- Limited trades occur amid approaching FY-end

- LME nickel prices drop, Asian NPI rises w-o-w

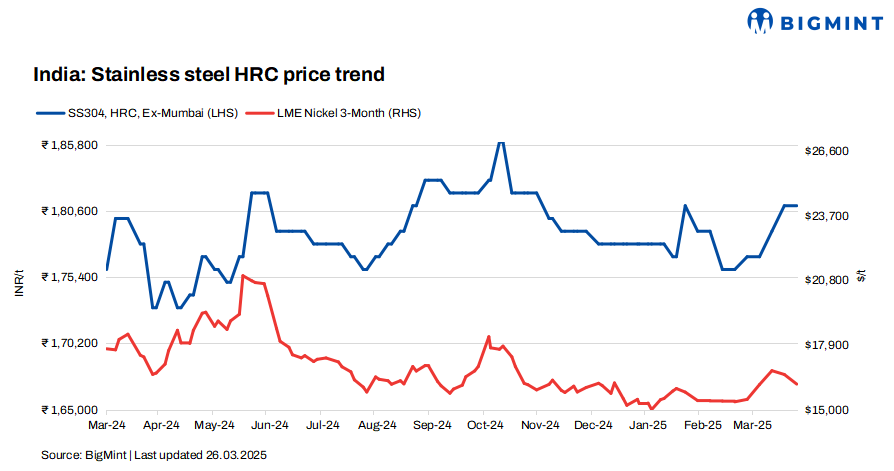

Prices of Indian domestic stainless steel (SS) finished products remained stable w-o-w, amid sluggish activity during the fiscal year-end.

BigMint’s benchmark assessment for stainless steel (304 series) hot-rolled coils (HRCs) stood at INR 181,000/tonne (t), steady w-o-w, while 304L (25-100 mm) black round bars also remained stable at INR 160,500/t, both ex-Mumbai.

LME nickel tags drop, Asian NPI rises w-o-w

At the time of reporting, three-month LME nickel prices stood at $16,170/t, reflecting a marginal dip of 2.3% from last week’s $16,565/t. Nickel stocks in LME-registered warehouses remained largely stable at 201,330 t compared to 200,796 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) witnessed an increase of RMB 15/metric tonne unit (mtu) ($1/mtu) w-o-w to RMB 1,025/mtu ($141/mtu). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $122/mtu, up by $2/mtu w-o-w.

Finished market remains steady w-o-w

As per BigMint’s assessment, SS 316 HRCs remained stable w-o-w at INR 325,000-327,000/t ex-Mumbai.

BigMint’s assessment of SS 316L (25-100 mm) black round bars stood at INR 270,000-272,000/t ex-Mumbai, unchanged w-o-w. Prices of SS 316L (25-100 mm) bright bars stood at INR 288,000-290,000/t ex-Mumbai, steady w-o-w.

A market participant noted, “The market continues to show sluggish activity, particularly in stainless steel finished materials. With the financial year coming to a close in March, we are not expecting any major trades in the near future, which only adds to the overall dullness in the market.”

As the fiscal year-end approaches, most mills prioritised the collection of credit payments. To avoid any financial strain, they steered clear of long credit gaps, focusing on closing their books for the year.

On the demand side, there was hardly any improvement, and exports of longs slowed due to the weakness in the EU market, which remains the largest export destination for Indian longs.

Chinese stainless steel prices rise

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 14,250/t ($1,961/t) exw, up by RMB 200/t ($27/t) w-o-w, while FOB prices of 304-grade CRCs were at $1,910/t.

Moreover, China’s stainless steel imports fell 29.3% y-o-y to 322,000 t in the first two months of 2025, while exports rose 11.84% to 755,000 t. Imports declined by 28% y-o-y in February, while exports dropped 42.7% m-o-m but grew 6.6% y-o-y. Net exports in February surged 220.9% y-o-y, while a total of 433,400 t was recorded for the first two months, up 104.4% y-o-y.

Raw materials overview

Ferro molybdenum: Indian ferro molybdenum prices witnessed a slight decline of INR 23,000/t ($268/t) this week, compared to the previous assessment on 19 March. Barring the slight drop, prices were largely stable w-o-w amid unchanged global prices and regular trades in the Indian domestic market.

As per BigMint’s assessment on 26 March, ferro molybdenum prices in India were at INR 2,572,000/t ($30,026/t) exw on a 60% pro rata basis.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,500/t ($1,173/t) exw-Jajpur, stable w-o-w amid limited market movements.

Outlook

Domestic demand is anticipated to increase in April and May, driven by upcoming project-based work, with particularly strong demand expected from the western region.

Leave a Reply