- Higher landed costs trigger domestic price protection

- Spinning mills face margin pressure amid weak yarn demand

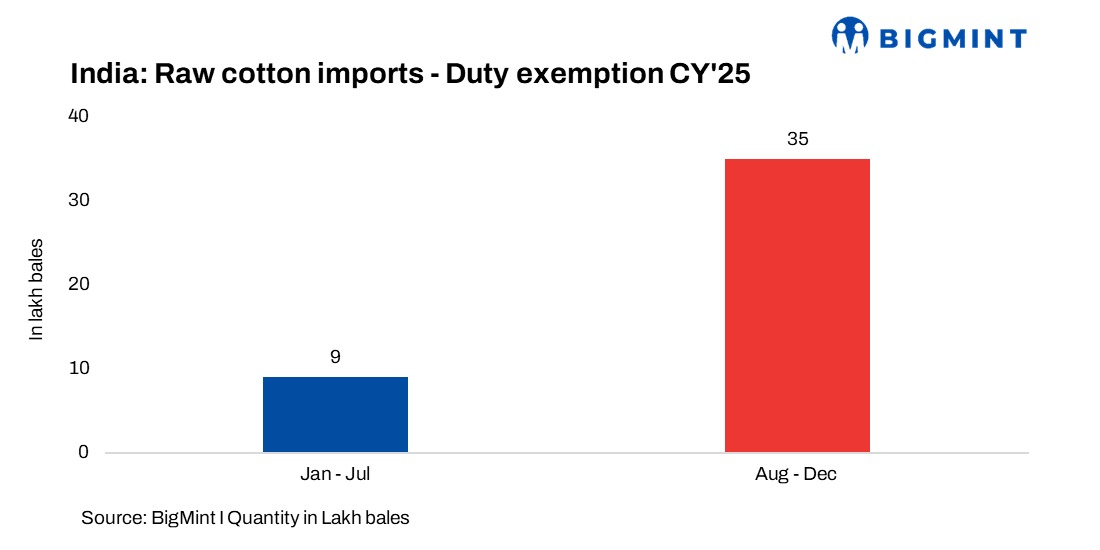

India has reinstated the 11% import duty on raw cotton from 1 January 2026, as the temporary duty-free import window expired without further extension. The exemption, introduced in August 2025 and extended multiple times until 31 December, was aimed at easing raw material costs for the textile value chain during a period of weak exports and global trade disruptions.

With no fresh notification issued, cotton imports are now subject to the standard customs duty, immediately increasing landed costs for overseas cotton.

What happened is a clear policy reversal in favour of domestic price protection. During the duty-free phase, India imported an estimated 35-36 lakh bales (3.5-3.6 million bales), mainly from Brazil, the US and Australia, as spinning millers preferred cheaper imported fibre over higher-priced domestic cotton. The return of duty raises the cost of imported cotton by roughly INR 6,000-7,000/tonne (t), narrowing the price gap between imported and Indian cotton. This is expected to slow fresh import bookings and shift demand back towards domestic supplies, particularly in central and southern India.

The clue lies in the persistent weakness in domestic cotton prices despite MSP support. Spot prices in several mandis, especially in Vidarbha, have remained well below the minimum support price (MSP) of INR 8,110/quintal, in some cases closer to INR 6,700-7,000/quintal. Farmer groups have consistently argued that duty-free imports were depressing local prices at a time when arrivals were heavy and Cotton Corporation of India (CCI) procurement was already absorbing a large share of the crop. Reinstating the duty is intended to prevent imported cotton from undercutting domestic fibre and to reinforce the MSP framework during peak arrival months.

For spinning millers, however, the timing is challenging. Yarn demand remains uneven, export orders are yet to fully recover, and margins are already under pressure due to weak downstream offtake. While duty-free imports helped spinning millers manage costs and blend higher-quality fibre, the re-imposition of duty raises input costs at a time when passing on price increases to buyers is difficult. Many mills may now rely more on domestic cotton or operate with tighter spreads, especially in medium-count yarns.

Outlook

What may happen next is a gradual firming of domestic cotton prices, supported by reduced import competition and continued MSP procurement. However, prices are unlikely to rise sharply unless yarn and fabric demand improves meaningfully.

For ginners, the policy offers some relief through better price realisation and slower inventory liquidation. For spinning millers, sourcing strategies may shift back towards domestic cotton, with greater emphasis on quality segregation and cost control. Brokers should expect import parity to weaken and domestic price discovery to remain policy-influenced rather than purely market-led in the near term.

Leave a Reply