- Leading Indian mill hikes coil prices in mid-Dec’25

- Stainless steel longs face sluggish demand

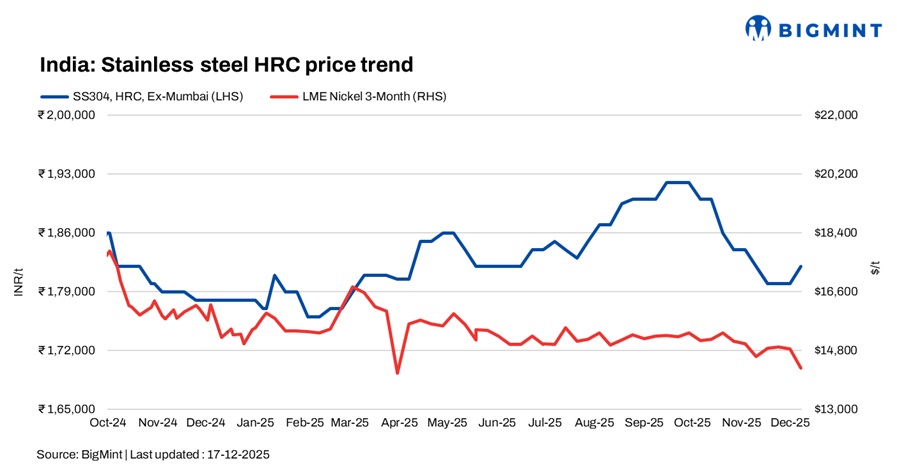

India’s stainless steel market witnessed divergent trends across product segments during the week, as tight raw material availability and global uncertainties offered support to finished flats, while sluggish downstream demand continued to weigh on longs. Market participants remained cautious amid year-end slowdown and evolving global trade developments.

Finished flats gain marginal support

The finished flats segment moved slightly higher during the week, supported by global cost pressures and selective price hikes by domestic producers.

BigMint’s benchmark assessment for 304 HRC stood at INR 182,000/t ex-Mumbai while 316 HRC stood at INR 335,000/t, both up INR 2,000/t w-o-w.

Sentiment improved after a leading domestic stainless steel producer announced a price hike effective 17 December, marking its first upward revision this month. The company raised 304-grade coils by INR 2,000/t, 316-grade coils by INR 2,000/t, and JT HR coils by INR 2,000/t. The increase was driven by a strengthening US dollar and China’s upcoming export licence regime for all stainless steel products, effective 1 January 2026.

Moreover, market sources indicated that Tsingshan (Indonesia) has increased stainless steel flat prices by $30/t, adding to cost pressures and influencing pricing sentiment in the Indian market.

Stainless steel longs remain under pressure

In contrast, the stainless steel longs segment continued to face downside pressure, as weak downstream movement and muted buying interest weighed on market sentiment. Mills largely focused on clearing existing inventories rather than fresh production.

BigMint’s benchmark assessments for stainless steel 304L (25 to 100 mm) black round bars was INR 153,000/t ex-Mumbai, down INR 2,000/t w-o-w. Meanwhile, SS 316L black round bars were at INR 268,000/t ex-Mumbai, down INR 2,000/t over the week.

A mill source said, “Finished demand has weakened significantly. We have nearly 20-25 days of scrap inventory, so the focus is on clearing material until mid-January rather than fresh buying.”

Another market participant highlighted that the conversion cost from SS 304 to SS 316 making conversion more economical than procuring SS 316 scrap. As a result, most major players are increasingly favouring conversion routes.

In the export market, indicative FOB prices for Indian stainless steel longs were heard at $2,050-2,100/t for 304 bright bars and $3,550-3,570/t for 316 bright bars, while European offers stood higher at $3,000-3,400/t for 304 and $4,000-4,050/t for 316.

Global developments influence sentiment

Global sentiment remained cautious as China announced the introduction of a new export licence system for all stainless steel products from 1 January. Under the new framework, exporters will need government approval for every shipment, aimed at curbing illegal and under-priced exports that have distorted global pricing. Exporters can begin applying for licences from 15 December.

Raw material market overview

Ferro molybdenum: Indian ferro molybdenum prices remained largely stable, inching up slightly by INR 37,000/t ($410/t) w-o-w to INR 2,644,000/t ($29,271/t) ex-works on 17 December, according to BigMint’s assessment. Regular domestic trading activity and balanced supply-demand dynamics kept prices broadly stable.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices dropped by INR 1,600/t w-o-w to INR 107,500/t ($1,189/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices inched down by INR 700/t ($8/t) on 15 December compared with the assessment on 8 December. According to BigMint, ferro silicon prices in India stood at INR 97,600/t ($1,072/t) exw- Guwahati on 8 December. In Bhutan, prices edged down by INR 500/t ($6/t) w-o-w to INR 98,500/t ($1,082/t) exw.

Ferrous scrap: India’s imported ferrous scrap market remained weak as the rupee depreciated to record lows near INR 91/$, inflating landed costs. Cheaper domestic scrap availability, high inventories, weak steel demand, and year-end holidays further curtailed import activity, limiting purchases to urgent requirements.

Containerised shredded scrap was assessed around $346/t CFR Nhava Sheva, while EU-origin HMS 80:20 hovered at $315–319/t CFR. Import volumes dropped sharply to around 3,000 t, compared with 8,000 t last week.

Outlook

India’s stainless steel finished market is expected to remain subdued in the near term, with weak end-user demand, year-end caution, and adequate inventories limiting trading activity. While finished flats may continue to find marginal support from global developments and cost pressures, stainless steel longs are likely to remain under pressure until downstream demand improves. Market participants anticipate some pickup in activity only after mid-January once procurement cycles normalise and demand visibility improves.

Leave a Reply