- Maximum power demand rises 13% on average, IEX prices surge 22% y-o-y

- Hydropower generation falls 29% y-o-y due to weaker reservoir inflows

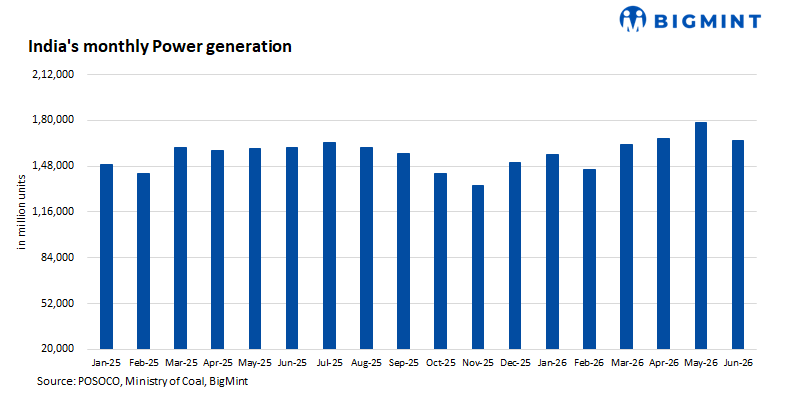

India’s power market tightened considerably during the first 28 days of June 2026 as a delayed and uneven southwest monsoon prolonged cooling demand, curtailed hydroelectric generation, and increased reliance on coal-fired power plants. Despite robust growth in renewable generation, coal remained the backbone of the electricity system, helping meet record demand, while coal inventories at thermal power plants steadily declined and spot electricity prices on the Indian Energy Exchange (IEX) climbed up sharply.

The data presents a clear picture of a power system that successfully met rising demand but did so at the cost of drawing down coal stocks and experiencing significantly tighter market conditions, particularly during evening peak hours.

Delayed monsoon extends summer power demand

Although the southwest monsoon officially reached Kerala on 4 June, its progress across the country proved unusually sluggish. Instead of bringing widespread relief from high summer temperatures, the monsoon stalled almost immediately after onset, prolonging heat conditions across many of India’s largest electricity-consuming regions.

Between 4 and 15 June, India received only 19.2 mm of rainfall against the normal 53.7 mm, resulting in a nationwide rainfall deficit of nearly 64%. The Northern Limit of Monsoon (NLM) then remained virtually stationary for almost ten days, stretching from the Konkan coast through Maharashtra to Bihar before advancing only during the final week of June.

The delayed advance prolonged cooling demand while limiting reservoir inflows, reducing hydroelectric generation precisely when electricity demand was strengthening.

Only after 26 June did weather systems strengthen sufficiently to revive rainfall across the northeast, Sub-Himalayan West Bengal, and the west coast, allowing the monsoon to resume its northward advance. While this improved the rainfall outlook towards month-end, it came too late to materially influence the generation mix during most of June.

The India Meteorological Department (IMD) attributed the delayed advance to unfavourable upper-air circulation that inhibited moisture penetration over the subcontinent despite abundant moisture over surrounding seas. Skymet Weather also highlighted the emerging El Niño risk, warning that seasonal rainfall could remain below normal if ocean-atmosphere conditions strengthen during the second half of the monsoon.

Electricity demand reaches record levels

Contrary to expectations that the onset of the monsoon would moderate electricity consumption, demand remained exceptionally strong throughout June.

Average daily maximum demand met increased to around 250 GW, up from approximately 221 GW during the corresponding period last year, representing growth of over 13%.

More importantly, India’s peak demand continued to establish new records. The highest demand during the first 28 days of June reached 264,768 MW on 27 June, exceeding the previous year’s peak of 242,493 MW by more than 22 GW.

The delayed arrival of widespread rainfall across northern, western, and central India prolonged air-conditioning demand through most of the month, while economic activity and industrial consumption remained supportive.

IEX spot prices signal a much tighter market

The stronger demand environment was clearly reflected in India’s spot electricity market.

The average Day-Ahead Market (DAM) clearing price on the IEX increased from around INR 3,700/MWh during the corresponding period of June 2025 to approximately INR 4,500/MWh in June 2026, representing an increase of roughly 22%.

