- January South Africa exports down 33% m-o-m

- Domestic coal steady; SECL allocations lower

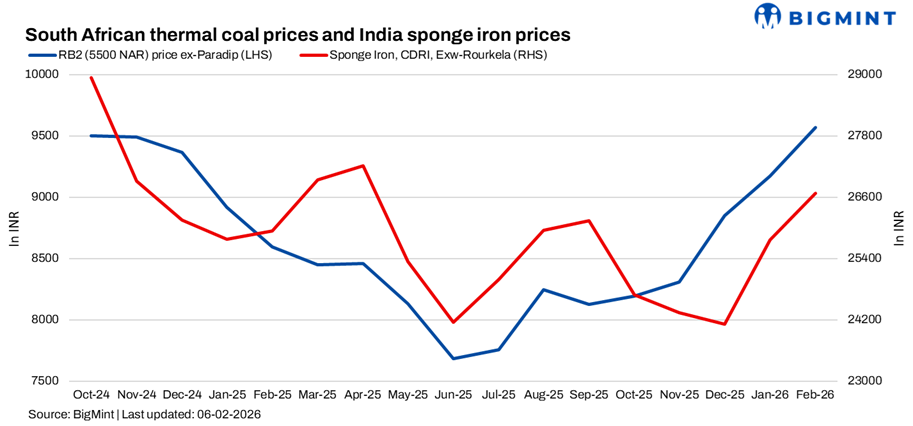

South African thermal coal prices at Indian ports extended gains w-o-w amid tight inventories and firm import offers. As per BigMint assessment, exw-Paradip 5,500 NAR increased INR 200/t to INR 9,700/t, while 4,800 NAR rose INR 50/t to INR 8,150/t. At Vizag, 5,500 NAR gained INR 100/t to INR 9,500/t, while 4,800 NAR remained at INR 8,000/t. Portside 5,500 NAR offers were heard near INR 10,000/t. FOB levels hovered around $85/t, translating to roughly $100/t CNF. RB2 was offered at INR 9,500-9,600/t with acceptance closer to INR 9,400/t, while RB3 was indicated at INR 8,100-8,200/t.

Low availability continued, with limited port stocks at Gangavaram, Navlakhi and Haldia ports.

South African non-coking coal exports in January fell to 4.03 mnt, down 33.2% m-o-m and 32.2% y-o-y, tightening prompt supply.

Market discussions indicated 6000 NAR FOB could approach $100/t by late February or early March, supported by buying interest from South Korea, Bangladesh and Vietnam, alongside India’s DRI demand. Sponge iron CDRI exw-Rourkela increased INR 500/t w-o-w to INR 26,800/t, though sentiment remained subdued as mills covered near-term requirements and monitored price direction.

In the Atlantic basin, improved logistics in South Africa are shaping the broader supply outlook. Richards Bay Coal Terminal has outlined plans to raise exports toward 65 mnt in 2026, supported by better rail performance, reduced cable theft and automation investments. This improved export reliability is adding optional supply to the Atlantic market.

Overall, while South African portside prices in India remain firm due to low inventories and strong Asian enquiries, improving export reliability and softer Atlantic fundamentals may cap excessive upside unless logistics tighten again or gas prices spike sharply.

On the domestic side, non-coking coal prices remained unchanged w-o-w, with 5,000 GCV at INR 5,750/t and 4,500 GCV at INR 4,800/t. SECL offered 554,000 t on 31 January and allocated 128,100 t, sharply lower than 915,200 t on 27 January. On 3 February, 380,050 t of G11 was offered and fully allocated, indicating steady utility-led demand despite lower volumes.

Leave a Reply