- LC constraints to keep domestic scrap prices firm

- Domestic rebar sales sluggish despite stable pricing

Bangladesh’s steel industry is grappling with subdued demand during Ramadan and the sluggish pace of infrastructure projects. Mills are operating below capacity to control costs, while some are accepting lower or even negative margins to maintain cash flow and keep operations running.

With the Eid holidays approaching, market activity is expected to slow further, leading to reduced steel consumption and lower production levels. Industry participants remain cautious about a quick recovery, with any rebound likely to be gradual and limited post-holidays.

Imported market

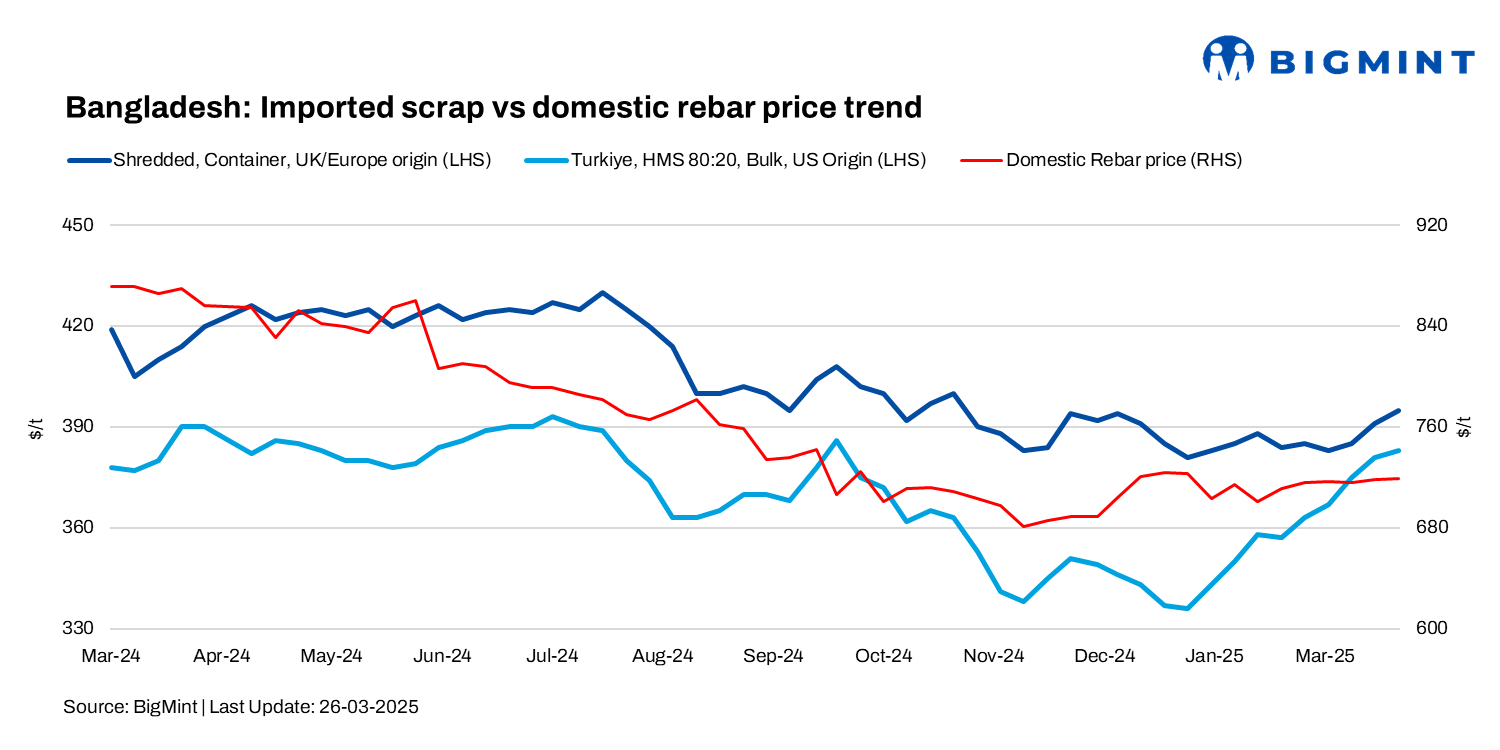

A Chattogram-based scrap trader noted that containerised busheling and shredded are offered at $395-400/t, Australian HMS 80:20 at $370-375/t, and shredded at $385-390/t. Busheling from Malaysia is at $395/t, while Singapore PNS is at $390-395/t. US West Coast bulk offers HMS 80:20 at $385-390/t, while Japanese H2 bulk was recently booked at $370-372/t.

Another Bangladeshi importer shared that PNS from Hong Kong/Malaysia is offered at $385-390/t, HMS bundles from Hong Kong at $360/t, PNS bundles at $375/t, and Malaysian shredded at $375-380/t CFR Chattogram.

A scrap importer noted some deals but said sellers are reluctant to match buyers’ prices, creating a $5-7/t gap. Japanese rebar bundles are at $388/t CFR, while Australian shredded is at $390/t, with buyers aiming for $380/t. Australian HMS 80:20 is offered at $371-372/t, but buyers are bidding $364-365/t.

Another trader reported Malaysia PNS offers at $397/t CFR Chattogram, but rising prices are limiting inquiries.

BigMint’s weekly assessments

- European-origin containerised shredded inched up by $4/t w-o-w to $395/t.

- European-origin HMS (80:20) increased by $2/t w-o-w to $375/t

- US-sourced HMS (80:20) bulk prices stood at $384/t, up by $6/t w-o-w.

- Japanese-origin H2 bulk prices stood at $372/t CFR Chattogram, inched up by $6/t w-o-w

Recent imported deals:

- 4,000 t PNS from Hong Kong sold at $390/t CFR Chattogram.

- 1,000 t Shredded from Australia sold at $390/t CFR Chattogram.

- 1,000 t Rebar bundles from Japan sold at $388/t CFR Chattogram.

- 1,000 t PNS from Malaysia sold at $385/t CFR Chattogram.

Domestic market

- Domestic scrap prices remain elevated due to low LC approvals, but with Eid approaching, a 10-day market halt and no new LC openings may pressure prices downward.

- Local scrap trades at BDT 57,000-59,000/t ($468-485/t), Dhaka rebar at BDT 80,000-83,000/t ($657-682/t), and Chattogram rebar at BDT 86,000-88,000/t ($706-723/t).

- A domestic steel supplier noted that the Eid halt will slow purchases, with ship-scrap at BDT 56,000-58,000/t exy ($460-477/t). Dhaka rebar hovers at BDT 82,500-83,500/t exw ($678-686/t), while Chattogram rebar stands at BDT 86,000-86,500/t exw ($706-710/t), with sluggish sales expected.

Green steel project setback

Bangladesh’s BDT 37 billion green steel project by Bashundhara Multi Steel Industries Limited (BMSIL) is facing setbacks due to a lack of utility infrastructure and policy support. The plant, located in Mirsarai, Chattogram, aims to produce eco-friendly steel using Danieli’s MIDA technology.

Initially set for mid-2026 production, the project now faces delays as promised funding falls short. Without immediate policy intervention, its future remains uncertain.

Outlook

The upcoming Eid holidays, starting in the fourth week of March, are expected to stall market activity, with consumption likely to remain stagnant for over 10 days. A gradual recovery is anticipated from mid-April as operations resume and pent-up demand is released. However, the rebound is expected to be mild, with no sharp revival in sight due to weak underlying fundamentals. While short-term demand may see a slight post-holiday boost, the industry remains cautious about its sustainability.

Leave a Reply