The tightening market became particularly evident during the second half of June.

During the first half of the month, daily market clearing prices generally ranged between INR 2,100-5,000/MWh.

However, prices strengthened steadily after mid-June as demand increased and hydro generation remained subdued. The highest daily market clearing price reached INR 7,002/MWh on 27 June, the highest level recorded during the month.

Growing intraday volatility

Hourly market data highlights the increasingly important influence of renewable generation on electricity prices. During daylight hours, abundant solar generation frequently pushed market prices to extremely low levels as renewable output displaced conventional generation.

However, once solar generation declined during the evening, prices rose sharply as coal-fired stations became the principal source of balancing power.

On several occasions during the final week of June, hourly prices reached the market ceiling of INR 10,000/MWh, illustrating the scarcity of flexible generation during evening peak demand.

The widening gap between low daytime prices and extremely high evening prices highlights one of the defining characteristics of India’s evolving power market — renewables continue to reduce daytime prices, but thermal generation remains indispensable after sunset.

Coal continues to anchor India’s power system

India’s generation mix adjusted significantly to meet higher electricity demand.

Coal-fired generation increased by 8.6% y-o-y, contributing the largest absolute increase in electricity production during the month.

Renewable energy continued its rapid expansion, increasing 15.4% over the previous year, while nuclear generation rose by 17.3%. However, these gains were more than offset by a sharp 28.9% decline in hydroelectric generation due to weaker reservoir inflows caused by the delayed monsoon.

Gas, naphtha, and diesel-based generation declined by almost one-third, reflecting the continued high cost of these fuels and their role as marginal sources of generation.

The changing generation mix demonstrates that although renewable capacity continues to expand rapidly, coal remains India’s primary balancing fuel during periods of elevated demand and lower hydro availability.

Coal stocks continued to decline

Higher coal generation inevitably translated into lower inventories at thermal power plants.

Overall inventories declined by approximately 4.61 mnt during June as coal consumption consistently exceeded receipts.

By the end of the month, the number of thermal power stations classified as having critical coal stocks had increased from 22 to 34, reflecting increasing pressure on inventories.

Daily CEA coal stock reports also indicate that several generating companies continued operating well below normative inventory levels, particularly in Andhra Pradesh, Telangana, Tamil Nadu, and parts of Maharashtra, underscoring the uneven distribution of coal availability across the country.

Towards the end of June, thermal power plants were consuming around 2.66 mnt/day of coal compared with receipts of approximately 2.58 mnt/day, explaining the continued drawdown in inventories despite steady coal supplies.

Imported coal-based stations, however, remained relatively stable, indicating that most of the inventory decline occurred at domestic coal-fired plants.

Outlook

June 2026 reinforced several important structural trends in India’s electricity market.

First, coal continues to be the backbone of India’s power system. Even with strong growth in renewable generation, coal-fired stations supplied the incremental electricity needed to meet record demand and compensate for weaker hydro generation.

Second, renewables are increasingly reshaping intraday market dynamics rather than replacing coal. Solar generation continues to depress prices during daylight hours, but thermal generation remains essential for meeting evening demand, resulting in pronounced price spikes once solar output declines.

Third, coal inventory management will remain critical through the monsoon season. Although the system avoided widespread supply disruptions, declining inventories and the increasing number of critical plants demonstrate how quickly stock buffers can erode when coal consumption outpaces receipts.

Looking ahead, the late revival of the southwest monsoon should gradually improve reservoir inflows and moderate cooling demand during July. However, if rainfall distribution remains uneven or El Nino conditions strengthen later in the season, coal-fired generation is likely to continue carrying the bulk of India’s peak electricity demand, keeping pressure on coal logistics, plant inventories and spot electricity prices.

The developments during June underline a broader reality for India’s energy transition: while renewable energy is growing rapidly, the reliability and flexibility of the power system continue to depend fundamentally on coal. Until large-scale storage and flexible balancing resources become more widely available, coal will remain the principal stabilising force during periods of high demand and weather-related variability.

Leave a Reply