- Soft sponge prices keep pressure on SA coal

- Increased freight rates to weight on prices

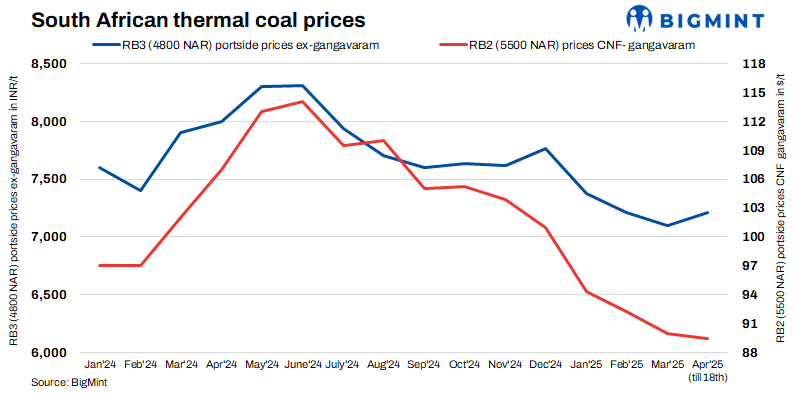

BigMint’s assessment of portside South African thermal coal prices in India showed a mixed trend this week. RB2 (5500 NAR) offers remained stable at INR 8,450/tonne (t) exw-Gangavaram, while RB3 (4800 NAR) also held steady at INR 7,200/t. However, slight softening was seen at other ports. At Paradip, RB2 dropped to INR 8,350/t and RB3 to INR 7,200/t. Exw-Vizag, RB2 was heard at INR 8,300/t and RB3 at INR 7,150/t.

Recent deals:

- A deal for 30,000t of RB2 was concluded at INR 8,400/t ex-Dhamra.

- Another deal for 24,000t of RB2 was concluded at INR 8,400/t ex-Dhamra.

The portside South African thermal coal market remained largely inactive, with only a few need-based buyers procuring based on specific technical requirements. The continued softness in sponge iron prices contributed to subdued demand.

Market updates

South African coal export offers firm: RB2 was assessed marginally higher at $76.5/t FOB, while RB3 edged up to $63.5/t FOB as of 18 April, supported by limited supply of RB3.

Domestic coal prices steady: Indian coal prices remained flat, with 4500 GCV and 5000 GCV grades at INR 4,500/t and INR 4,950/t exw-Bilaspur. In recent SECL auctions, bids were again seen hovering near the base price.

Sponge iron prices ease further: Indian C-DRI prices dropped by INR 400/t w-o-w to INR 27,150/t exw-Rourkela, reflecting weak sentiments in the domestic steel market.

Outlook

South African portside coal prices may stay range-bound due to limited buying interest. Higher freight rates and sluggish sponge demand may continue to weigh on market sentiments.

Leave a Reply