- Buyers remain cautious as high offers curb trades

- Weak sponge iron market limits bulk spot purchases

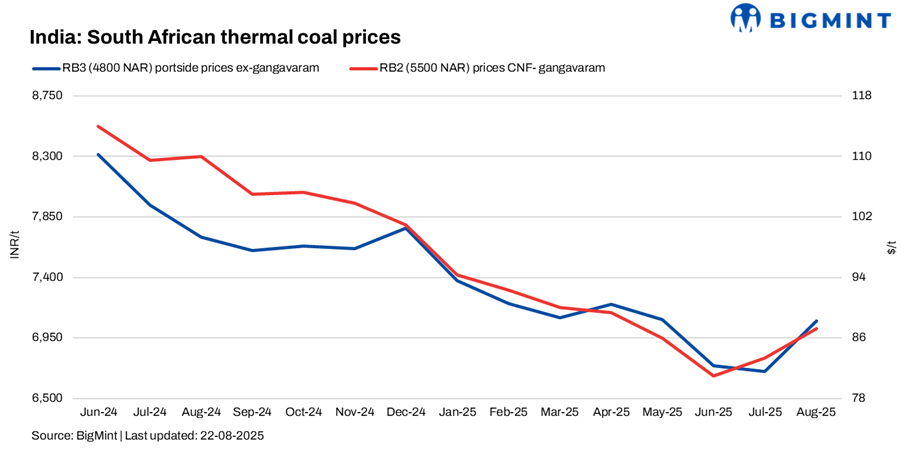

South African RB2 thermal coal prices at Indian ports rose INR 50/t w-o-w to INR 8,300/t exw-Gangavaram, while RB3 gained INR 100/t to INR 7,200/t. Offers for RB2 in the eastern ports were heard at INR 8,300-8,350/t. Higher freight rates pushed offers up, but demand remained sluggish. At Vizag, no trader cargoes were seen in the past month, with activity limited to end-users.

Domestic coal market trends

Domestic coal prices showed mixed movement this week. BigMint assessed 5000 GCV at INR 5,000/t exw-Bilaspur, rising by INR 250/t w-o-w, while 4500 GCV remained stable at INR 4,500/t. The uptrend in 5000 GCV is being supported by supply disruptions caused by monsoon-affected mining operations, along with gradual demand recovery from the steel sector, which continues to provide a floor to domestic market sentiment.

Portside inventories increase marginally

India’s portside thermal coal stocks rose 1.2% w-o-w to 13.86 million tonnes (mnt) in Week 33 from 13.70 mnt in Week 32.

Sponge iron market weakens further

BigMint’s C-DRI index (ex-Rourkela) slipped INR 200/t w-o-w to INR 25,900/t. On 21 August, spot sponge iron prices dropped INR 50-100/t across Raipur, Bellary, and other hubs, weighed by weak demand and cautious buying. Durgapur was an exception, where prices edged up INR 50/t. Around 12,000 t of sponge iron changed hands, mostly need-based purchases. Sellers offered discounts, but poor finished steel demand kept sentiment bearish.

Export offers move up slightly

South African RB2 export offers increased $1/t w-o-w to $74/t FOB, while RB3 gained $2/t to $62/t, reflecting firmer sentiment despite muted Indian buying.

Outlook

Portside South African coal offers may remain elevated in the near term on the back of firm freight rates and limited trader activity. However, actual trade volumes are expected to remain under pressure until steel demand shows a meaningful recovery in the coming weeks.

Leave a Reply