- Buyer activity gradually increases in Jabalpur

- High-grade concentrate availability remains tight

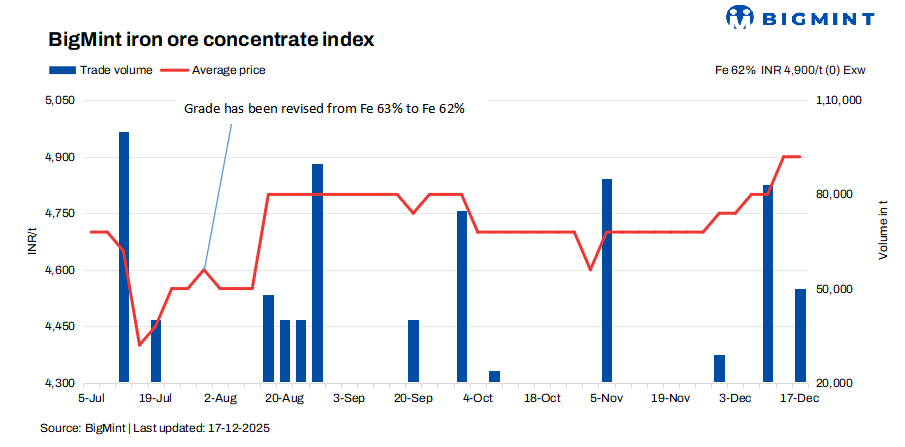

BigMint’s latest bi-weekly assessment for India’s iron ore concentrate (Fe 62%) remained stable at INR 4,900/tonne ($54/t) ex-works Jabalpur on 17 December as against 13 December. Meanwhile, market momentum strengthened noticeably, with prices climbing by INR 100/t ($1/t) w-o-w, driven by aggressive seller-side offers and tightening availability. The strength in prices was further reinforced as bulk transactions were heard concluded at these elevated levels.

Meanwhile, Fe 63% iron ore concentrate prices stayed firm at INR 5,100-5150/t ($57/t) ex-works, reflecting sustained tightness in the availability of high-grade material. Industry sources indicated that severe scarcity of premium-grade ore across regions has effectively prevented any downside movement, leaving buyers with very limited procurement flexibility. Supply pressure has been compounded by the fact that very few sellers are currently offering this grade, as ongoing grade degradation in the region has sharply reduced output of higher-quality concentrate. These factors together continue to uphold price levels.

Moreover, buyer participation has been increasing, as new entrants seek to gain a foothold and compete in the regional market. This has intensified competition for limited volumes, enhancing sellers’ pricing leverage and providing added support to current price levels.

A Jabalpur based seller told BigMint that “a revival in the finished steel segment is expected to provide strong and sustained support to iron ore concentrate prices in the coming weeks.” The seller added that fresh offers are unlikely to emerge until previously booked orders are fully dispatched, effectively restricting near-term availability and reinforcing price firmness.

A Jabalpur-based buyer said, “Ample concentrate inventories and subdued current consumption have temporarily kept buyers out of the market.” However, he cautioned that this pause may be short-lived, indicating that prices could start moving higher by January.

Rationale

- Two (2) trade was recorded in this publishing window and was taken into consideration, receiving a 50% weightage.

- Seven (7) offers and indicative prices were heard, and four (4) were taken into consideration as T2 trades, receiving 50% weightage.

Factors influencing prices

BigMint’s Odisha iron ore fines (Fe 62%) index remained unchanged w-o-w at INR 5,700/t ($63/t) ex-mines on 13 December. Iron ore prices in Odisha stayed firm supported by bulk bookings concluded by major miners and a prompt and encouraging response to auctions held by selected producers.

Market participants noted that large miners were able to secure substantial volumes in recent days, reinforcing their confidence in prevailing price levels. Consequently, miners kept their offers steady despite mixed conditions in the downstream steel market, as consistent procurement activity was sufficient to offset cautious sentiment and sustain current prices.

PELLEX inches lower

PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, inched lower by INR 50/t ($0.5/t) to INR 9,400/t ($103/t) DAP on Tuesday, compared with the assessment on 12 December. Pellet prices in the Raipur region continued to face headwinds, as trading activity remained sluggish amid a sustained downturn in sponge iron and semi-finished steel prices.

Market participants noted that soft downstream demand has significantly dampened buying interest, resulting in limited deal finalisation even as sellers largely stood firm on their offer levels. With procurement activity remaining sparse and market liquidity thin, overall sentiment stayed guarded, leaving pellet prices exposed to continue pressure in the near term.

Outlook

Iron ore concentrate prices are expected to remain stable in the near term, supported by tight supply, limited fresh offers, and sustained buyer participation. While clearing of older orders and a gradual improvement in finished steel demand could provide additional support. Overall, prices are likely to hover around current levels with a slightly firm bias, with clearer market direction expected toward January.

Leave a Reply