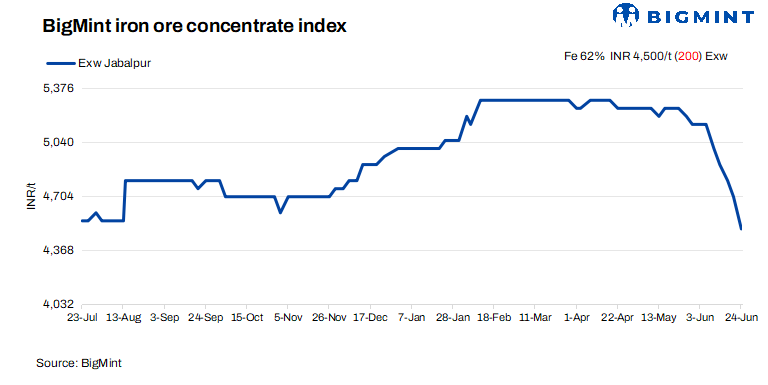

Iron ore concentrate prices in central India continued to face downward pressure during the assessment period, weighed by subdued buying interest and weak sentiment across the broader ferrous value chain. Buyers remained focused on procuring material at lower price levels, limiting any upward movement in prices despite sellers’ efforts to raise offers following the clearance of earlier dispatch backlogs.

According to BigMint’s latest bi-weekly assessment, Fe 62% iron ore concentrate prices were assessed at INR 4,500/t ($48/t) ex-works, down by INR 200/t ($2/t) from the previous assessment on 20 June 2026. Meanwhile, offers for Fe 63% grade concentrate were heard at around INR 5,000-5,200/t ($53-55/t) ex-works. With the latest decline, Fe 62% concentrate prices have fallen to their lowest level in nearly a year, with similar price levels last recorded in July 2025.

The continued weakness in concentrate prices was primarily driven by sluggish demand from pellet manufacturers and bearish sentiment in the Odisha iron ore market. Weak pellet fundamentals have significantly impacted purchasing activity, with consumers remaining reluctant to accept higher offers amid expectations of further corrections in raw material prices. The bid-offer gap that had constrained trading activity in recent weeks has narrowed, largely because sellers have become increasingly willing to align offers with buyers’ expectations in order to maintain inventory movement and cash flow.

Market sources indicated that previously pending dispatches have largely been completed, easing logistical pressure on suppliers. However, despite quoting marginally higher prices against fresh enquiries, sellers were ultimately compelled to conclude deals at lower levels due to persistent buyer resistance. Participants also highlighted the absence of the usual pre-monsoon restocking activity, which typically supports demand during this period. Both buyers and sellers largely remained on the sidelines, resulting in limited trade volumes and subdued market momentum.

Commenting on the prevailing market conditions, a Jabalpur-based seller told BigMint, “The market is currently not supportive for concentrate producers. Pellet prices continue to weaken, which remains a major concern for us. Any further decline in pellet prices could put additional pressure on concentrate realizations. Buyers are already seeking lower prices for upcoming orders, and sentiment remains cautious across the market.”

Rationale

- Three (3) trade was recorded in this publishing window, in which two (2) deal is taken into consideration, receiving a 50% weightage.

- Nine (9) offers and indicative prices were heard, and seven (7) were taken into consideration as T2 trades, receiving 50% weightage.

Factors affecting prices

- PELLEX declines by INR 200/t ($2/t) w-o-w: PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, stood at INR 9,100/t ($96/t) DAP on 23 June. Although pellet manufacturers in the Raipur cluster raised offers by INR 200/t to INR 8,900-9,000/t ($94-95/t) ex-works on 22 June, supported by improved buying interest and active procurement at lower price levels ahead of the monsoon season, overall pellet prices remained down by INR 200/t w-o-w. Market participants attributed the temporary firmness in offers to aggressive bookings following the recent price correction; however, subdued demand from sponge iron producers and weak downstream steel market fundamentals continued to weigh on the broader pellet market sentiment.

- Odisha iron ore prices remain firm w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index remained unchanged w-o-w at INR 4,950/t ($52/t) ex-mines on 20 June 2026. However, spot prices across various grades in Odisha declined by INR 100-200/t over the past week, weighed down by weak downstream steel demand and subdued buying interest from steelmakers. Market participants indicated that the limited procurement activity seen in the market was largely driven by seasonal inventory replenishment, as steelmakers increased stock levels ahead of the monsoon season to mitigate potential disruptions to mining operations and transportation. Nevertheless, overall sentiment remained cautious, with weak steel market fundamentals continuing to exert pressure on iron ore prices.

Outlook

Iron ore concentrate prices are expected to remain under pressure in the near term and may witness further downside if demand from pellet producers and steelmakers fails to improve. While some sellers with ongoing negotiations may continue to seek fresh orders, most market participants are likely to focus on executing and dispatching existing contracts. In the absence of meaningful improvement in downstream demand, buying activity is expected to remain cautious, keeping concentrate prices range-bound to weak over the coming weeks.

Leave a Reply