- China, Japan record notable declines in exports

- Price recovery hinges on steel market revival

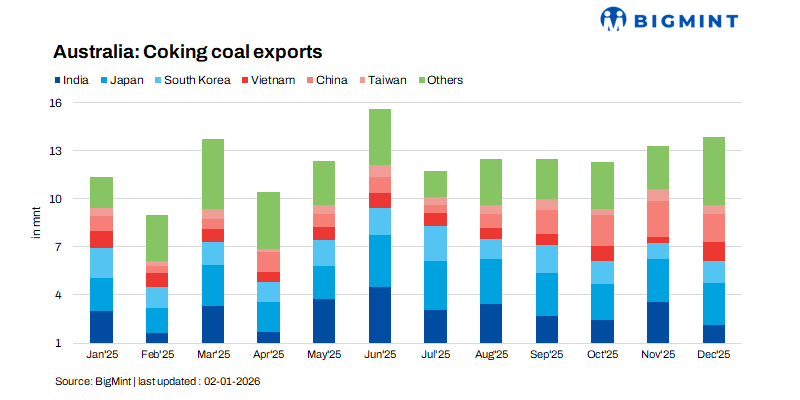

During January-December 2025 (CY’25), Australia’s coking coal exports stood at 148.5 mnt, down 5% from 156.3 mnt in 2024. The decline was largely driven by subdued global steel demand, cautious raw material procurement amid economic uncertainty, and lower steel output in key consuming nations, particularly China and Japan.

These factors constrained import volumes, although select Southeast Asian markets continued to lend moderate support due to comparatively healthier production margins.

However, exports recorded a modest 4.1% m-o-m rise in December to 13.86 million tonnes (mnt) from 13.32 mnt in November. Australia’s coking coal export shipments recorded a decline of 5.9% y-o-y compared with 14.73 mnt in December 2024, reflecting persistent softness in global steelmaking activity.

Key markets: Diverging demand trends

India emerged as a bright spot, with imports rising 4.8% y-o-y to 38.4 mnt in CY’25, supported by improved steel production. In contrast, Japan’s imports declined by 12% y-o-y to 30 mnt, in line with ongoing production cuts and weak domestic steel demand.

China’s imports fell sharply by 21% y-o-y to 13.8 mnt during the period, reflecting policy-driven supply adjustments and muted steel sector activity. Meanwhile, imports by South Korea and Taiwan remained largely stable y-o-y at 18.6 mnt and 6.3 mnt, respectively.

Vietnam recorded the strongest growth among major buyers, with imports surging 25.9% y-o-y to 10.1 mnt, underpinned by robust steel and coke production, favourable margins, and higher mill utilisation rates.

Port-wise export performance

Export performance across Australian coal terminals in January-December 2025 remained mixed. Dalrymple Bay Coal Terminal (DBCT) reported a 5% y-o-y decline in shipments to 47.9 mnt, while Hay Point saw a 3.5% y-o-y reduction to 34.1 mnt.

In contrast, Gladstone Port registered a marginal 1.4% y-o-y increase in exports to 47.2 mnt, partially offsetting declines at other terminals. Abbot Point experienced a sharper contraction, with shipments falling 17.6% y-o-y to 15.1 mnt. Among smaller ports, Port Kembla recorded a notable 30.7% y-o-y drop to 3.1 mnt, whereas Newcastle Port exports remained broadly stable at around 1.1 mnt.

Prices recover in Dec’25

Australian coking coal prices strengthened in December 2025, rising by approximately $14/t m-o-m compared with November, supported by disruption in supply-side, restocking interest from select buyers, and improved margins in parts of Southeast Asia.

Outlook

Australia’s coking coal export outlook remains firm in the coming month while seasonal issues may impact supplies. Demand support from India and Southeast Asia may keep prices range-bound.

Leave a Reply